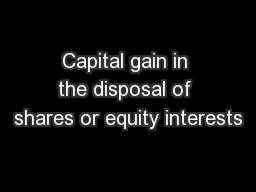

Is the seller a CT taxpayer that declares its income based on effective income or that transfers the shares to a related party Ordinary income CT Final Taxes Yes No Is the capital gain higher than 10 UTA approximately USD 8000 ID: 599877

Download Presentation The PPT/PDF document "Capital gain in the disposal of shares o..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Slide1

Capital gain in the disposal of shares or equity interests

Is the seller a CT taxpayer that declares its income based on effective income or that transfers the shares to a related party?

Ordinary income

(CT+ Final Taxes)

Yes

No

Is the capital gain higher than 10 UTA (approximately USD 8,000)?

No

Non taxable income

Yes

The total amount of the capital gain is subject to Final Taxes (on an accrued or perceived basis, at the election of the taxpayer) + possibility to resettle the GCT by declaring on an accrued basis

Are they shares from an open-stock corporation incorporated in Chile with stock market presence?

No

Was the disposition made in: (

i

) a Chilean stock exchange authorized by the Superintendency of Securities and Insurances (“SVS”) or (ii) in a takeover bid pursuant to the rules contained in Title XXV of Law No. 18,045 (“SML”) or (iii) in securities contribution pursuant to Article 109 of the Income Tax Law (“ITL”)?

Yes

No

Yes

Were the shares purchased: (

i

) in

a Chilean stock exchange authorized by the

SVS

or (ii) in a takeover bid pursuant to the rules contained in Title XXV of the SML or (iii) in a placement of shares of first issue or as a consequence of the company’s incorporation or of a capital increase or (iv) on the occasion of the exchange of public offering securities convertible into shares or (v) in a securities repurchase pursuant to Article 109 of the ITL?

No

Non taxable income

Yes

Are they shares from a corporation that were purchased before January 31, 1984? Is there no relationship between the seller and the buyer and is the sale of shares not a usual business of the seller?

Non taxable income

Yes

No

Notes:

This diagram includes the amendments introduced by Law No. 20,899.

Taxation applicable as from year 2017.The capital gain subject to taxes is determined by the difference between the tax cost of the shares or equity interests and the sale price. Resettlement is an option to distribute the capital gain in the fiscal years in which the shares or equity interests were held, up to a maximum of 10 years.Abbreviations: CT = Corporate Tax. GCT = Global Complementary Tax. Final Taxes = GCT or Withholding Tax.

*The content of this document is provided by Carey y

Cía

. For educational and informational purposes only and is not intended to be exact or complete, and should not be relied on as a substitute for legal advice. Carey y

Cía

. is not responsible for any consequences resulting from the action, lack of action or decision regarding the information contained in this publication.