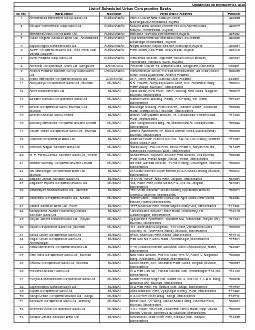

The definition of a bank varies from country to country Under English common law a banker is defined as a person who carries on the business of banking which is specified as conducting current accounts for his customers paying cheques drawn on himher and collecting cheques for hisher custome ID: 1029912

Download Presentation The PPT/PDF document "Meaning and Nature of Bank A bank is an ..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

1. Meaning and Nature of Bank A bank is an institution, usually incorporated with power to issue its promissory notes intended to circulate as money (known as bank notes); or to receive the money of others on general deposit, to form a joint fund that shall be used by the institution, for its own benefit, for one or more of the purposes of making temporary loans and discounts; of dealing in notes, foreign and domestic bills of exchange, coin, bullion, credits, and the remission of money; or with both these powers, and with the privileges, in addition to these basic powers, of receiving special deposits and making collections for the holders of negotiable paper, if the institution sees fit to engage in such business.

2. The definition of a bank varies from country to country. Under English common law, a banker is defined as a person who carries on the business of banking, which is specified as: conducting current accounts for his customers, paying cheques drawn on him/her, and collecting cheques for his/her customers.

3. Origin of the Word ‘Bank’ The name bank is derived from the Italian word banco “desk/bench”, used during the Renaissance by Florentine’s bankers. These bankers used to make their transactions above a desk covered by a green tablecloth. There are traces of banking activity even in ancient times. In fact, the word traces its origins back to the ancient Roman Empire, where moneylenders would set up their stalls in the middle of enclosed courtyards called macella on a long bench called a bancu. It is from here that the words banco and bank are derived. As a money changer, the merchant at the banco did not invest much money but merely converted the foreign currency into the only legal tender in Rome that is the Imperial Mint.

4. 1.2 Characteristics of Indian Banking System From the meaning and nature of banks mentioned in earlier section, the characteristics/features of a bank may be listed as follows: 1. Dealing in Money: Bank is a business activity which deals with other people’s money i.e. getting money from depositors and lending the same to borrowers. 2. Banking Business: A bank is a financial institution which does banking activities of selling financial services like home loans, business loans, lockers, fixed deposit etc. In order to enable people to confirm that it is a bank and is dealing in money, for easy identification, a bank should add the word “bank” as its last name. 3. Acceptance of Deposit: A bank accepts money from the people in the form of deposits where there is an obligation to refund deposits on demand or after the expiry of a fixed tenure as they feel it is a safest place to deposit money. 4. Lending Money: A bank provides advance money in the form of loans to needy persons for promotion & development of business, purchase of home, car etc.

5. 5. Easy Payment and Withdrawal Facility: Payment & Withdrawal of money can be made through issuance of cheques & drafts, ATM, Online Fund Transfer without the need for carrying money in hand. A bank provides easy payment and withdrawal facility to its customers in the form of cheques, drafts, ATM’s and ETF. 6. Motive of Profit with Service Orientation: A Bank has a motive of employing funds received as deposits from the public in a profitable manner with service oriented approach. 7. Linking Bridge: Banks collect money from those who have surplus money and give the same to those who are in need of money. It acts as a trust/custodian of funds of its customers. Notes A bank acts as a bridging link between borrowers and lenders of money. 8. Ever increasing Functions: Banking is an evolutionary concept. There is continuous expansion and diversification as regards the functions, services and activities of a bank. 9. Banking Business: A bank’s main activity should be to do business of banking which should not be subsidiary to any other business. 10. Name Identity: A bank should always add the word “bank” to its name to enable people to know that it is a bank and that it is dealing in money

6. 1.3 Functions of Commercial Banks The functions of commercial banks are divided into two categories: (i) Primary functions, and (ii) Secondary functions including agency functions. 1.3.1 Primary Functions The primary functions of a commercial bank include: (a) Accepting deposits; and (b) Granting loans and advances;

7. Secondary Functions Besides the primary functions of accepting deposits and lending money, banks perform a number of other functions which are called secondary functions. These are as follows: (a) Issuing letters of credit, travellers’ cheques, circular notes etc; (b) Undertaking safe custody of valuables, important documents, and securities by providing safe deposit vaults or lockers; (c) Providing customers with facilities of foreign exchange; (d) Transferring money from one place to another; and from one branch to another branch of the bank; (e) Standing guarantee on behalf of its customers, for making payments for purchase of goods, machinery, vehicles etc; (f) Collecting and supplying business information; (g) Issuing demand drafts and pay orders; and (h) Providing reports on the credit worthiness of customers