II Post Development Stage Sale to Host Government I Development Stage GreenStreet Africa Development Company Ownership of All Intangible Assets Dist Gen System 1 Dist Gen System ID: 1037468

Download Presentation The PPT/PDF document "Host Government (Borrower)" is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

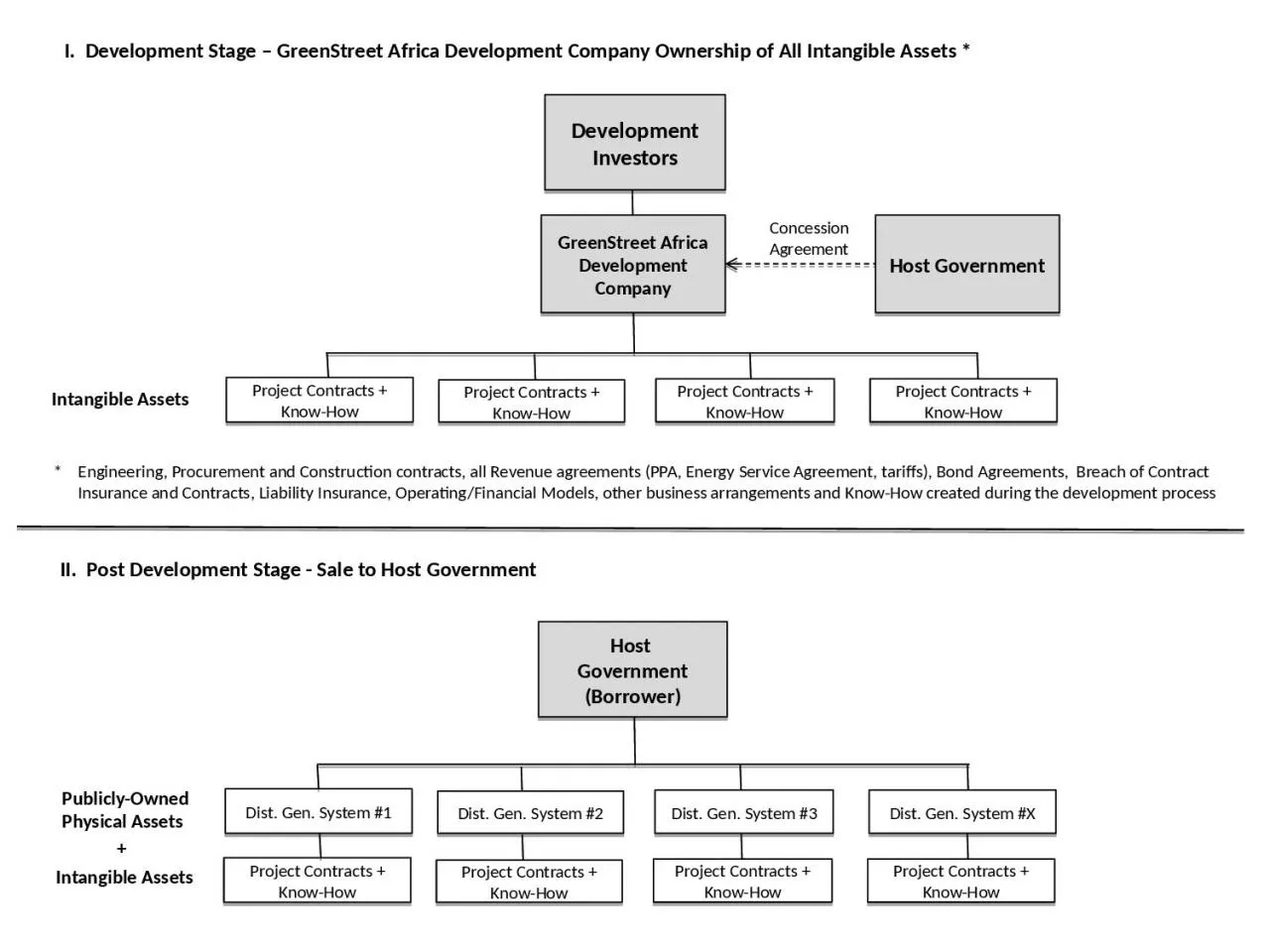

1. Host Government(Borrower)II. Post Development Stage - Sale to Host GovernmentI. Development Stage – GreenStreet Africa Development Company Ownership of All Intangible Assets *Dist. Gen. System #1Dist. Gen. System #2Dist. Gen. System #3Dist. Gen. System #XIntangible AssetsPublicly-OwnedPhysical Assets+Intangible AssetsProject Contracts + Know-HowProject Contracts + Know-HowProject Contracts + Know-HowProject Contracts + Know-HowDevelopment InvestorsProject Contracts + Know-HowProject Contracts + Know-HowProject Contracts + Know-HowProject Contracts + Know-How* Engineering, Procurement and Construction contracts, all Revenue agreements (PPA, Energy Service Agreement, tariffs), Bond Agreements, Breach of Contract Insurance and Contracts, Liability Insurance, Operating/Financial Models, other business arrangements and Know-How created during the development processGreenStreet Africa Development CompanyHost GovernmentConcessionAgreement

2. GreenStreet Africa’s Green Bond Mechanisms GreenStreet Africa plans to bring two proven - but never deployed in Sub-Saharan Africa - international green bond funding mechanisms to bear in its operations. A third option for funding in local currency is also being explored. The three mechanisms are described below. Diagrams and explanatory notes on the first two existing options follow.1) Sovereign Borrower The core structural elements of an international bond financing for a government-owned or government guaranteed borrower are shown below in Diagram 1: OPIC-Insured Structure. The basic principle is to insure against all payment defaults under the project’s permanent financing obligations by the sovereign, or state-owned purchaser. OPIC would supply this insurance in the form of a Non-Paying Sovereign insurance policy. Since the insurer is an AAA-rated gov’t agency, this allows for credit enhancement of the borrower up to a credit rating approaching that of the insurer. The transaction therefore receives better terms of leverage (100% up to $1B), tenor (out to 20 years) and pricing (based on expected rating of Aa2). The projects must be implemented directly by a government, or government-guaranteed entity, and must provide adequate return. Using this model, we envision that financed portfolios would include only generation assets supplying power to federally owned facilities. Two additional financing models shown below can accommodate different country situations, project structures and borrowing preferences. They may finance generating assets supplying power to both public and private facilities, but they will not include rural mini-grids or supply of power to households. 2) Private SPV or PPP FinancingWhere organizing a portfolio of publicly-owned generating assets is not practical or desirable, a private or PPP ownership model is possible. In this approach a privately- or PPP-owned SPV would be the borrower of the international bond issue proceeds with repayment cover provided by MIGA Breach of Contract (BOC) insurance. The same principles associated with OPIC insurance would apply, wherein MIGA would insure against payment default by the private or PPP borrower under the project’s permanent financing obligations. The MIGA BOC product covers 95% of loss out to 15 years. Other investors would provide the remaining 5%. This structure is shown in Diagram 2: MIGA-Insured Structure. 3) Local Currency FinancingGreenStreet is also interested in developing a Local Currency Bond Issue Structure (no diagram is presented). In this configuration, a multilaterally-backed insurer such as GuarantCo or InfraCredit would issue a partial repayment guarantee for sovereign or corporate bond issues that are denominated in local currency and used to finance Host Governments, Private Developers, or Commercial and Industrial (C&I) Borrowers that are seeking to build out distributed generation systems of scale.

3. Diagram 1

4. Diagram 2

5. Structural Notes for both OPIC and MIGA Structure DiagramsProvisional Payments under Indenture: Provisional payments sized at one year of debt service (interest) and payable by OPIC/MIGA once the Issuer exhausts the debt service reserve fund;OPIC or MIGA Insurance Policy: The OPIC or MIGA Policy covers expropriation, defined as (i) non-payment of an arbitral award (after commercially reasonable efforts to enforce) and (ii) denial of justice. OPIC insurance can cover 100% of insured principal for a term of 20 years. MIGA insurance provides for 95% coverage out to 15 years. Foreign Enterprise Support Agreement (FESA): As a condition of the OPIC Policy, Borrower must agree to FESA provisions and covenants, including compliance with certain OPIC policies and US & local laws. MIGA insurance carries similar FESA undertakings.Delaware Trust: The OPIC structure would utilize a U.S. based Trust as the issuer. OPIC requires the structure to comply with certain ownership and eligibility requirements: (a) The Issuer shall remain a statutory Delaware Trust; (b) the Issuer's Trustee shall be (i) a U.S. citizen, (ii) a U.S. corporation > 50% owned by U.S. citizens, or (iii) a corporation created under foreign law in which > 95% interest is owned under (i) or (ii). Each individual/entity meeting the criteria of (i), (ii), and (iii) is an “Eligible Person”; (c) As of the start of the OPIC Policy, at least 25% of the initial holders of the Notes must be Eligible Persons; and (d) the ultimate beneficial interest of the Insured shall at all times be more than 50% owned by an Eligible Person; The MIGA structure may accommodate a USD or Euro bond issuance in USA or Europe. Debt Service: Principal on the Notes will be paid under a sinking fund as Loan amortization payments are received under the Credit Agreement.Arbitration Agreement: Each of the parties shall (i) waive its right to a trial by jury and (ii) enter into the Arbitration Agreement to submit to expedited multi-party arbitration. Under the OPIC structure, arbitration will be conducted in New York City under the 6-month procedures of Article 30 of International Chamber of Commerce (ICC).Credit Agreement: Loan proceeds shall be funded on the issuance date as undisbursed loan proceeds and held until disbursed by the Issuer in the form of delayed draw term loans or reserves. Interest shall be payable monthly in arrears. Principal on a TBD quarterly schedule.Host Government (Borrower) or Privately or PPP Owned SPV (Borrower): Under the OPIC structure, Borrower is directly the host government sovereign credit. Under the MIGA structure, Borrower may not be the Host Government or 100% owned parastatal but can be either a Public Private Partnership including the Host Government, or a Private Developer. Mini-Grid/Distributed Generation Systems: The individual facilities of the Target Portfolio. In all funding structures, these facilities are public facilities, facilities owned by public-private partnerships, or facilities owned by private Commercial and Industrial (C&I) businesses. Rural mini-grids/distributed generation systems and Solar Home Systems (SHS) are excluded.5% of Capital Structure: Under the MIGA structure, 5% of total capitalization of the project portfolio(s) would be required to be funded by other TBD long-term investors/lenders. We anticipate a Development Finance Institution would provide this capital in the form of a subordinated loan at a to-be-determined rate of interest.