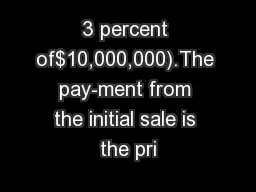

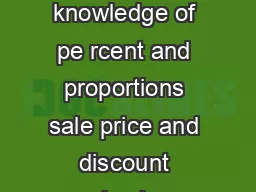

2 Starting leg Dealer Aborrower Mutual fundlender Treasury notesClosing leg Dealer A Mutual fund Treasury notes willing to accept any of a variety of Treasury and other related securities as colla ID: 822504

Download Pdf The PPT/PDF document "3 percent of$10,000,000).The pay-ment fr..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

3 percent of$10,000,000).The pay-ment fr

3 percent of$10,000,000).The pay-ment from the initial sale is the principal amount oftheloan;the excess ofthe repurchase price over the sale price isthe interest paid on the loan.As with a collateralized loan,the lender has possession ofthe borrowers securities duringthe term ofthe loan and can sell them ifthe borrowerdefaults on its repurchase obligation.general collateral RP is a repurchase agreement inwhich the lender offunds is willing to accept any ofa varietyofTreasury and other related securities as collateral.Theclass ofacceptable collateral might be limited to Treasurysecurities maturing in less than ten years or it might includeall Treasury and agency securities.The lender is concernedprimarily with earning interest on its money and havingpossession ofassets that can be sold quickly with minimaltransaction costs in the event ofa default by the borrower.Direct Trading and SettlementIn the textbookdescription ofa general collateral RP,theborrower and lender negotiate directly between themselvesthe principal amount,term,and interest rate,as well as theclass ofacceptable collateral.Sometime before 11 a.m.,theborrower identifies to the lender the securities within theagreed-upon class ofacceptable collateral that it will actuallydeliver,and thenas shown in Figure 1delivers thosesecurities against payment ofthe principal amount oftheloan.Securities deliveries must be completed by 3:30 p.m.,the closing time for transfers over the securities Fedwire,an electronic transfer system operated by the FederalReserve.At the end ofthe loan,the lender offunds deliversthe securities back to the borrower against repayment ofprincipal and payment ofinterest at the negotiated rate.Trading and Settlement in the Inter-Dealer MarketSome dealers make markets in RPs,quoting offer rates atwhich they are prepared to lend money for different periodsas well as bid rates at which they are prepared to borrow.Additionally,they transact amongst themselves to adjusttheir net borrowings,and the term structure oftheir net borrowings,to desired levels.However,the largest dealers donot,as in the textbook description,negotiate and settle reposdirectly when they transact with their competitors.Instead,they use inter-dealer brokers (IDBs) to disseminate theirbids and offers anonymously over electronic communicationsystems and they settle their transactions through the IDBsand through FICC.Settlement ofan RP that is arranged by a broker betweentwo FICC members differs from the textbook description ofa repo settlement in two important respects.First,the brokeris involved in the settlement at the start ofthe repo.Asshown in the top panel ofFigure 2,the borrowing dealerdelivers its securities to the broker,rather than directly to thelender,against payme

nt ofthe principal amount ofthe borrowin

nt ofthe principal amount ofthe borrowing.The broker then redelivers the securities to thelender against payment ofthe same principal amount.Thismore costly,two-step settlement process is necessary to preserve the anonymity ofthe borrower and lender.Second,the settlement at the end ofthe RP goesthrough FICC.FICC nets the settlement obligations ofeachofthe three partiesthe borrower,the lender,and thebrokerwith other obligations ofeach ofthose parties toreceive and deliver the same securities on the terminationdate ofthe RP.If,for example,the lender (dealer B inFigure 2) happens to be a buyer (from another FICC member)of$7 million principal amount ofthe same series ofTreasury notes,it would have a net obligation to deliveronly $3 million ofthe notes ($3 million = $10 million ofnotes due to be returned to dealer A,less $7 million ofthenotes due to be received in settlement ofits purchase).TheCURRENTISSUESINECONOMICSANDFINANCE2Starting legDealer A(borrower)Mutual fund(lender)Treasury notesClosing legDealer AMutual fundTreasury noteswilling to accept any of a variety of Treasuryand other related securities as collateral.www.newyorkfed.org/rmaghome/curr_issbroker always drops out ofthe settlement process becauseit has offsetting obligations to receive $10 million ofthenotes from dealer B and to deliver $10 million ofthe notesto dealer A.In the simple case in which the borrower and lenderhave no other obligations to receive or deliver the samesecurities on the same day,the lender delivers the securi-ties that collateralized the RP to FICC against payment byFICC ofthe principal and interest on the borrowing,andFICC delivers the securities to the borrower against payment ofthe same sum.This is shown in the lower panelofFigure 2.When the borrower and lender do have otherobligations,settling the closing leg ofthe RP through FICCis cheaper and more efficient than settling through the broker because ofthe efficiencies ofnet settlement(described in Fleming and Garbade [2002]).The startingleg ofthe RP is not settled through FICC because,outside ofthe GCF Repo facility described below,FICC does notprovide for net settlement oftransactions that settle on theday they are negotiated.Transaction Costs ofInter-Dealer TradingA variety oftransaction costs limit the liquidity ofthe inter-dealer repo market and,therefore,the liquidity ofthe largerdealer-customer repo market.First,because the starting legsofinter-dealer RPs have to be settled on an individual,trade-by-trade basis,inter-dealer RPs are more costly to settle thantransactions in which the parties have to settle only their netobligations.Ifa dealer agrees at 8 a.m.to borrow $100 millionovernight through broker X and at 9 a.m.agrees to lend$100million overnight through brok

er Y,it has to settle eachRP separately,

er Y,it has to settle eachRP separately,delivering securities to broker X againstreceiving $100 million and receiving securities from broker Yagainst paying $100 million.A second transaction cost is the relatively early (in theday) loss ofthe borrowers option to deliver any ofa varietyofsecurities.A dealer borrowing funds on a general collat-eral RP has to identify by about 11 a.m.the securities that itintends to deliver.As soon as it does so,it becomes obligatedto deliver those specific securities.Ifthe dealer identifiessecurities that it expects to receive later in the day but thatultimately fail to arrive,the dealer has to go back to thelender and request that it agree to accept different securities.The possibility that repo settlements may have to be renego-tiated adds to the costs ofmaking a two-way market in general collateral RPs.A third transaction cost is the cost to a lender ofaccom-modating a borrowers request to substitute collateral on aterm,or multiple-day,repo.A dealer that borrows money ona term RP will sometimes request that it be allowed to provide different collateral ifit identifies an opportunity tosell outright some or all ofits original collateral at a favor-able price.Collateral substitution requires two settlements,one when the lender delivers the original collateral back to the borrower against payment,and the second when the borrower delivers the new collateral to the lender,alsoagainst payment.A dealer lending money on a general col-lateral RP bears additional expenses whenever a borrower substitutes collateral.GCF RepoGCF Repo was designed to reduce transaction costs andenhance liquidity in the inter-dealer repo market by allow-ing for netting in both legs ofthe settlement process,byextending the time interval before a borrowers deliveryoption is lost,and by reducing the cost ofcollateral substitu-tion.This section explains how GCF Repo works and how itStarting legDealer A(borrower)BrokerDealer B(lender)Treasury notesTreasury notes$10, 000,000$10, 000,000Closing legDealer AFICCDealer BTreasury notesTreasury notes$10, 000,833$10, 000,833liquidity of the inter-dealer market and,therefore, the liquidity of the largerdealer-customer repo market. accomplishes these objectives.For expository purposes,wewill describe trading in GCF Repo on all Treasury bills,notes,and bonds (all Treasury issues) by dealers that clearthrough JPMC.Trading in GCF RepoTrading in GCF Repo starts each morning at about 7:30 a.m.when dealers begin to submit bids and offers for money to inter-dealer brokers that are members ofFICC.(There isno provision at this time for direct trading in GCF Repobetween FICC members.) One dealer might,for example,bid2.15 percent for money over a two-week term and anotherdeale

r might offer to lend for the same term

r might offer to lend for the same term at 2.20 percent.When a dealer signals to an IDB that it is willing to borrow or lend on the terms proposed by another dealer,the IDBbrokering the transaction reports the details ofthe trade to FICC.Trading in GCF Repo stops at 3:30 p.m.when thesecurities Fedwire closes.Settlement ofGCF Repo transactions is designed to mini-mize costly movements ofsecurities by allowing for nettingin the settlement process.At 3:45 p.m.,FICC computes theobligation ofeach dealer to lend or borrow money for one business day or longer as a result ofthe GCF Repocontracts that it negotiated during the day and (as explainedbelow) the continuing term GCF Repo contracts that it negotiated on earlier days.Each dealer is informed eitherthat (a) it is a net borrower and is obligated to deliverTreasury collateral to FICC against payment ofthe aggregateprincipal amount ofits net borrowing,or that (b) it is a netlender and is obligated to receive Treasury collateral againstpayment ofthe aggregate principal amount ofits net loan.Settlement ofGCF Repo is also designed to preserve foras long as possible the borrowers option to choose whatcollateral to deliver.A dealer that clears through JPMC andis a net borrower on GCF Repo on all Treasury issues hasuntil 4:30 p.m.to deliver Treasury bills,notes,and/or bondsofits choosing to an FICC account at JPMC against pay-ment ofthe principal amount ofits net borrowing.JPMCis responsible for verifying that the securities are in factTreasury securities and that they have a market value(including any accrued interest) at least as large as theprincipal amount ofthe dealers net borrowing.The bor-rower does not have to give any advance notification ofthespecific collateral that it plans to deliver,so its option tochoose which securities to deliver survives well past thetime when collateral is assigned for conventional repos.The securities transferred to FICCs account are redeliv-ered to other dealers that also clear through JPMC and thatare net lenders against payment ofthe principal amounts oftheir respective net loans.The transfers ofsecurities fromnet borrowers to FICCs account at JPMC,and the transfersofsecurities from FICCs account to net lenders,occurentirely on the books ofJPMC and do not require anyFedwire transfers.The aggregate net borrowing ofall ofthedealers that are net borrowers and clear through JPMC isidentical to the aggregate net loan ofall ofthe dealers thatare net lenders and clear through JPMC because every GCFRepo transaction involves a borrowing and a loan ofidenti-cal size by parties that clear through the same bank.Thus,the total payments received by FICC in its JPMC accountequal the total payments disbursed by FICC from its JPMCaccount.All ofthe foregoin

g deliveries and payments are reversedbe

g deliveries and payments are reversedbefore the opening ofthe securities Fedwire at 8:30 a.m.thenext morning.Borrowed funds are returned to lenders andcollateral securities are returned to borrowers.Except forinterest payments (described below),the reversals constitutefinal settlement ofGCF Repos terminating that day.The morning reversals are important to dealers borrowingon continuing term RPs because they restore a borrowerscontrol over its collateral,giving it access to securitiesthatCURRENTISSUESINECONOMICSANDFINANCE4important to dealers borrowing on continuingterm RPs because they restore a borrowersunrelated sales. Settlement of GCF Repo transactions isdesigned to minimize costly movements ofsettlement process. www.newyorkfed.org/rmaghome/curr_issmight be needed to settle unrelated sales.The morningreversals eliminate the costs ofrequesting and effecting specific collateral substitutions because borrowers regaincontrol over alloftheir collateral through securities andfunds transfers that take place entirely on the books oftheirclearing bank.Ofcourse,ifa dealer committed to borrow on a term RPthat is not terminating,its borrowing must be renewed,thatis,the morning reversal must itselfbe reversed.Similarly,ifa dealer committed itselfto lend on a continuing RP,its loan must be renewed.Thus,FICC reinstates all continuingborrowing and lending commitments immediately followingeach morning reversal.Any additional commitments negoti-ated during the day are combined with the reinstated commitments in the 3:45 p.m.calculation ofeach dealersnet obligation to borrow or lend that day.Ifthe dealer is a net borrower at 3:45 p.m.,it is obligatedto deliver Treasury collateral to FICC against payment oftheaggregate principal amount ofits net borrowing.It does not,however,have to deliver the same securities that it receivedin the morning (assuming it had been a net borrower on thepreceding day).Ifit needed some ofthose securities to settletwo-day GCF Repo on Treasury collateral with dealer BSometime after 3:45 p.m. and before 4:30 p.m. onJune 1, dealer A delivers $100 million of Treasury secu-terminating on June 3. (A System Repo Rate is FICCs($5,972.22 = $5,833.33 + $138.89). Dealer B receivesdealer A delivers $100 million of Treasury securities toits reinstated commitment to borrow.Additionally, dealer A receives back the $5,972.22itself, means that dealer As payment of $5,972.22 thefor the dealer. In particular, the money was returned andmoney. The disbursement of the $5,972.22 on June 2merely served to facilitate the return of dealer As collat-RP on that day.These payments are included in each dealers daily funds-onlysettlement.See Fixed Income Clearing Corporation,Government SecuritiesDivision,Rulebook (January

14,2003),Rule 13Funds-Only Settlement.T

14,2003),Rule 13Funds-Only Settlement.The Government Securities Division Rulebook is posted atttp://www.ficc.com/gov/other.docs/rules/r&#xh23.;çules.pdf.unrelated sales,it can continue its borrowing using othersecurities as substitute collateral.In this way,GCF Repomakes collateral substitution an entirely transparentprocess.As explained earlier,interest on a textbook RP is included aspart ofthe invoice price due upon return ofthe collateral atthe close ofthe RP.Interest on GCF Repo is also paid atmaturity but,in addition,there are daily accrued interestand mark-to-market payments associated with the reversalsdescribed above.These payments protect the financial inter-ests ofboth borrowers and lenders.They are,therefore,acrucial aspect ofGCF Repo.In order to justify the return ofa borrowers collateralagainst payment ofonly the original principal amount oftheborrowers RP,FICC requires that the borrower pay accruedinterest on its borrowing and make (or receive) a mark-to-market payment to account for the decline (or rise) in themarket value ofits contract due to changes in GCF Reporates since the contract was negotiated.To preserve the con-vention that interest on GCF Repo is paid in full at maturity,both ofthe foregoing payments are returned the followingday with interest at the overnight repo rate.The box presentsa numerical example.GCF Repo Compared with Conventional RepoGCF Repo offers dealers several important advantages overconventional general collateral repo:GCF Repo transactions settle on a net rather than grossbasis,reducing movements offunds and securities andthereby lowering settlement costs.In 2002,for example,average daily net settlement volume ofGCF Repo was$101 billion while average daily gross settlement volumewas $721 billion.GCF Repo settles entirely on the books ofthe clearingbanks and does not require movement ofTreasury secu-rities on Fedwire.GCF Repo can thereby accommodatesettlement later in the day,allowing a borrower ofmoneyto defer deciding what securities to use as collateral until4:30 p.m.GCF Repos are reversed every morning and renewed everyafternoon.A borrower ofmoney can therefore use collat-eral securities to settle unrelated transactions during theday and can easily change collateral securities withoutexceptional provisions for collateral substitutions.ConclusionGCF Repo is a recent innovation in the market for repurchaseagreements that provides several advantages to dealers overconventional general collateral RPs.In particular,GCF Repoprovides for netting in settlement,accommodates settlementlater in the day,and allows collateral to be easily substituted.These features reduce transaction costs,enhance liquidity,and facilitate the efficient use ofcollateral.The benefits ofGCF Repo have

contributed to its rapid growth and expl

contributed to its rapid growth and explainwhy it has captured such a large share ofthe brokered gen-eral collateral repo market.Notes2.Ingber (2003) recounts the development of GCF Repo; see also Taylor(DTCC), which also owns the Depository Trust Company. The GovernmentSecurities Division of FICC is the successor to the Government Securities3.The figures double count the actual volume of transfers of funds and secu-4.The Bond Market Association (1998) recommends that borrowers adviseCURRENTISSUESINECONOMICSANDFINANCE6Interest on GCF Repo is . . . paid atmaturity but, in addition, there are dailyand lenders. www.newyorkfed.org/rmaghome/curr_issThe views expressed in this article are those ofthe authors and do not necessarily reflect the position ofthe FederalReserve Bank ofNew York or the Federal Reserve System.Michael J.Fleming is a research officer and Kenneth D.Garbade a vice president in the Capital Markets Function ofthe Research aMarket Analysis Group.Current Issues in Economics and Financeis published by the Research and Market Analysis Group ofthe Federal ReserveBank ofNew York.Dorothy Meadow Sobol is the editor.Back issues ofCurrent Issues in Economics and Financeare availableat http://www.newyork fed.org/rmaghome/curr_iss/5.Fleming and Garbade (2002) describe the details of delivery and payment6.Dealers actually quote bid rates for (borrowing) collateral against lendingmoney and offer rates for (lending) collateral against borrowing money. We7.The brokers role in settling the starting leg of an RP was made possible byobligations. This guarantee, as well as other aspects of repo settlements, is 8.For reasons that will become evident shortly, dealers that clear throughthrough BoNY. FICC sponsors GCF Repo trading in four other classes of col-Mortgage Corporation (Freddie Mac), (3) fixed-rate mortgage-backed secu-9.A net borrower can deliver securities after 4:30 p.m. but it is then subject to10.Between June 1999 and March 2003, FICC sponsored trading in GCF RepoReferences November 2. �agrees/revrepotrdprcguidlnes.pdf, Moved to the Front Burner: Settlement Fails in the Treasury Market afterEconomic Policy Review, July 25. . . 2003. Repo Market Is Hit by Limits on a Top Product,www.newyorkfed.org/rmaghome/curr_issBy subscribing to our free Electronic Alert service you receive an e-mail whenever new publications are posted on ourwebsite.You can then link directly to the publications.Visit http://www.newyorkfed.org/rmaghome/subscribe/subscribe.html� to join the service.that reduces transaction costs, enhances liquidity, and facilitates the efficient use of collateral.epurchase agreements (reposor RPs)play a crucial role in the efficient allocationwww.newyorkfed.org/rmaghome/curr_iss