Victoria Chick Note A Perspective not The Perspective Big field with several approaches Cannot cover everything PostKeynesian Joan Robinson AEA meetings 1971 where she gave the Ely Lecture The second Crisis in Economic Theory came to meeting called by Paul Davi ID: 248013

Download Presentation The PPT/PDF document "Money in the Economy: A Post-Keynesian P..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Slide1

Money in the Economy: A Post-Keynesian PerspectiveVictoria Chick

Note: ‘A Perspective’ not ‘The Perspective’. Big field with several approaches. Cannot cover everything. Slide2

‘Post-Keynesian’Joan Robinson, AEA meetings 1971 (where she gave the Ely Lecture, ‘The second Crisis in Economic Theory’ ) came to meeting called by Paul Davidson –scholars who took Keynes seriously

‘Keynesians’ still influential, though monetarists on

th

rise

She suggested ‘post-Keynesian’Slide3

Mill and Hayek on money'There cannot ... be intrinsically a more insignificant thing, in the economy of society, than money' J S Mill

'...

the task of monetary theory is a much wider one than is commonly assumed; that its task is nothing less than to cover a second time the whole field which is treated by pure theory under the assumption of barter... The first step ... is to release monetary theory from the bonds which a too narrow conception of its task has created.' F A Hayek, Prices and Production p 110, quoted by Keynes in his review, CW XIII, p. 254.Slide4

Keynes on monetary theoryIn the standard theory of Keynes's time (and ours) money is 'a convenient means of effecting exchanges - [it is] an instrument of great convenience, but transitory and neutral in its effect. ... [in what] might be called ... a real-exchange economy. The theory which I desiderate would deal, in contradistinction to this, with an economy in which money plays a part of its own and affects motives and decision and is, in short, one of the operative factors in the situation, ... [I]t is this which we ought to mean when we speak of a monetary economy

. Keynes

, 'A Monetary Theory of Production', CW XIII, pp 408-9.Slide5

A money production economy in contrast to a real exchange economy

Money in Keynes’s

General Theory

: p

ervasive

influence:

Labour bargains for money wages

Saving = putting money into financial assets

The rate of interest is a rate of return in the form of money on an asset denominated in money

Firms seek profit ( = sales minus money-costs

)

Marx: Barter economy: C – M – C

Money economy: M – C – M

’Slide6

Production, time, uncertainty and moneyProduction takes time. Goods are produced for a ‘market’ that will exist some time in the future.

The future is irreducibly uncertain. Producers cannot ‘know’ their market. Neither can workers know the real value of their wages.

Money allows us to keep our options open. It ‘lulls our disquietude’ (Keynes). It also creates uncertainty. Intentions

hidden

.Slide7

Liquidity preference A theory of the rate of interest (r/

i

) based on the desire to hold liquid assets versus the return from going less liquid.

A liquid asset is ‘more certainly realisable at short notice without loss’ (Keynes, Treatise on Money). Three dimensions: probability, time, price variation.

Can see r/

i

as a liquidity premium or reward for parting with liquiditySlide8

Incentives to liquidity

Transactions, precaution, speculation

Transactions: obvious : money, by convention or

govt

sanction (acceptance in payment of taxes, protection of contracts in law) serves as means of final settlement.

Precaution – keeping one’s options open

Speculation: the liquid assets help avoid losses on less liquid assets.

Can be generalised to a theory of asset prices, including real assets (GT

Ch

17). c, q, l, aSlide9

Essential properties of moneyLow elasticity of production ‘so far as the power of private enterprise in concerned’ (GT p. 230), and a low elasticity of substitution. (GT p. 231)

Translated: There’s nothing quite like money and ‘the public’ cannot make it when they want more of it. Only the banks and the monetary authorities can do that.Slide10

The rate of interest, investment , employment and economic prosperity.

Why is the r/

i

important? Important in determining investment, which is the engine of growth.

I = I(r/

i

, expectations of future profit). Influence of r/

i

can be swamped by volatile expectations.

New investment is (in Keynes’s theory) financed by bank credit. New money in the system.Slide11

In other words‘The rate of interest on money plays a peculiar part in setting a limit to the level of employment, since it sets a standard to which the marginal efficiency of a capital asset must attain if it is to be newly produced.’ (GT p. 222

)Slide12

Money is not neutralS/he who has money or can borrow it can do what s/he wishes. Money determines the shape of the economy.

Look at today’s British economy, with its preponderance of financial activity, much of which supports asset prices (

esp

house prices) instead of investment and production. Slide13

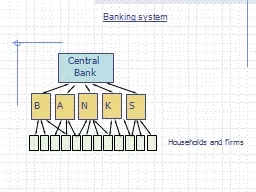

The monetary authorities and the banks IHow do banks create money?

A bank balance sheet:

Assets

l

iabilities

liquid assets deposits

‘investments’ equity capital

loansSlide14

The monetary authorities and the banks IICan the central bank control money?

accommodationists

and

structuralists

Banks, credit and economic growth.

should the banks determine the shape of the economy?

Banks and financial stabilitySlide15

Modern Monetary TheoryQuite wrong and nothing new? (Palley

)

Govt spends and then claws back money in tax.

Acceptability in payment of tax determines what is money.

Govt should act as Employer of Last Resort

Interest rates should be kept at zero

Full employment can be achieved w/o inflationSlide16

Circuit theoryBank credit provides working capital to pay wages. Wages used to but goods, Revenue from sales of goods used to pay back bank loans.

Circuit starts from nothing. How is it that banks and firms exist? Another circuit: yesterday’s sales pay

today’s wages.Slide17

EvaluationFew followed the GT. Textbook macro limits role of money to determining prices. Neutral. No uncertainty. Fantasy world.

Some details of treatment in GT out of date. Banks no longer lend for investment. First consumer loans, then mortgages, financial speculation.

Whoever can borrow from banks

pre-empts

resources.

LP still a valuable idea. GFC and liquidity illusion. Money morphs. Watch shadow banking..