Direct Costs Unallowed Costs Rate Fixed with CarryForward Indirect Rate Calculation Indirect Cost Classification Matrix Classifications Direct Excluded Indirect or Unallowed ID: 1027256

Download Presentation The PPT/PDF document "Indirect Costs + Carry-Forward" is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

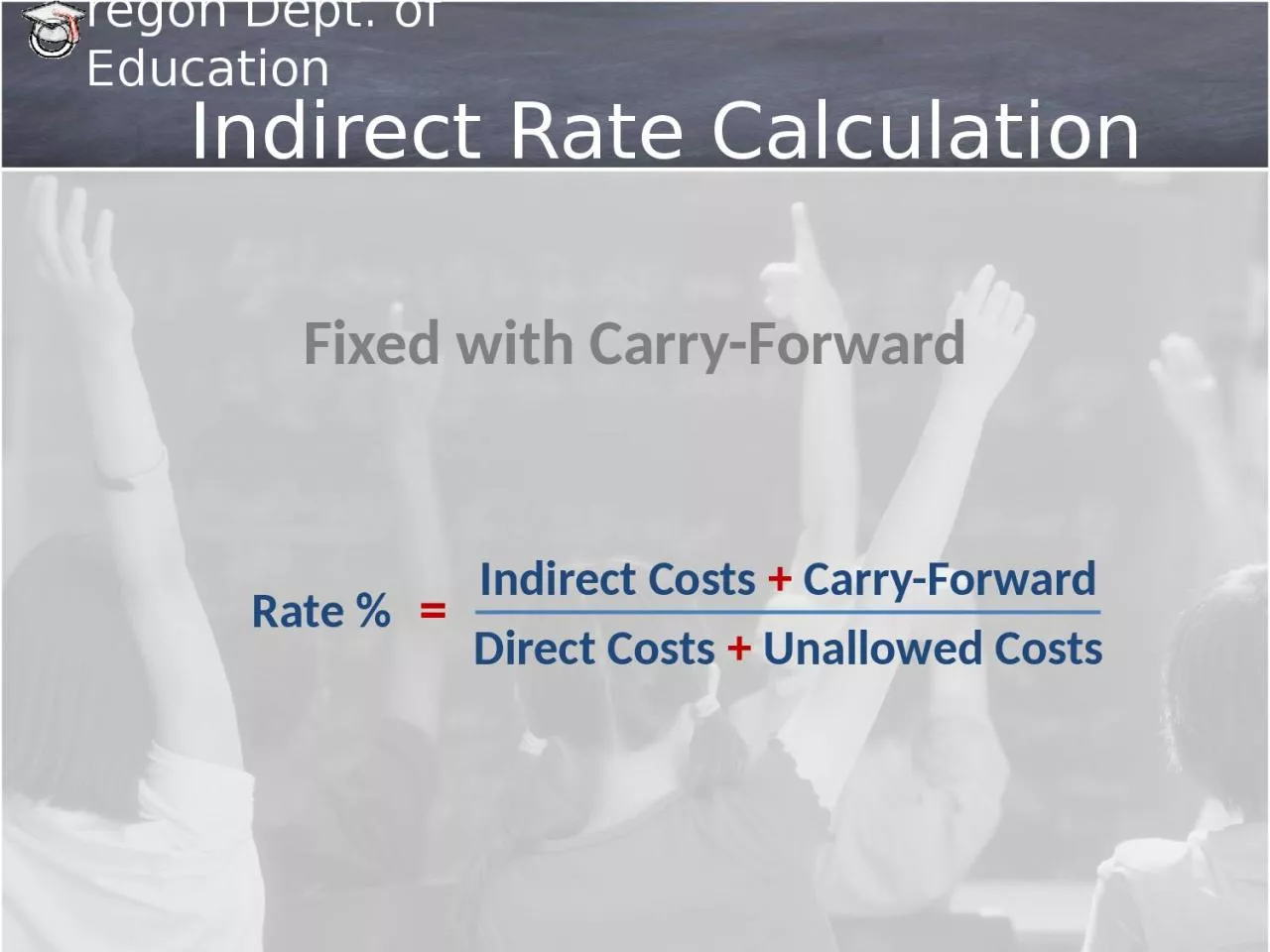

1. Indirect Costs + Carry-ForwardDirect Costs + Unallowed Costs=Rate % Fixed with Carry-ForwardIndirect Rate Calculation

2. Indirect Cost Classification MatrixClassifications: Direct, Excluded, Indirect, or UnallowedFund, function, and object determines the classificationOMB Circular A-87 (additional guidance)PBAM 2010 (additional guidance)Cost Classification

3. Can be identified specifically with a particular cost objectiveExamples of direct costs incurred specifically to carry out a specific programEmployee payrollTravel expensesMaterials/suppliesOffice ExpensesDirect Costs

4. Common or joint purpose benefiting more than one cost objectiveA few examples of indirect costsProcurementPayrollPersonnel functionsMaintenance/operations of spaceData processingAccountingAuditingBudgetingTelephonePostageIndirect Costs

5. CANNOT be charged to federal awards & included only for purposes of calculating the indirect rate.A few examples of indirect costsBad debtsContingenciesEntertainmentFinesPenaltiesGeneral governanceContributions/donations to outside organizationsUnallowed Costs

6. Not included in the calculationA few examples of indirect costsCapital outlayNon-capitalized equipmentDebt serviceJudgments (against school districts)Internal service fund expendituresIndirect cost recoveriesFire prevention & safety fundsExcluded

7. Based on an estimate of that period’s level of operationEstimates using actual expendituresDifference between estimated and actual is carried forward as an adjustmentAdjustment carried forward to 2nd FY Odd years compared with odd years; even with evenCarry-forward adjustment is either an under or (over) recoveryCarry-Forward Calculation

8. 2 Types of Adjustments: Mandatory & Optional*MandatoryGeneral managementContract expenditures > $25,000 (per contract per FY)OptionalTerminal leaveFood servicesInsuranceJudgments*See Indirect Cost Plan for a complete list of mandatory & optional adjustmentsAdjustments

9. Non Sub Award Adjustments

10. General Management Adjustment