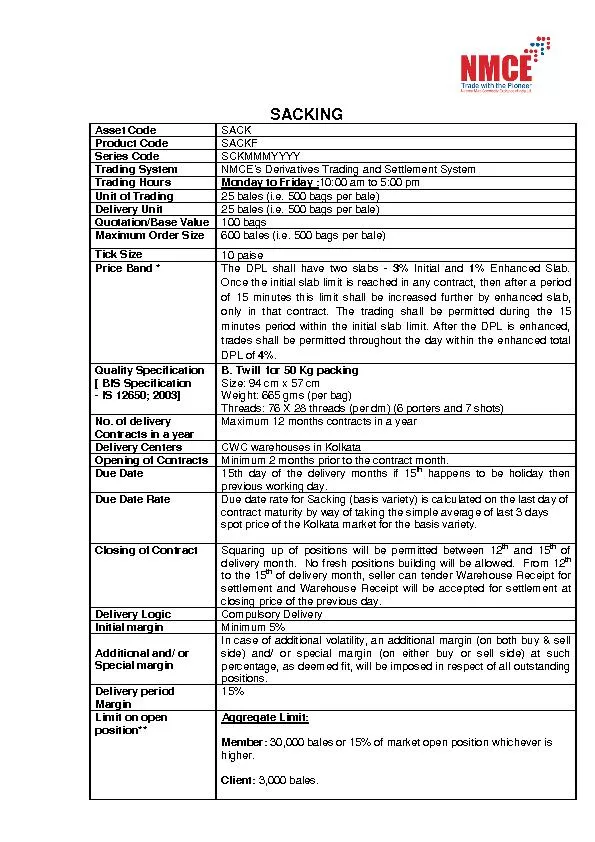

The EMIR Reporting Technical Standards Victoria Cooley OTC Derivatives amp Post Trade Policy Financial Conduct Authority 1 2 Agenda Introduction to EMIR The reporting requirements ID: 707369

Download Presentation The PPT/PDF document "New EU Rules on Derivatives Trading" is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Slide1

New EU Rules on Derivatives TradingThe EMIR Reporting Technical Standards

Victoria CooleyOTC Derivatives & Post Trade PolicyFinancial Conduct Authority

1Slide2

2AgendaIntroduction to EMIR

The reporting requirementsFrequently asked questionsReporting to trade repositoriesSlide3

3IntroductionG20 statement in Pittsburgh:

All standardised OTC derivative contracts should be traded on exchanges or electronic trading platforms, where appropriate, and cleared through central counterparties by end-2012 at the latest. OTC derivative contracts should be reported to trade repositories. Non-centrally cleared contracts should be subject to higher capital requirements. Slide4

4The reporting requirementsSlide5

5Reporting obligation

Applies to all counterparties to all derivative contracts (OTC and exchange traded)Information to be reported to TRs - about 60 data fields in total!

Basic trade information, ‘who, what, when, how many and how much’;

- the parties to the contract (or the beneficiary)

- type of contract

- maturity

- notional value

- price

- settlement date

- unique trade identification

- amendments to tradeSlide6

6Reporting of exposures

Essential for monitoring systemic riskOnly financial and non-financial counterparties (NFC) above the clearing threshold are required to report exposuresInformation to be reported daily; - Mark to market or model valuations

- Collateral value and basis (transaction or portfolio)

6 month transitional from reporting start dates for reporting exposures informationSlide7

7Timeline for reporting

Credit and interest rate derivatives; - If no registered TRs by 1 April – 90 days after registration - Expected mid-September 2013For all other derivatives;

- If TR is registered by 1 October - reporting

begins 1 January 2014

- If no registered TRs by 1 October – 90 days

after registrationSlide8

8Timeline for reporting

Backloading of existing tradesIf outstanding at time of reporting date; - 90 days to report to TR - report in current position

If not outstanding, but remained outstanding on 16 August 2012;

-

3 years to report to TR

- report final positionSlide9

Frequently asked questions9Slide10

10Frequently asked questionsThere is a need to ensure harmonisation of reporting across EU

ESMA published 1st set of Q&As in March 2013Expected to be an iterative process

Need for immediate Q&As for trading scenarios, give up trades, block/allocation tradesSlide11

Frequently asked questionsStill some uncertainty around interpretation

Work is ongoing to establish how EMIR applies in some situationsRest of the presentation represents current FCA views and may be subject to further clarification by either the European Commission or ESMA

11Slide12

12Clearing models

If the process involves creation of a bilateral trade followed by novation, separate reports likely to be requiredIf clearing is instantaneous and no bilateral trade exists, only the cleared trade should need to be reportedCorrect approach where novation occurs very quickly after bilateral execution still subject to discussionSlide13

Who has reporting obligationBrokers and dealers do not have a reporting obligation when they act purely in an agency capacity

Still some uncertainty over how to report transactions where a broker, dealer or clearing member clears or facilitates a transaction for a client on a principle basis13Slide14

14Give up trades

Only counterparties to the contract have reporting obligationTypically, counterparty and CCP would reportApproach still to be agreed at EU levelSlide15

15Reporting of block/allocation trades

No exemptions – reporting obligation applies to all derivative transactionsIf block trade gives rise to multiple transactions, each of those would have to be reportedProcess still to be agreed at EU level however we expect both stages to be reportedSlide16

16Reporting to trade repositoriesSlide17

17How to fulfil reporting obligation

Both counterparties MUST report each trade unless by prior arrangement, one party can report on behalf of both counterparties Either counterparty may also delegate reporting to a third-party (such as a CCP or trading platform)Likely through contractual obligations with one another which should set out what information is to be reported

Regulatory responsibility remains

with original counterpartiesSlide18

Practical preparationsFirms either have to establish delegated reporting arrangements or direct connectivity with a TR

If delegating; - make sure delegate is willing to accept the delegation (including for any intragroup trades) - have processes in place to ensure that reports submitted on your behalf are accurateIf want to connect directly to a TR;

- start now

- consider whether TR(s) will be authorised in time

- will TR cover all asset classes for all reporting

obligations

18Slide19

Legal entity identifiers (LEI) - ROC established January - Expect Central Operating Unit to be formed

in April/May - Interim phase – Local Operating Units - Expect pre-LEIs code to be mutually recognised

19

IdentifiersSlide20

20IdentifiersUnique product identifiers

- No agreed EU UPI - Existing codes, ESMA taxonomyUnique trade identifiers - No agreed EU UTI - Counterparty generates and agrees with other counterparty

- Lifecycle events include UTI linked to

original UTISlide21

21Further information – visit our website

www.fca.org.uk/firms/markets/international-markets/emirLinks to Commission and ESMA publicationsLink to ESMA Q&ALink to FCA consultationsEMIR mailing listSlide22

22

Any questions?