IS OPEN Thursdays session will include updates on the CARES Act CFAP and other emerging legal and economic issues Join us and share your questions concerns and topics of interest Each office hour will include a short update and lead into a question and answer time on additional topics o ID: 1027396

Download Presentation The PPT/PDF document "The OSU Extension FARM OFFICE" is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

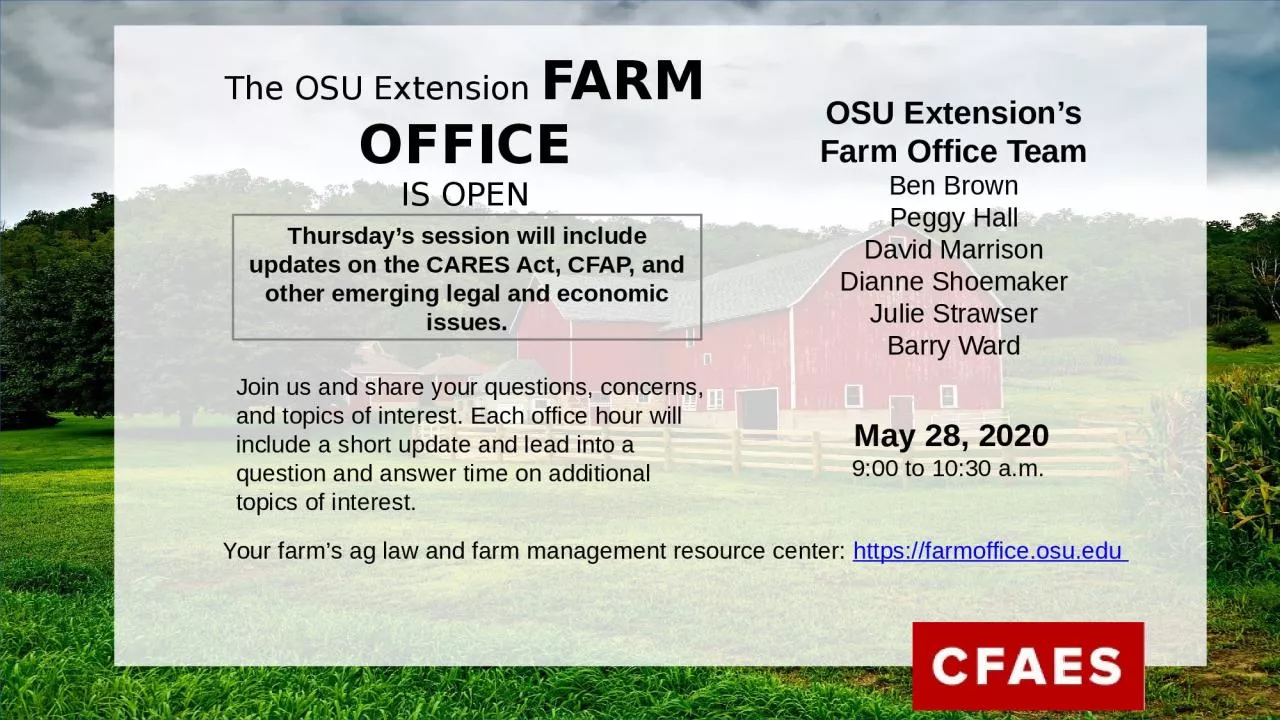

1. The OSU Extension FARM OFFICEIS OPENThursday’s session will include updates on the CARES Act, CFAP, and other emerging legal and economic issues.Join us and share your questions, concerns, and topics of interest. Each office hour will include a short update and lead into a question and answer time on additional topics of interest. OSU Extension’sFarm Office TeamBen BrownPeggy HallDavid MarrisonDianne ShoemakerJulie StrawserBarry WardMay 28, 20209:00 to 10:30 a.m. Your farm’s ag law and farm management resource center: https://farmoffice.osu.edu

2. Farm Office Team

3. Update of the CARES ACT Paycheck Protection Program

4. Good-faith certification “Current economic uncertainty makes this loan request necessary to support the ongoing operations of the Applicant.”SBA safe harborsPPP loans with an original principal amount of less than $2 million will be deemed to have made the required certification concerning the necessity of the loan request in good faithWill be eligible for the Employee Retention CreditLoans over $2 million are subject to SBA reviewThe CARES Act Paycheck Protection Program

5. Paycheck Protection Program Loans (Forgivable) are still an optionU.S. Treasury: PPP Loan Amounts Approved $511.2B, Total appropriated $659BFarmers can apply for forgivable loans: Employee compensation, owner-employees and self-employed payroll compensation, non-payroll costsThe CARES Act Paycheck Protection Program

6. Loan Forgiveness PPP Loan Forgiveness Application – May 15PPP Loan Forgiveness Interim Final Rule - May 22Information on what qualifies as payroll, details on eligible non-payroll costs, timing of expenditures within the covered period, and forgiveness reductions including FTE equivalencies and salary/wage reductions.The CARES Act Paycheck Protection Program

7. Legislation provisions being discussedExtend 8 week covered period to 12/16/24 weeksReduce/Eliminate the 75% payroll requirementReverse Treasury’s position that forgiven expenditures under PPP are not tax deductibleExtend filing deadline to DecemberPPP loans may be used for personal protective equipment for employees and to pay for other "adaptive investments" needed to reopen safely, such as drive-thru window expansions and sneeze guardsThe CARES Act Paycheck Protection Program

8. Coronavirus Food Assistance Program (CFAP)https://u.osu.edu/ohioagmanager/2020/05/20/sign-up-for-usda-cfap-direct-support-to-begin-may-26-2020/

9. Coronavirus Food Assistance Program (CFAP)https://u.osu.edu/ohioagmanager/2020/05/20/sign-up-for-usda-cfap-direct-support-to-begin-may-26-2020/

10.

11. Coronavirus Impact: CFAP- Direct Support Spending$9.5 Billion from CARES Act- Passed in March- Intended to “help offset sales losses and increased marketing expenses associated with the COVID-19 Pandemic”$6.5 Billion from the Commodity Credit Corporation (CCC) “Funding will compensate producers due to on-going market disruptions and will assist with the transition to a more orderly marketing system as the pandemic wanes.”$16 billion in total payments. Source: USDA-Cost Benefit Analysis- adds up over 16 billion due to payment limitations.

12. Limited to $250,000 per individual or $750,000 per entity.Payments split into 3 parts for specialty crops & 2 parts for non-specialty crops and livestock.80% of payment will be released when application is approved. 20% held. May be paid later.Producers must retain documentation in support of their application for 3 years.Payments & Payment Rates

13. Coronavirus Impact: CFAP-Commodities-5%Can supply specialty crop price declines if requested. *Poultry-I find that broilers had a 21% price decline but did not receive payments.Eggs saw a price increase over the period.Price change was betweenJanuary 13-17 and April 6-9Source: Futures prices from respective trading board and Agricultural Marketing Service

14. Includes malting barley, corn, oats, soybeans, and sorghum. Does not include soft red winter wheat. The formula to calculate non-specialty crops and wool has two parts: Part 1: The lesser of either 50% of 2019 production or the unpriced inventory on hand as of January 15, 2020 multiplied by 50% and the CFAP per unit rate per commodity. Part 2: The lesser of either 50% of 2019 production or the unpriced inventory as of January 15, 2020 multiplied by 50% and the CCC per unit rate per commodity. Non-Specialty Crops & Wool

15. Table 2: Payment rates for non-specialty crops, dairy, and livestockCommodityUnitCARES Act Payment Rate ($/unit)CCC Payment Rate ($/unit)Average Payment Rate for Grain*Barley (malting)bushel$0.34$0.37$0.355Canolapound$0.01$0.01$0.01Cornbushel$0.32$0.35$0.335Durum Wheatbushel$0.19$0.20$0.195Hard Red Spring Wheatbushel$0.18$0.20$0.19Milletbushel$0.31$0.34$0.325Oatsbushel$0.15$0.17$0.16Sorghumbushel$0.30$0.32$0.31Soybeansbushel$0.45$0.50$0.475Sunflowerspound$0.02$0.02$0.02Upland Cottonpound$0.09$0.10$0.095Dairyhundredweight$4.71$1.47--Slaughter Cattle- Mature cattlehead$92$33--Slaughter Cattle-Fed cattlehead$214$33--Feeder cattle less than 600 poundshead$102$33--Feeder cattle 600 pounds or morehead$139$33--All other cattlehead$102$33--Pigshead$28$17--Hogshead$18$17--Lambs and Yearlingshead$33$7--Wool (graded, clean basis)pound$0.71$0.78--Wool (non-graded, greasy basis)pound$0.36$0.39--

16. Must meet three conditions.CFAP: Eligible InventoryCondition 1: Eligible InventoryCondition 2: Unpriced InventoryCondition 3: Subject to Price RiskThe lower of:self-certified unpriced inventory; vested ownership as of January 15, 2020 or50% of 2019 production.Ohio FSA on a call yesterday confirmed that corn chopped for silage in 2019 counts a production and any held on January 15, counts for the corn payment. “any production that is not subject to an agreed upon price in the future through a forward contract, agreement or similar binding document”(Final Rule- USDA FSA)Basis contract are eligible.No clarity as of 5/27/20 on delayed/deferred prices or long futures contracts. “any production, sales, and inventory that is not subject to an agreed-upon price in the future through a forward contract, agreement or similar binding document” and “must still be at risk of price fluctuations after January 15, 2020 to be eligible”

17. Scenario: 40,000 bushels of unpriced corn on hand 1/15/2020 representing 40% of 2019 production. 18,000 bushels of unpriced soybeans on hand 1/15/2020 representing 90% of 2019 production. Example for Non-Specialty Crops & WoolCrop50% of 2019 production(bushels)Jan. 15 inventory (bushels)Rate per bushelTotalCorn50,00040,000 $0.335$13,400Soybean10,00018,000$0.475$4,750Total$18,15080% First Installment$14,52020% Second Installment$3,630Formula Reminder(50% * (Lesser of 50% of 2019 production or inventory Jan. 15) * CFAP Rate) +(50% * (Lesser of 50% of 2019 production or inventory Jan. 15) * CCC Rate)Simplified Formula100% * (Lessor of 50% of 2019 production or inventory Jan. 15) * average payment rate

18. The formula to calculate the dairy payment has two parts:Part 1 is based on the producer’s certified milk production during the first quarter of 2020 (January through March) times $4.71/cwt. The CARES rate represents 80% of the USDA calculated first quarter price decline. Part 2 multiplies first quarter production by 1.014 (adjusting for increased second quarter production) times $1.47/cwt. The CCC payment rate representing 25% of the calculated price decline. Dairy

19. CFAP Dairy CalculationExample:A herd with 100 milking cows ships an average of 80 pounds of milk per cow per day or a total of 7,280 cwt. of milk January – March 2020 7,280 cwt x $4.71 = $34,288.80 + (7,280 cwt x 1.014) x $1.47 = $10,851.42 $34,288.80 + $10,851.42 = $45,140.22 Gross payment $45,140.22 x 0.8 = $36,112.18 first payment

20. Includes cattle, sheep (yearlings and lambs only), and hogs. Dairy milk is eligible but has a separate payment calculation. Separate payment rates exist for cattle and hogs of different size and age classifications: slaughter cattle-mature cattle, slaughter cattle-fed cattle, feeder cattle less than 600 pounds, feeder cattle 600 pounds or more; all other cattle, pigs (less than 120 pounds) and hogs. Livestock

21. The formula to calculate livestock payments has two parts: Part 1: Livestock sales (number of head) between January 15, 2020 and April 15, 2020 multiplied by the corresponding animal species CFAP payment rate per head.Part 2: The highest amount of livestock inventory (number of head) on any day between April 16, 2020 and May 14, 2020 multiplied by the corresponding species CCC payment rate per head. Livestock

22. Table 2: Payment rates for non-specialty crops, dairy, and livestockCommodityUnitCARES Act Payment Rate ($/unit)CCC Payment Rate ($/unit)Average Payment Rate for Grain*Dairycwt$4.71$1.47--Slaughter Cattle- Mature cattlehead$92$33--Slaughter Cattle-Fed cattlehead$214$33--Feeder cattle less than 600 poundshead$102$33--Feeder cattle 600 pounds or morehead$139$33--All other cattlehead$102$33--Pigshead$28$17--Hogshead$18$17--Lambs and Yearlingshead$33$7--Wool (graded, clean basis)pound$0.71$0.78--Wool (non-graded, greasy basis)pound$0.36$0.39--

23. Scenario: 50 head of feeder cattle more than 600 pounds sold 3/20/20 and 100 head of other cattle 5/01/2020. (Animals (head) sold 1/15/20-4/15/20 * CARES Rate)+(Head of unpriced animals 4/16/20-5/14/20 * CCC Rate)(50 head * $139) = $6,950 +(100 head * $33) = $3,300 Total Payment of $10,250 (80% will be paid up front)Example for Livestock

24. Payment rates for specialty crops CommodityCARES Act Payment Rates for Sales Losses ($/lb.)Column 2CARES Act Payment Rate for Product that left the farm, but spoiled due to loss of marketing channel ($/lb.)Column 3CCC Payment Rate ($/lb.)Column 4Almonds$0.26$0.57$0.11Apples--$0.18$0.03Artichokes$0.66$0.49$0.10Asparagus--$0.38$0.07Avocados--$0.14$0.03Beans$0.17$0.16$0.03Blueberries--$0.62$0.12Broccoli$0.62$0.49$0.10Cabbage$0.04$0.07$0.01Cantaloupe--$0.10$0.02Carrots$0.2$0.11$0.02Cauliflower$0.11$0.31$0.06Celery--$0.07$0.01Corn, sweet$0.09$0.13$0.03Cucumbers$0.13$0.15$0.03Eggplant$0.07$0.15$0.03Garlic--$0.85$0.17Grapefruit--$0.11$0.02Kiwifruit--$0.32$0.06Lemons$0.08$0.21$0.04Lettuce, iceberg$0.20$0.15$0.03Lettuce, romaine$0.07$0.12$0.02Mushrooms--$0.59$0.11Onion, dry$0.01$0.05$0.01Onions, green--$0.30$0.06Oranges--$0.14$0.03Papaya--$0.32$0.06Peaches$0.08$0.32$0.06Pears$0.08$0.18$0.03Pecans$0.28$0.93$0.18Peppers, bell$0.14$0.22$0.04Peppers, other$0.15$0.22$0.04Potatoes $0.04$0.01Raspberries $1.45$0.28Rhubarb$0.15$1.03$0.20Spinach$0.37$0.37$0.07Squash$0.72$0.39$0.08Strawberries$0.84$0.72$0.14Sweet Potatoes--$0.18$0.04Tangerines--$0.22$0.04Taro--$0.23$0.05Tomatoes$0.64$0.38$0.07Walnuts--$0.45$0.09Watermelons--$0.02--Specialty Crops45 Commodities (Full list in bulletin)3 Part FormulaTotal Sales between 1/15/20 and 4/15/20 * Column 2+ Crops harvested and shipped but subsequently spoiled due to loss of market between 1/15/20 and 4/15/20 * Column 3+Unpriced specialty crops that did not leave the farm or mature crops that remained unharvested between 1/15/20 and 4/15/20 * Column 4

25. Scenario: A producer sold 1,000 pounds of tomatoes on 3/1/20, had 200 pounds shipped but unpaid, and had 4,000 pounds rot in the hoop house. Example for Specialty Crops1,000 pounds sold tomatoesX$0.64200 pounds shipped but unpaid tomatoesX$0.384,000 pounds unharvested (rotted in the field)X$0.07$640$76$280++++Total Payment of $99680% First Installment $796.8020% Second Installment $199.20

26. FSA will have calculator: farmers.gov/cfap

27. Questions?

28. Barry Ward 614.688.3959 or ward.8@osu.eduPeggy Hall937.645.3123 or hall.673@osu.eduBen Brown614.688.8686 or brown.6888@osu.eduDianne Shoemaker330.533.5538 or shoemaker.3@osu.eduDavid Marrison740.622.2265 or marrison.2@osu.eduJulie Strawser614.292.2433 or strawser.35@osu.eduContact Information

29. The OSU Extension FARM OFFICEWILL BE OPEN AGAINThursday, June 11, 20209:00 to 10:30 a.m.Register at: https://go.osu.edu/farmofficelive