CA SANJEEV MALHOTRA FCA FCS ACMA LLB casanjeevmalhotragmailcom What is GST GST is a comprehensive value added tax on goods and services It is collected on value added at each stage of sale or purchase in the supply chain ID: 1027655

Download Presentation The PPT/PDF document "GOODS AND SERVICES TAX REFORM TO CONSOL..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

1. GOODS AND SERVICES TAXREFORM TO CONSOLIDATE INDIRECT TAXATIONCA. SANJEEV MALHOTRA FCA, FCS, ACMA, LL.B. casanjeevmalhotra@gmail.com

2. What is GST GST is a comprehensive value added tax on goods and servicesIt is collected on value added at each stage of sale or purchase in the supply chain No differentiation between Goods and Services as GST is levied at each stage in the supply chainSeamless input tax credit throughout the supply chain till tax is charged on final consumption valueAt all stages of production and distribution taxes are a pass through and tax is borne by the final consumerExemption limit to be uniform; to maintain value chain, exemption limit to cover only retail trade where transactions with ultimate consumers; this will ensure proper input tax accounting and rebating mechanism for exports.

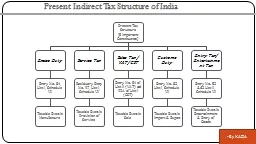

3. Present Indirect Tax Structure

4. Taxes to be Subsumed - Central

5. Taxes to be subsumed - State

6. Proposed Indirect tax Structure

7. GST exclusionsFollowing goods and services will not be part of proposed GST.Alcohol for human consumption. – State Excise plus VAT.Electricity – Electricity duty.Real Estate – Stamp duty plus property taxesPetroleum Products – (to be included from the date to be notified by GSTC)Tobacco Products – GST with Central Excise

8. IGST Adjustments and SettlementIGST credits can be adjusted for payment of IGST, CGST and SGST in sequence by importing dealer.The exporting state will transfer to centre the credits of SGST used for payment of IGST.The centre will transfer to the importing state the credits of IGST used for payment of SGST.Central Govt. will act as a clearing house and transfer the funds across states.

9. Process of RegistrationRegn. To be done within 30 days.PAN based 15 digits GSTIN to be allotted.Gross Annual turnover all over the country will be considered for regn. Or compounding Scheme.Compulsory registration for dealer of inter state sale or reverse charge cases.Unique identification no. for UN Bodies and Govt. deptt./ PSUsThe concept of ISD to continue for services.Suo moto registration in Enforcement cases.Multiple registration in same state allowed for Business Verticals.

10. Process of Registration… contdThe scheme of TRP and Facilitation Centres to be started.Compulsion to use DSC in case reqd. by any other law.Application in GSTN and printed Extract to be submitted to concerned tax authority within 30 days.GSTN will communicate with applicant and concerned tax authority.Approval or Rejection to be done within 3 working days otherwise it will be deemed approved by GSTN. Risk profiling of assessee to be done by tax authority and input in GSTN.

11. Process of PaymentOnline tax payments are required.Bank payments are restricted to Rs. 10,000/- per challan.Challan to be generated from GSTN which will have unique Common Portal identification no. (CPIN).CPIN will remain valid for 7 working days.The system will be integrated with RBI system.RBI will act as clearing house for Govt. Cheque bouncing – System will bar such assessees from this facility.

12. Process of RefundsGSTN to be integrated with Customs deptt.Refund application to be filed online.Refund application to be made within time limit. (1 year as present)Refund to be processed in a specified time limit.Stress on online verification of information.Pre and post audit of refunds to be carried out depending on amounts.Provision of interest on delay in payment of refund.

13. Way Forward for IntroductionConstitutional Amendment Bill to be passed.To be ratified by 50% of State Assemblies.Assent by PresidentConstitution of GSTC.GSTC to recommend GST law and Procedure.GST law to be introduced in Parliament and State Assemblies.GSTN (GST network) to be made operational.

14. Likely GST Administration CGST by Union department and SGST by State Revenue deptt.Cases with turnover upto 1.5 crores exclusively with State Revenue deptt.Union to deal only with Enterprises having Pan India presence.Routine matters with State and monitoring with Union.

15. ReturnsMandatory E filing of Returns.Returns to be made transaction wise.Returns up to a certain turnover limit will be assessed by one AA.

16. THANK YOU CA. SANJEEV MALHOTRA FCA, FCS, ACMA, LL.B.casanjeevmalhotra@gmail.com 9810995282