TIN 1 Registration Number TIN is to be entered in this field by all de alers liable to file return in F orm VAT 10 2 It should be exactly as per the Registration Certificate issued to the dealer 3 If TIN is wrong system will not accept the return 573 ID: 13225

Download Pdf The PPT/PDF document " BoxColumn Instructions to f..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

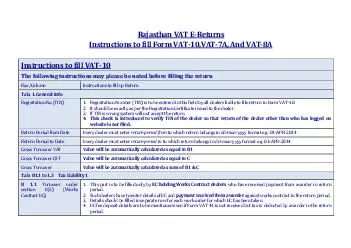

Rajasthan VAT E - Returns Instructions to fill Form VAT - 10 ,VAT - 7A, And VAT - 8A Instructions to fill VAT - 10 The following instructions may please be noted before filling the return Box/Column Instructions to fill up Return Tab: 1. General Info Registration No.(TIN) 1. Registration Number (TIN) is to be entered in this field by all de alers liable to file return in F orm VAT - 10. 2. It should be exactly as per the Registration Certificate issued to the dealer. 3. If TIN is wrong system will not accept the return. 4. This check is introduced to verify TIN of the dealer so that return of the dealer other than who has logged on website is no t filed. Return Period from Date Every dealer must enter return period from to which return belongs in dd - mon - yyyy format e.g. 01 - APR - 2014 Return Period to Date Every dealer must enter return period to to which return belongs in dd - mon - yyyy format e.g. 01 - APR - 2014 Gross Turnover VAT Value will be automatically calculated as equal to B1 Gross Turnover CST Value will be automatically calculated as equal to C Gross Turnover Value will be automatically calculated as sum of B1 & C Tab: B1.1 to 1.3 Tax Liability 1 B 1.1 Turnover under section 8(3) (Works Contract EC) 1. This part is to be filled only by EC holding Works Contract dealers who have received payment from awarder in return period. 2. Such dealers have to enter details of EC and payment received from awarder against works contract in the return period. 3. Details should be filled in separate row for each work order for which EC has been taken. 4. EC fee deposit details are to be mentioned even if Form VAT 41 is not received but tax is deducted by awarder in the return period. B 1.2 Turnover under section 5(1) of RVAT Act (Composition Schemes) 1. This part is to be filled only by dealers who have opted for payment of tax in lump sum for notified goods u/s 5 and also have other taxable turnover. 2. Such dealers have to enter details of turnover and lump sum amount payable in lieu of tax during return period for each class of goods in separate rows. 3. Dealers dealing exclusively in goods on which option to pay tax in lump sum has been exercis ed under section 5 are required to file VAT 11 . B 1.3 Turnover under section 3(2) (in case opt out of section 3(2)) 1. This part is to be filled only by dealers who have opted out of section 3(2) in the return period . 2. Such dealers have to p rovide the details of turnover and tax payable from the beginning of the financial year up to the date of opting out of section 3(2) as per RVAT rule 18(11). Tab: B1.4 to 1.7 Tax Liability 2 B 1.4 Sale of goods taxable at MRP (First sale within the state) 1. This part is to be filled only by dealers (manufacturer or importer) who have opted to pay tax at full rate on the maximum retail price . 2. Such dealers have to enter the details of sale price, turnover at MRP and tax payable at MRP on goods for which dealers have opted to pay tax on the maximum retail price as per RVAT rule 18(7). 3. Entries should be made in separate row for each class of goods for which tax is paid on MRP. B 1.5 Taxable Sales 1. In this part dealers have to enter details related to turnover, tax rate, commodity and amount of tax payable on taxable sales other than as mentioned in B1.1 to 1.4 and B 1.5A . For the sales at unit basis, the rate will be auto populated based on Commodit y. Thus, for such cases first select commodity. 2. As far as possible, entries should be made in separate row for each commodity. In case a commodity is not mentioned in drop down list, the commodity and applicable tax rate may be mentioned in others column. Taxable sales mentioned in B 1.4 and B 1.5 must be equal to the sum of sales referred to in Part I and Part II of VAT 08A. B 1.5a Tax on Sales made by commission agent on behalf of principal against Form VAT 36 1. This part is to be filled only by dealer a cting as Principal . 2. Such dealers have to enter details of tax payable by them on sales made by commission agent on behalf of principal against form VAT 36 as per RVAT rule 37. B 1.6 Sales return of taxable goods within state under rule 22(1)(c) (other than return period) 1. In this part dealers have to enter details related to turnover, tax rate, commodity and amount of tax payable on sales return of goods other than in the return period . 2. Please ensure that such return of goods should be within a period of six months from the date of invoice thereof . 3. You shall have to provide details of sales return in sales retu rn register under Part D of VAT - 10A . B 1.7b Tax on sales other Value will be automatically calculated as (1.4 + 1.5) - 1.6 than above B 1.7 Output Tax due Value will be automatically calculated as 1.5a + 1.7b Tab: B1.8 Turnover not liable to be taxed B 1.8 Turnover not liable to be taxed Dealers have to enter details of turnover which is exempted from payment of tax – 1.8.1 Dealers working as subcontractors having turnover which is exempted under Rule 22A by virtue of main contractor having taken EC have to fill details of such turnover. For each EC of contractor, entries are to be done in separate rows. 1.8.2 In this part dealers have to enter the turnover of goods which are exempted under Schedule – I. 1.8.3 In this part dealers have to enter the turnover of goods which are exempted under Schedule – II. 1.8.4 In this part dealers have to enter the turnover related to sales of goods for promotion of SEZ or Export u/s 8(4). 1.8.5 In this part dealers have to enter the turnover of goods which are purchased & sold outside state. 1.8.6 In this part dealers have to enter the turnover of goods which are taxable at first point and have already suff ered tax. 1.8.7 In these part dealers acting as Commission Agent have to enter turnover of goods for which principal is liable to pay tax against Form VAT 36A. Enter details of such taxable sales in Part III of VAT 8A. 1.8.8 In this part Works Contract d ealers have to enter the turnover on which they are claiming deductions from turnover as per RVAT rule 22A. 1.8.9 In this part dealers have to enter the turnover related to sale of goods to Exporters within the state against Form VAT 15. 1.8.10 Please specify any other turnover which is not liable to Tax under VAT in this column. 1.8.11 In this part dealers have to enter turnover related to sales return of goods within the return period. Please ensure to exclude such sales in Part I of VAT 08 A 1.8 Total : Value will be automatically calculated as sum of 1.8.1 to 1.8.11 B1 Total Turnover :Value will be automatically calculated as 1.1+1.2+1.3+1.4+1.5+1.8 Tab: B2 Purchase Tax / Other Amounts Purchase Tax/Any other payable amount Dealers whose liability to pay tax or any amount arises due to any of the following are required to provide details in this p art. The details should be provided in separate row for each commodity. Reasons for liability should be selected from drop down lis t in the “Type of tax” column. Following are the types of liability : Registered dealers, commonly known as developers/ builders at S.N.6 of notification no F12.(59)FD/Tax/ 2014 - 18 dated 14.07.2014 opting to pay lump sum in lieu of tax have to provide details of purchase price of goods which are procured or purchased from dealer other than the registered dealer of the State and an amount equal to the amount of tax that would have been payable had the goods been purchased in the State from a registered dealer. Registered dealers engaged in execution of works contracts , opting for exemption from payment of tax leviable on the transfer of property in goods opting exemption under notification no F12.(59)FD/Tax/2014 - 23 dated 14.07.2014 have to provide det ails of purchase price of goods which are procured or purchased from dealer other than the registered dealer of the State and an amount equal to the amount of tax that would have been payable had the goods been purchased in the State from a registered deal er. Registered dealers opting for payment of tax in lump sum in accordance with the provisions of section 5 have to provide details of purchase price of goods in stock which has not suffered tax at full rate and tax payable under Rule 17A(7) on such stock at the rate applicable at the time of exercising the option. Registered dealers opting for payment of tax under section 3(2) have to provide details of purchase price of goods in stock which has not suffered tax at full rate and tax payable under Rule 18(7A) on such stock at the rate applicable at the time of exercising the option. Sub - contractors where main contractor has exercised option of exemption fee have to provide details of purchase price o f goods which are procured or purchased from dealer other than the registered dealer of the State and an amount equal to the amount of tax that would have been payable had the goods been purchased in the State from a registered dealer as per proviso of R VAT rule 22A (6). Dealers applying for cancellation of registration have to provide details of tax payable under Rule 43 in respect of every taxable goods held in stock and capital goods on the date of such cancellation. Any other amount for any other reason Tab: B3 Reverse Tax Reverse Tax Dealers must enter details of input tax for which credit has been availed in contravention of the provisions of section 18.Se lect reason for reversal of input tax from the drop down list as : Return of goods sold in period prior to return period Goods purchased for a purpose specified in Section18 (1) (a) to (g) but disposed off otherwise including non - allowable proportionate ITC In case of SOS (up to 4%) ------ % Stocks remained in case of switch over to option u/s3(2) [See Rule17(3)] Stocks remained in case of switch over to option of EC as per notification no F12.(59)FD/Tax/2014 - 23 dated 14.07.2014 Stocks remained in case of switch over to option for payment of tax in lump sum in accordance with t he provisions of section 5 [See Rule17A(6)] Tab: B4 Input Tax B4:1.1 Input Tax & Details of Purchases Dealers claiming ITC against VAT Invoice subject to Section 18 and Rule 18 of RVAT must enter details of purchases and input tax claimed on such purchases. B4:1.2 Purchases of Capital Goods Purchases of capital goods must be entered in this part. B4:1.3 It will be automatically calculated as the sum of 1.1 and 1.2 of B4. 1.4 ITC claimed in 7A ITC claimed as per VAT 7A must be entered here. The amount of tax shown in Part I of VAT - 07A must be equal to the tax shown in 1.4 ITC Claimed in 7A of Input Tax tab of VAT10. B4:1.5Purchases returned In this part dealers have to enter the details of purchases and tax paid on goods which were returned in the return period. B4:1.6 Eligible ITC Value of Eligible Input Tax Credit is automatically calculated as Minimum of (1.3 - 1.5 or 1.4) B4:1.7 ITC carry forward Enter amount of ITC to be carried forward from the previous quarter. B4:1.8 Available ITC Value of available ITC is automatically calculated as 1.6 + 1.7. Tab: C Turnover and Liability under CST Act C 1.1 Tax Liability under CST This part is to be filled only by dealers who have made sales under CST Act. 1.1.1 Dealers must enter details of taxable sales under CST Act. Under “details of sales” select type of sales made e.g. Inter st ate sale against form C, Interstate sale without form, C Branch Transfer etc. 1.1.9 Tota l is automatically calculated as sum of data entered in rows of 1.1.1 1.1.10 In this part dealers have to enter turnover and tax of sales return of goods of period other than the return period under CST Act 1.1 Total is automatically calculated as 1.1.9 - 1.1.10 C 1.2 Turnover not liable to tax under CST Dealers have to provide details of turnover which is not liable to tax under CST 1.2.1 In this part dealers have to enter the turnover of goods which is sold in course of Export against Form H . 1.2.2 In this part dealers have to enter the turnover of goods which is sold in course of Export under section 5(1) . 1.2.3 In this part dealers have to enter the turnover of goods which is sold outside state by Branch/Depot/Stock transf er/consignments against Form F . 1.2.4 In this part dealers have to enter the turnover of subsequent interstate sales of goods u/s 6(2) of CST Act against form C and EI/EII . 1.2.5 In this part dealers have to enter the turnover of interstate sales of goods to any official, personnel, consular, or diplomatic agent of - (i) any Foreign diplomatic mission or consulate in India or (ii) the United Nations or any other similar international bo dy in course of Export against Form J under section 6(3) of CST Act . 1.2.6 In this part dealers have to enter the turnover of interstate sales of goods to SEZ against Form I under section 8(6 ) of CST Act. 1.2.7 In this part dealers have to enter the turnover of interstate sales of goods exempted under CST Act . 1.2.8 Please specify any other turnover which is not liable to Tax under CST in this column. 1.2 Total - Value will be automatically calculated as sum of 1.2.1 to 1.2.8. 1.3 In this part dealers have to enter the turnover of sales return of goods within the return period . C Total Turnover - Value will be automatically calculated as the sum of 1.2,1.3 and 1.3. Tab: D Details of Tax due and Deposit of Tax, Interest and Late Fee D1.1 Details of Tax due In this part dealers have to enter details of tax payable in relevant tax payment period 1. Select Payment Category as per tax period notified under sub - section (1) of section 20 Thrice in a month/ monthly/Quarterly 2. Enter Tax Period in dd - mon - yyyy format according to Payment category selected under payment category. 3. Select Tax Type VAT /CST – Act under which tax is deposited. 4. Enter details of tax payable . 5. Total of tax due must be equal to (upto two decimal) EC Fees + Composition Amount + Tax Under 3(2) + Output Tax + Purchase Tax + Reverse Tax +Tax under CST – ITC – Tax deferred (if any) D1.2 Details of Deposit In this part dealers have to enter details of deposits in the chronological order as per date of deposit. 1. Tax Period – Value will be calculated automatically as entered in D1.1 2. Due date - Value will be calculated automatically according to tax period selected in D1.1 3. Tax Type - Value will be calculated automatically according to tax type VAT/CST selected in D1.1 4. Tax deposited - Enter details of tax deposited. Click on clear to delete all the rows of details of deposit. 5. Date of deposit - Enter date of depo sit in dd - mon - yyyy format. 6. Delay in deposit - Value will be calculated automatically according to delay in payment of due tax. 7. Interest due - Value will be calculated automatically as per prescribed interest rate. 8. Mode of deposit – Select mode of deposit as given in drop down list from amongst EGRAS - manual or electronic,/VAT 37B/ VAT 38/VAT 41/VAT 25 9. Description for Payment - Enter GRN in case of manual payment and CIN in case of electronic payment. D1.3 Details of VAT41/TDS Certificate In this part Registered dealers engaged in execution of works contract have to enter details of VAT 41 received from awarder Tab: Late Fee Details of Late Fee 1. Due date of filing of return - Enter due date of return filing. 2. Date of submission of return - Enter date on which return is to be submitted on web portal. 3. Late fees will be automatically calculated in “Total Late Fees Due“ Column of late fees 4. Amount of late fee - Enter details of Late Fee payable as per Rule 19A 5. Date of deposit of late fee - Enter date of deposi t of late fee. 6. Mode of deposit – Select mode of deposit as given in drop down list from amongst EGRAS - manual or electronic,/VAT 37B/ VAT 38/VAT 41/VAT 25/adjusted against tax creditable ( Enter value adjusted against tax creditable in E 1.30 of Tax Payable Tab if this mode is selected) Tab: E Tax Payable Details of tax payable/ITC carried forward /Refund claimed All the columns except non - white are non - editable and Value will be automatically calculated Total Tax Payable / Deferred 1.1 Output Tax : Value will be calculated automatically as equal to B1.1.7(d) 1.2 Tax Collected as per sales invoice :Enter details of tax collected as per sales invoice for VAT sales 1.3 Output tax : Value will be calculated automatically as maximum of 1.1 and 1.2 1.4 Purchase Tax/ Tax as per rule 22A/43/18(7A)/17A (B2): Value will be calculated automatically as equal to B2 1.5 Reverse Tax : Value will be calculated automatically as equal to B3 1.6 Others, If any, (Specify): Please enter details of any other tax liability, if any Other Description : mention any other tax liability 1.7 Total tax : Value will be calculated automatically as sum of 1.3 to 1.6 1.8 Total input tax credit available : Va lue will be calculated automatically as equal to B4.1.8 1.19 Net Tax Payable : Value will be calculated automatically as (1.7 – 1.8) 1.10 Tax Deferred in Percent (under VAT): Please enter percentage of tax deferred , if any 1.11 Tax Deferred (under VAT): Please enter Value of tax deferred as mentioned in percentage above 1.12 Amount Payable (+)/Creditable : Value will be calculated automatically as (1.9 - 1.11) 1.13 Exemption Fee (in case of works contract): Value will be calculated automatically as equal to B 1.1d 1.14 Composition Fee : Value will be calculated automatically as B1.1.2 d 1.15 Tax Payable on Turnover under section 3(2) [in case opt out of section 3(2)]: Value will be calculated automatically as equal to B1.1.3 d 1.16 Total Amount Payable(+)/Creditable( - ): Value will be calculated automatically as (1.12+ 1.13+1.14+1.15) 1.17 Amount Deposited Under VAT : Value will be calculated automatically as D2 1.18 Amount Payable (+)/Creditable ( - ): Value will be calculated automatically as (1.16 - 1.17) 1.19 Tax due under CST ACT : Value will be calculated automatically as (C - 1.1) 1.20 Tax Collected as per sales invoice: Enter details of tax collected as per sales invoice for CST sales 1.21 Maximum of 1.19 and 1.20 : Value will be calculated automatically as Maximum of 1.19 and 1.20 1.22 Tax Deferred in percent (Under CST): Please enter percentage of tax deferred , if any 1.23 Tax Deferred (Under CST): Please enter Value of tax deferred as mentioned in percentage above 1.24 Set off of Entry Tax paid (Only in case of CST for commodity like paper, Dyes and dyes stuff, Textile auxiliaries, Edible oil notified under section 8 (5) of CST ACT):Enter details of set off 1.25 CST to be deposited: Value will be calculated automatically as mentioned in D1.2 1.26 Creditable ITC to be adjusted Value will be calculated automatically as 1.18 (if in minus) 1.27 CST payable : Value will be calculated automatically as(1.25 - (absolute Value of 1.18 if in minus) 1.28 Amount Deposited Under CST : Value will be calculated automatically as 1.21 - (1.23+1.24) 1.29 Net Tax payable / creditable under VAT +CST : Value will be calculat ed automatically as 1.27 - 1.28 If 1.29 is in negative i.e Tax is creditable, then it is mandatory to adjust the excess amount in 1.30 or 1.31 or 1.32. 1.30 Adjusted against Late Fee (if any): : Value will be auto calculated if entered in Late Fee Tab 1.31 Refund claimed (if any): Enter amount if wish to take refund of excess ITC or excess deposit 1.32 ITC to be carried forward for next quarter: Enter amount if ITC is to be carried forward to next quarter Instructions to fill VAT - 7A The following instructions may please be noted before filling the return Box/Column Instructions to fill up Return Tab: 1. General Info Registration No.(TIN) 1. Registration Number (TIN) is to be entered in this field by all dealers liable to file return in Form VAT - 7A. 2. It should be exactly as per the Registration Certificate issued to the dealer. 3. If TIN is wrong system will not accept the return. 4. This check is introduced to verify TIN of the dealer so that Form VAT - 7A of the dealer other than who has logged on website is not filed. Return Period from Date Every dealer must enter period from to which return belongs in dd - mon - yyyy format e.g. 01 - APR - 2014 Return Period to Date Every dealer must enter period to to which return belongs in dd - mon - yyyy format e.g. 30 - Jun - 2014 Tab: [Part - I] Particulars of purchases, excluding Purchase return with in the return period , made within the State against VAT invoice includ ing Capital Goods on which Input Tax Credit is allowed under section 18(1)) will be filled in Pat I. Tab: [Part - II] Particulars of purchases made within the State against VAT invoice on which Input Tax Credit is not allowed under section 18(1) will be filled in Pat II. Tab: [Part - III] Particulars of purchases made from outside the State other than Capital Goods . Goods Received from outside State (Branch/Depot/Stock Transfer/ Consignment) will be filled in Pat III. Check with VAT10 The amount of tax shown in Part I of VAT - 07A must be equal to the tax shown in 1.4 ITC Claimed in 7A of Input Tax tab of VAT10. Instructions to fill VAT - 8A The following instructions may please be noted before filling the return Box/Column Instructions to fill up Return Tab: 1. General Info Registration No.(TIN) 1. Registration Number (TIN) is to be entered in this field by all dealers liable to file return in Form VAT - 8 A. 2. It should be exactly as per the Registration Certificate issued to the dealer. 3. If TIN is wrong system will not accept the return. 4. This check is introduced to verify TIN of the dealer so that Form VAT - 8A of the dealer other than who has logged on website is not filed. Return Period from Date Every dealer must enter return period fro m to which return belongs in dd - mon - yyyy format e.g. 01 - APR - 2014 Return Period to Date Every dealer must enter return period to which return belongs in dd - mon - yyyy format e.g. 30 - Jun - 2014 Tab: [Part - I] Particulars of sales made within the State against VAT invoice to registered dealers excluding MRP sales and excluding sales return within the return period will be filled in Pat I Tab: [Part - II] Particulars of sales made within the State against VAT invoice other than in Part - I and ( ii ) against invoices will be filled in Pat II Tab: [Part - III] Particulars of goods sold in the state on behalf of principal against form VAT 36A will be filled in Pat III Check with VAT10 The amount of tax shown in Part I and Part II of VAT - 08A must be equal to the Maximum of [(sum of 1.4 Total and 1.5 Total of Tax Liability 2 tab ) , (1.2 Tax Collected as per sales invoice of Tax Payable tab)]