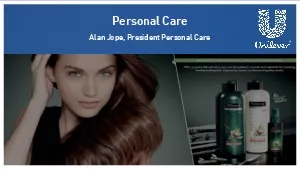

Alan Jope President Personal CareOur Business283820082015Personal Care as of group salesA Transformed BusinessAn increasing part of UnileverSignificant shift in scale11 bn20 bn20082015Personal Care T ID: 867300

Download Pdf The PPT/PDF document "Personal Care" is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

1 Personal Care Alan Jope, President Pers

Personal Care Alan Jope, President Personal Care Our Business 28% 38% 2008 2015 Personal Care as

2 % of group sales A Transformed Business

% of group sales A Transformed Business An increasing part of Unilever Significant shift in scal

3 e € 11 bn € 20 bn 2008 2015 Personal

e € 11 bn € 20 bn 2008 2015 Personal Care Turnover Our Personal Care categories Global Le

4 ading Position Strong Challenger ORA

ading Position Strong Challenger ORAL CARE SKIN CARE DEODORANTS SKIN CLEANSING HAIR Our Top B

5 rands and Countries Top 15 Brands Top 15

rands and Countries Top 15 Brands Top 15 Countries India Argentina France Brazil Philippines Russ

6 ia Indonesia Mexico Germany China Japan

ia Indonesia Mexico Germany China Japan Vietnam USA UK Thailand Personal Care Category Role ` Ste

7 p up profitability Scale household care

p up profitability Scale household care Grow the core Build premium Accelerate growth Strong cash

8 flow Grow Ice Cream ROIC Accelerate tea

flow Grow Ice Cream ROIC Accelerate tea whole person from head to toe health & beaut

9 y 10% 5% 7% Unilever Market CAGR% +6.4%

y 10% 5% 7% Unilever Market CAGR% +6.4% Competitive Growth Global PC Competitor USG, January

10 - September 2016 Unilever PC & Market CA

- September 2016 Unilever PC & Market CAGR, 2008 - 2015 1 2 3 4 5 6 Top 5 Global Competitors U

11 nilever PC Quarterly USG, 2013 - 2016 Q

nilever PC Quarterly USG, 2013 - 2016 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 2013 2014 201

12 5 2016 Our Growth Strategy Personal Care

5 2016 Our Growth Strategy Personal Care Growth Strategy CORE CONNECTED 4 GROWTH MARKET DEVELOPM

13 ENT PREMIUMISATION HIGH GROWTH CONSUMER

ENT PREMIUMISATION HIGH GROWTH CONSUMER SEGMENTS ON - TREND BENEFITS PRESTIGE AGILITY IN THE CO

14 NNECTED WORLD MORE GLOBAL, MORE LOCAL EX

NNECTED WORLD MORE GLOBAL, MORE LOCAL EXPANSION WINNING CHANNELS Brush Day & Night Market Develo

15 pment Hair Regimen Deodorants Daily Usag

pment Hair Regimen Deodorants Daily Usage Premiumisation Ranges Formats Brands Dove Men+Care Dol

16 lar Shave Club High Growth Consumer Segm

lar Shave Club High Growth Consumer Segments: Men Axe Innovation Communication High Growth Consum

17 er Segments: Muslim Consumers On Trend B

er Segments: Muslim Consumers On Trend Benefits Naturals Therapeutics Winning Channels E - Commer

18 ce Drugstores Murad Expansion: Prestige

ce Drugstores Murad Expansion: Prestige Kate Somerville Dermalogica Connected 4 Growth More Globa

19 l: Category Expertise & World Class Tech

l: Category Expertise & World Class Technology More Local: Consumer Insight & Execution Vaseline

20 Example Pitch Co - creation Centre In

Example Pitch Co - creation Centre In - house Creative Agility in the Connected World Capabilit

21 ies Connected 4 Growth Strategy for Grow

ies Connected 4 Growth Strategy for Growth Personal Care Strong Performance 1 2 3 4 5 6 Top 5 Glo

22 bal Competitors USG, January - Septemb

bal Competitors USG, January - September 2016 Personal Care Alan Jope, President Personal Care