Agriculture and Policy Outlook Conference Ben Brown November 2 2018 The Early Years A photographic 12 months 2018 A Tale of Two Halves Source USDAAgricultural Marketing Service Daily Prices for Cincinnati Ohio ID: 727397

Download Presentation The PPT/PDF document "Commodity Outlook: Corn and Soybeans St..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Slide1

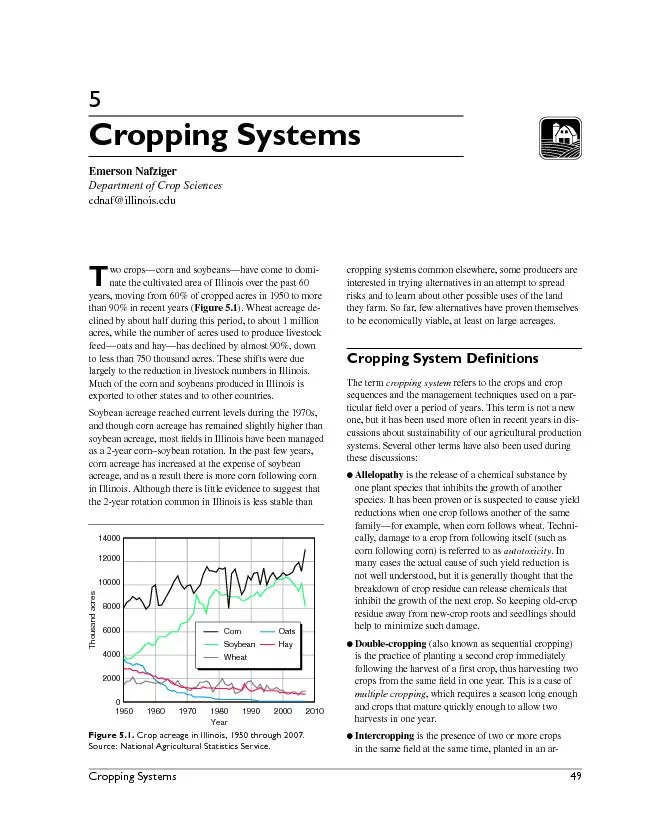

Commodity Outlook: Corn and Soybeans Struggle to Find Strength

Agriculture and Policy Outlook Conference

Ben Brown

November 2, 2018Slide2

The Early Years-

A photographic 12 monthsSlide3

2018: A Tale of Two Halves

Source: USDA-Agricultural Marketing Service Daily Prices for Cincinnati, Ohio

January-May

$4.00 corn and $10.50 soybean cash prices

Strong world economic growth

Shrinking world stocks

June-October

Escalating trade tensions

Large SuppliesSlide4

Location, Location, Location

South America Drought: Spring 2018

Source: Latin American Flood

and Drought Monitor at Princeton

Drought in South America Reduced World Ending Stocks even with large U.S. corn stocks

Corn: -

2

%

Soybeans: -1%

Absolute changes in Brazil helped counter losses in Argentina

Source: USDA-FASSlide5

U.S. Corn Yield: Another Record

Source: USDA- NASS

New Record 3 Straight Years

6 Straight years of Above Trend Yields

2013 was at the time

Reasons?

Weather

Genetics

ManagementSlide6

Ohio Corn Yield: How’d we compare?

Record Yields Across Corn Belt

Ohio 13 bu./acre above previous record (2017)

Ohio outperformed the country in deviation from trend

The country had a good year, we just had a better one!

2018 Corn Yield by State

Bushels per Acre

Source: USDA- NASS

October Crop ProductionSlide7

U.S. Corn Production: Up from 2017

U.S. Production is up from 2017 on higher yields.

Not a record due to fewer acres.

Only 3 major corn producing states up in acreage from 2017.

Missouri, Nebraska and Ohio

Second Largest Ohio corn

c

rop.Slide8

U.S. Corn Demand: Continues Strong

2015/16

2016/17

2017/18

2018/19

Δ 2017/18

Area Planted

(Mil. Acres)

88.0

94.0

90.2

89.1

-1%

Yield

(Bu./acre)

168.4

174.6

176.6

180.7

2%

Production

(Mil. Bu.)

13,602

15,148

14,604

14,778

1%

Beg

. Stocks

(Mil. Bu.)

1,731 1,737 2,293 2,140 -7%Imports(Mil. Bu.) 67 57 36 50 39%Total Supply(Mil. Bu.) 15,401 16,942 16,934 16,968 0%Feed & Residual(Mil. Bu.) 5,120 5,470 5,302 5,550 5%Food, Seed, & Other(Mil. Bu.) 1,422 1,453 1,453 1,480 1%Ethanol(Mil. Bu.) 5,224 5,432 5,601 5,650 1%Exports(Mil. Bu.) 1,898 2,294 2,438 2,475 2%Total Use(Mil. Bu.) 13,664 14,649 14,793 15,155 2%Ending Stocks(Mil. Bu.) 1,737 2,293 2,140 1,813 -15%Season Av Price($/bu.)$3.61$3.36$3.36$3.50+ $0.14

Higher Production and Lower Beg. Stocks Roughly same Total Supply as 2017/18

Source: USDA-WAOBSlide9

2015/16

2016/17

2017/18

2018/19

Δ 2017/18

Area Planted

(Mil. Acres)

88.0

94.0

90.2

89.1

-1%

Yield

(Bu./acre)

168.4

174.6

176.6

180.7

2%

Production

(Mil. Bu.)

13,602

5,148

14,604

14,778

1%

Beg

. Stocks

(Mil. Bu.)

1,731 1,737 2,293 2,140 -7%Imports(Mil. Bu.) 67 57 36 50 39%Total Supply(Mil. Bu.) 15,401 16,942 16,934 16,968 0%Feed & Residual(Mil. Bu.) 5,120 5,470 5,302 5,550 5%Food, Seed, & Other(Mil. Bu.) 1,422 1,453 1,453 1,480 2%Ethanol(Mil. Bu.) 5,224 5,432 5,601 5,650 1%Exports(Mil. Bu.) 1,898 2,294 2,438 2,475 2%Total Use(Mil. Bu.) 13,664 14,649 14,793 15,155 2%Ending Stocks(Mil. Bu.) 1,737 2,293 2,140 1,813 -15%Season Av Price($/bu.)$3.61$3.36$3.36$3.50+ $0.14

Cattle on Feed is up 5% from 2017, new recordSeptember placements were lower than 2017Source: USDA-WAOB

Corn Feed Use:

Livestock up but use down??Slide10

Corn Feed Use: Disappointing 4th Quarter

Data: USDA-ERS, Feed-Grain Report

Needed to reach USDA 5,550

First Quarter feed usage makes up roughly 43% of total MY feed use.

To reach 5,550 the first quarter would need 2,385 mil. bu.

Given low performance of 2017/18 forth quarter, first quarter could look more like 2,200 mil. bu.

2017/18 feed use decline 250 mil. bu. from Oct- Finish

5,150- (350)Slide11

U.S. Corn Demand: Ethanol Strong in 2017/18

2015/16

2016/17

2017/18

2018/19

Δ 2017/18

Area Planted

(Mil. Acres)

88.0

94.0

90.2

89.1

-1%

Yield

(Bu./acre)

168.4

174.6

176.6

180.7

2%

Production

(Mil. Bu.)

13,602

5,148

14,604

14,778

1%

Beg

. Stocks

(Mil. Bu.)

1,731 1,737 2,293 2,140 -7%Imports(Mil. Bu.) 67 57 36 50 39%Total Supply(Mil. Bu.) 15,401 16,942 16,934 16,968 0%Feed & Residual(Mil. Bu.) 5,120 5,470 5,302 5,550 5%Food, Seed, & Other(Mil. Bu.) 1,422 1,453 1,453 1,480 1%Ethanol(Mil. Bu.) 5,224 5,432 5,601 5,650 1%Exports(Mil. Bu.) 1,898 2,294 2,438 2,475 2%Total Use(Mil. Bu.) 13,664 14,649 14,793 15,155 2%Ending Stocks(Mil. Bu.) 1,737 2,293 2,140 1,813 -15%Season Av Price($/bu.)$3.61$3.36$3.36$3.50+ $0.14

Higher Production and Lower Beg. Stocks Roughly same Total Supply as 2017/18

Source: USDA-WAOBSlide12

U.S. Corn Use:

Expanded E-15, Little Change

Ethanol

Production

2015

2016

2017

2018

2019

Mill.

Barrels per Day

0.966

1.003

1.04

1.048

1.033

Percent Growth

4%

4%

1%

-1%

Data Source: U.S. Energy Information Administration Short Term Energy Outlook

Oct 9, Trump proposes E-15 Reid Vapor Pressure waivers. EPA needs to offer rule and then lawsuits likely.

RIN’s are cheap not making up for lower mpg

The RFS is the rule of the land and so is the Clean Air Act. Any change to RVP waivers will likely require changes to policy.

Oil and Gasoline Prices are forecasted slightly up in 2019 with little to no increases in consumption.

Low Profit Margins by Ethanol Manufactures expected at breakeven for 4

th

year. Lower daily production.Slide13

U.S. Corn Use: Ethanol Exports

Ethanol Exports were record strong in 2017/18 at almost 1.62 billion gallons.

U.S. Ethanol Exports to Brazil accounted for 34% of total 2017/18 exports.

Brazil’s Ethanol stocks are up 29% over last year.

Sugar refineries

2018/2019 corn use for ethanol numbers are more likely to be similar to 2017/18 at 5.6

bil

. Bu., than current projections of 5.65

bil

.

B

u.

Top U.S Ethanol Markets

Brazil

33%

Canada

24%

India

13%

Philippines

5%

Data Source: U.S.-EIASlide14

U.S. Corn Demand: Exports Finish Strong

2015/16

2016/17

2017/18

2018/19

Δ 2017/18

Area Planted

(Mil. Acres)

88.0

94.0

90.2

89.1

-1%

Yield

(Bu./acre)

168.4

174.6

176.6

180.7

2%

Production

(Mil. Bu.)

13,602

15,148

14,604

14,778

1%

Beg

. Stocks

(Mil. Bu.)

1,731 1,737 2,293 2,140 -7%Imports(Mil. Bu.) 67 57 36 50 39%Total Supply(Mil. Bu.) 15,401 16,942 16,934 16,968 0%Feed & Residual(Mil. Bu.) 5,120 5,470 5,302 5,550 5%Food, Seed, & Other(Mil. Bu.) 1,422 1,453 1,453 1,480 1%Ethanol(Mil. Bu.) 5,224 5,432 5,601 5,650 1%Exports(Mil. Bu.) 1,898 2,294 2,438 2,475 2%Total Use(Mil. Bu.) 13,664 14,649 14,793 15,155 2%Ending Stocks(Mil. Bu.) 1,737 2,293 2,140 1,813 -15%Season Av Price($/bu.)$3.61$3.36$3.36$3.50+ $0.14

Higher Production and Lower Beg. Stocks Roughly same Total Supply as 2017/18

Source: USDA-WAOBSlide15

U.S. Corn Use: Low Price Spurs Exports

S

trong corn sales through the first 8 weeks of the marketing year.

2018/19 corn sales came in 30% higher last week than a year ago.

Export inspections through the first 8 weeks sit 70% above a year ago.

Large supply and relatively low prices suggest strength in exports.

Statu

s of

Emerging

and Existing Markets

Country

Percent Change

Absolute Change Million Bushels

Vietnam

632%

63

Mexico

11%

56

EU-27

114%

40

Israel

847%

23

Columbia

12%

21

Japan

-

6%

-29

Data: USDA-FAS

755,000Slide16

U.S. Corn: Balance Sheet

Oct

WASDE

Ag

Policy and Outlook Forecast

Difference

Supply

Harvested Acres (Millions)

81.8

81.8

-

Yield (Bushels/ Acre)

180.7

180.7

-

Total Production (Million Bushels)

14,778

14,778

-

Beginning Stocks (Million Bushels)

2,140

2,140

-

Imports (Million Bushels)

50

50

-

Total Supply

16,968

16,968

-

Demand

Feed and Residual (Million bushels)

5,550

5,250(300)Food, Seed and Industry (Million bushels)7,1307,090(40) Ethanol5,6505,610(40)Exports (Million Bushels)2,4752,500+ 25Total Demand15,15514,840(315)Ending Stocks1,8132,128 180Ending Stocks as a Percentage of Use

11%

12%

1%

Average

MY Price 2018/19 ($/

Bushel)

$

3.50

$

3.50

No

ChangeSlide17

Corn Basis:

Weak

Dec Futures

Mar Futures

May Futures

Sept Futures

Basis is local, but weak across the state

To start 2018/19 marketing year Ohio is on average $0.20 below 5-year average

Lowest at harvest, then increasing

My expectation is for corn to follow this pattern increasing $0.10 by May unless tariffs are lifted.

Data Source: Author Calculation using DTN dataSlide18

Corn Marketing: Return to Storage Positive

Source: Author Calculations using CME Futures Prices

1-Nov

1-Aug

Change

Futures

$3.64

$3.99

$0.35

Basis

-$0.44

-$0.25

$0.19

Cash

$3.20

$3.74

$0.54

On farm storage shows positive returns.

Does not include bin cost.

U

nusual to see positive commercial storage returns.

Chance for

speculative returns

from storing.

If there is a chance that prices could go up there is also a chance they go down.

Cautions

to this: Basis may not increase $0.19 and storage charges might be more than $0.046. Slide19

2018/19 World Corn Production: Up

Million Metric Tons

2017/18

2018/19

Percent Change

World

1,034.20

1,068.3

3.3%

United States

371

375.4

1.2%

Foreign

663.3

692.9

4.5%

Argentina

32

41

28.1%

Brazil

82

94.5

15.2%

South Africa

13.5

13

-3.7%

Egypt

6.4

6.8

6.2%

European

Union

62.3

61

-2.1%

Mexico

27.526-5.5% Canada14.114.52.8% China215.92254.2% Ukraine24.13128.6%Data Source: USDA- WAOBSlide20

Stocks to Use: Tighter World and U.S. Stocks

Even with increasing production world use of corn has increased, lowering both U.S. and World Stocks to Use Ratios.

2018 projected at 11%

Tight stocks to use would suggest that any sudden positive change in world supply or use would sharply increase price.

Source: USDA-FAS & WAOBSlide21

U.S. Soy Yield: 4 out of 5 Years of New Records

4 out of last 5 years have been new records.

Ohio -60 bu./acre

Oct. WASDE + 0.3 from Sep. Estimate.

Ohio’s performance in yield was strongest in last 33 years.

Source: USDA-NASSSlide22

U.S. Soy Production: New Record, Bad Time

Acreage was down 534,000 acres in the Oct. WASDE, cutting total production.

But still record acreage.

Second

time in

history more soybean acres then corn acres.

Projected soybean returns early in the year suggested the market favored soybeans to corn.

Large increases in demand last eight years.

Source: USDA-NASSSlide23

U.S. Soybeans: Story is really all about Exports

2015/16

2016/17

2017/18

2018/19

Δ 2017/18

Area Planted

(Mil. Acres)

82.7

83.4

90.1

89.1

-1%

Yield

(Bu./acre)

48.0

52.0

49.3

53.1

8%

Production

(Mil. Bu.)

3,926

4,296

4,411

4,690

6%

Beg.Stocks

(Mil. Bu.)

191

197 302 438 45%Imports(Mil. Bu.) 24 22 22 25 14%Total Supply(Mil. Bu.) 4,140 4,515 4,734 5,153 9%Crushing(Mil. Bu.) 1,886 1,901 2,055 2,070 1%Exports(Mil. Bu.) 1,942 2,166 2,129 2,060 -3%Seed and Residual(Mil. Bu.) 115 146 112 137 22%Total Use(Mil. Bu.) 3,944 4,214 4,296 4,268 -1%Ending Stocks(Mil. Bu.) 197 302 438 885 102%Season Average Price($/bu.)$8.95$9.47$9.33$8.60-$0.73Source: USDA-WAOBSlide24

Soybean Price: Large S

upplies Counter Exports

Data Source: USDA- NASS

2018/19 originally forecasted as largest year for U.S. Soybean exports at 2,290 mil. bu. (Currently 3

rd

)

Increased U.S. and world production have weighed on price even with expanded exportsSlide25

Total Soy Exports: Lagging in 2018/19

Cheap soybeans encouraged exports in end of 2017/18.

Exports have been extremely week to start 2018/19.

33% behind average pace and forward sales are 16% below last year.

1

st

Quarter historically represents 42% of total sales.

Simply the smaller markets are

NOT

making up the loss from China.

Brazil’s new crop will soon be on the market.

Data Source: USDA-FAS

Statu

s of

Emerging

and Existing Markets

Country

%

Change

Absolute Change

Metric Ton

EU

-27

210%

1,094,487

Egypt

1,968%

411,176

Iran

733%

294,417

Netherlands

106%

203,681Slide26

How dependent is the U.S.?: Soybeans

Data Source: Author calculation using USDA-FAS dataSlide27

How Dependent is the U.S.?: Soybeans

Data: USDA- FSA; Calculated by Author

The U.S. soybean market has become more demand concentrated than corn and pork.

Did market concentration expose the U.S. soybean industry?

We can assume that the trade war will diversify U.S. soybean exports.

Some will argue for government regulation to prevent disruption again in the future. Slide28

U.S. Soybeans: Exports to China Not There

Data Source: USDA-FAS

Chinese Sales are currently 320 million bushels from a year ago.

The China National Grain and Oilseed Center has China soybean imports projected another 300 million bushels below current USDA projections at 3.45 bi. Bu. (10% reduction)Slide29

Soybean Price: Difference in U.S & Brazil

Data Source: USDA-AMS and

Cepea

(BR)

Brazil and U.S. soybean prices have historically tracked each other with occasional difference.

There is a noticeable break starting in June between the two prices.

Brazil Producers are getting the signal to expand production.

U.S Producers will get the signal to contract production. Slide30

-From South China Morning Post

-From CGTN

While the production and import changes from 2017 are small, what is the potential in future years?

Will China continue to change

their production policies?

Away from subsidies for corn and wheat to soybean

production.

Chinese

Soybean Behavior

(Million Metric Tons)

2017/18

2018/19

%

Δ

Production

14.2

15

6%

Imports

96.0

94.0

-2%

Ending Stocks

23.5

20.76

-12%

Data Source: WASDE Oct. Update

China Consumption Behavior:

ChangingSlide31

Source: USDA- Oilseeds: World Markets and Trade

China Oilseeds Supply

Distribution

(Million Metric Tons)

Domestic

Use

2014/15

2015/16

2016/17

2017/18

2018/19 Jun

2018/19

Palm Oil

5.7

4.8

4.8

5.1

4.9

5.4

Peanut Oil

2.8

2.9

3.0

3.1

3.2

3.1 Rapeseed Oil 4.0 4.1 4.1 4.3 4.6 5.1 Soybean Oil 14.2 15.4 16.4 16.9 18.5 17.3 Sunflower Oil 1.0 1.4 1.3 1.4 1.6 1.6 Other 2.1 1.8 1.9 2.1 2.1 2.2 Total 29.8 30.4 31.5 32.8 34.8 34.7 Substitution: Other Protein Sources for ChinaSlide32

U.S. Soybeans: Story is really all about Exports

2015/16

2016/17

2017/18

2018/19

Δ 2017/18

Area Planted

(Mil. Acres)

82.7

83.4

90.1

89.1

-1%

Yield

(Bu./acre)

48.0

52.0

49.3

53.1

8%

Production

(Mil. Bu.)

3,926

4,296

4,411

4,690

6%

Beg.Stocks

(Mil. Bu.)

191

197 302 438 45%Imports(Mil. Bu.) 24 22 22 25 14%Total Supply(Mil. Bu.) 4,140 4,515 4,734 5,153 9%Crushing(Mil. Bu.) 1,886 1,901 2,055 2,070 1%Exports(Mil. Bu.) 1,942 2,166 2,129 2,060 -3%Seed and Residual(Mil. Bu.) 115 146 112 137 22%Total Use(Mil. Bu.) 3,944 4,214 4,296 4,268 -1%Ending Stocks(Mil. Bu.) 197 302 438 885 102%Season Average Price($/bu.)$8.95$9.47$9.33$8.60-$0.73Source: USDA-WAOBSlide33

Soybean Crush: Shifts by Country

1,00

0 Metric Tons

2014/15

2015/16

2016/17

2017/18

2018/19

Jun

2018/19

Oct

China

74,500

81,500

88,000

90,000

102,000

93,500

United States

50,975

51,335

51,742

55,926

54,431

56,336

Argentina

40,235

43,267

43,303

37,500

44,000

43,000

Brazil

40,435

39,747

40,411

43,600

43,200

42,700

European Union14,45014,95014,40015,00014,90016,600India7,7005,5009,0007,6009,1009,000ROW36,51538,72540,49044,51345,84247,065Total264,810275,024287,346294,139313,473308,201International and Domestic Prices in relation to soybean meal and soybean oil influence quantity of soybean crush Source: USDA- Oilseeds: World Markets and TradeSlide34

U.S. Soy: Balance s

heet, looking for positives

Oct

WASDE

Ag

Policy and Outlook Forecast

Difference

Supply

Harvested Acres (Millions)

88.3

88.3

-

Yield (Bushels/ Acre)

53.1

53.1

-

Total Production (Million Bushels)

4,690

4,690

-

Beginning Stocks (Million Bushels)

438

438

-

Imports (Million Bushels)

25

25

-

Total Supply

5,153

5,153

-

Demand

Crushings

(Million Bushels)2,0702,080+ 10Exports (Million Bushels)2,0601,960(100)Seed and Residual (Million Bushels)137150+ 13Total Demand4,2684,190(78)Ending Stocks845963 118Ending Stocks as a Percentage of Use20%23%+ 3%

Average

MY Price 2018/19 ($/

Bushel)

$8.60

$8.30

($0.30)Slide35

Soybean Basis:

Weak

Data Source: Author Calculation using DTN data

Nov Futures

Jan Futures

Mar Futures

Aug Fut.

Basis is local,

large

differences across state

To start 2018/19 marketing year Ohio is on average $

0.36

below

3-year

average

Lowest at harvest, then increasing

I’m not sure we can expect basis to increase as much later in the year given PNW basis conditions.

May Futures

Jul Futures

Sep Fut.Slide36

Soybeans: Return to Storage Positive

On-Farm Storage does not include bin cost.

These estimates use future basis prices. Should we expect basis to strengthen?

Similar to corn, there is an opportunity for

price speculation

.

What if the trade negotiations are resolved?

Source: Author Calculations using CME Futures Prices

1-Nov

1-Aug

Change

Futures

$8.33

$9.00

$0.67

Basis

-$0.75

-$0.50

$0.25

Cash

$7.58

$8.50

$0.92

Cautions

to this: Basis may not increase $0.19 and storage charges might be more than $0.046. Slide37

Soybean Stocks to Use: Double 2017/18

Data Source: USDA-FAS & WAOB

Large supply and reduced exports result in more production and less consumption for 2018/19

Stocks to use forecasted double 2017/18.

Largest since 1985/86

Why does this matter?

Soybean price and stocks-to-use are negatively correlated. Slide38

Soybean Price Potential: Struggling

Source: USDA-FAS & WAOB

Outside a resolution in trade with China or a production shortfall in one of the major producing countries, the current 885 Mil. Bu. might be low.

Recent price rallies appear linked to the market over projecting yield or under projecting failed acreage early on.

Price prospects look to have limited upside potential. Slide39

Cash Flow:

2018 ARC-CO PMTS

2018 Ohio ARC Corn Payments

2018 Ohio ARC Soybean Payments

Corn: 2017 vs 2018

Smaller Payments ($57-$9)

Fewer Counties (87-16)

Soybeans: 2018 vs 2017

Larger Payments ($18-$19)

More Counties (34- 56)Slide40

USDA: Market Facilitation Program

Initial Payment Rate

Effective Payment Rate

Units

U.S. Expected Payment ($1,000)

% MFP Program

Payment $/Acre

U.S.

Ohio

Soybeans

$1.65

$0.825

per bushel

$3,629,700

75%

$43.81

$49.50

Pork

$8.00

$4.00

per head

$290,300

6%

Cotton

$0.06

$0.03

per pound

$276,900

6%

$27.03

Sorghum

$0.86

$0.43

per bushel

$156,800

3%

$32.25

Dairy

$0.12

$0.06 per cwt$127,400 3%Wheat$0.14 $0.07 per bushel$119,200 2%$3.33 $5.25 Corn$0.01 $0.005 per bushel$96,000 2%$0.90 $0.95 Fresh Cherries$0.16 $0.08 per pound$79,400 2%Shelled Almonds$0.03 $0.015 per pound$33,075 1%Total$4,808,775 100%Initial Payment Rate published by USDA, Expected payments and per acre payments are the authors calculation based on the USDA- NASS Oct Crop Production ReportApplications: www.farmers.gov/MFPSlide41

Soy Revenue: Large Crop and Aid Help in 2018

Crop Year

2016

2017

2018

Cash Price ($/bu.)

$9.66

$9.62

$8.40

Yield

(Bu./ Acre)

54.5*

49.5

60**

ARC-CO

PMT ($/Arce)

$36.93

$7.08

$12.53

MFP (2018 Only)

$49.50

Gross

Revenue/ acre

$563

$483

$566

* Current Record

** USDA October Forecast

*** Estimate for Cash Price

Working Capital is forecasted stronger in 2018

Large Yields and government assistance

Smart to save for 2019

Avg. Yields,

f

ew counties expected ARC Pmts., No MFPSlide42

Corn Revenue: Down from 2017

Crop Year

2016

2017

2018

Cash Price ($/bu.)

$3.61**

$3.55**

$3.60***

Yield

(Bu./ Acre)

159

177*

190

ARC-CO

PMT ($/Acre)

$65.01

$55.94

$1.57

MFP (2018 Only) ($/Acre)

$0.95

Gross

Revenue/ acre

$639

$684

$715

* Current Record

** Ohio MYA Price- NASS

***Estimate of Ohio MYA Price

Stronger price, weaker basis

Not all counties trigger ARC Pmt., but $2.50 in gov. assistance

2018 average variable costs plus land charge= $600Slide43

What could change this Analysis?

Production volumes of corn and soybeans in Brazil and Argentina

Resolution to trade disputes with China

U.S. Planting of Corn and Soybean reported in profit summaries of major seed companies and the USDA March Prospective Planting ReportSlide44

Soybean Production: Comparative Advantage?

Assuming same quality of soybean, the total U.S. comparative advantage over Brazil in soybean production is shrinking.

Transportation remains a nontrivial factor for the Mato Grosso State.

Chinese infrastructure investment in Brazil will be impactful to U.S. future competitiveness, all else equal.

Data Collected in Partnership with U.S. Federal Reserve BankSlide45

South America Acreage: UP in 2018/19

Brazil: Five year average in corn/ soybean acreage=

4.5% increase

2017 to 2018=

6.8% increaseArgentina: Slightly up, but projected larger yield compared to drought of 2017/18

Source: USDA-PSD dataSlide46

U.S. Acreage: Reduction in Soy, Increase in Corn

Given Current commodity prices, it is possible to see a reduction in corn and soybean combined acres.

177 million acres- 91 corn and 86 soybeans

Western Corn Belt states (Kansas, Oklahoma, Nebraska) more wheat, sorghum and cotton

Source: USDA-NASSSlide47

Key Takeaways: The 2 minute Rundown

Gr

ain Marketing

Weak Futures &

Weak Basis

Grain Elevator forward cash bids suggest that there could be improvement to basis for both corn and soybean.

Strong premiums for spring and early summer 2019

Today’s

f

uture price show

p

ositive return to storage for both on-farm and commercial storage.

Large supplies and lower use will continue to weigh on soybean prices.

Changing prices will influence producer/consumer choices

Market Facilitation Payments, ARC-CO soybean PMTs & FSA loans can help with cash flow this winter.

Not expecting the same cash flows in 2019. Slide48

Until we meet agrain… (or oilseeds)

Picture of soybean pile in North Dakota-October 20thSlide49

Ben BrownProgram Manager: Ohio Farm Management Program

College of Food, Agriculture, and Environmental Sciences

Department of Agriculture, Environmental, and Development Economics

Agriculture Administration Building, Room 235

2120 Fyffe Road Columbus, OH 43201-1067

660-492-7574- Mobile

brown.6888@osu.edu 614-688-8686- Phone aede@osu.edu