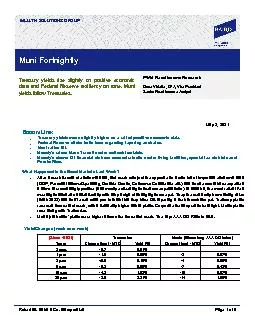

WEALTH SOLUTIONS GROUP Treasuryields rise slightly on positive economic data and Federal Reserve resiliencyon tone Muni yields follow Treasuries Bottom Line reasury yields move slightly higher on a ID: 834963

Download Pdf The PPT/PDF document "Robert W Baird Co IncorporatedPage of" is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

1 Robert W. Baird & Co. IncorporatedPage o

Robert W. Baird & Co. IncorporatedPage of WEALTH SOLUTIONS GROUP Treasuryields rise slightly on positive economic data and Federal Reserve resiliencyon tone. Muni yields follow Treasuries. Bottom Line: reasury yields move slightly higher on a raft of positive economic data. (Since 4 / 1 /2 1 ) Treasuries (Bloomberg AAA GO Index) Tenor Change (bps) - MTD Yield (%) Change (bps) - MTD Yield (%) 3 mos. - 0. 7 0. 0 1 % 1year - 1. 6 0. 0 5 % - 2 0. 0 7 % 2 year 0. 0 0.1 6 % - 4 0. 09 % 5 year - 5.2 0. 8 5 % - 7 0. 4 2 % 10 year - 4.3 1. 6 3 % - 10 0.97 % 30 year - 2.8 2. 3 1 % - 14 1. 65 % David NViolette, CFA, Vice PresidentSenior Fixed Income Analyst Muni Fortnightly PWM Fixed Income Research Dave Violette, CFA, Vice President Senior Fixed Income Analyst Muni Fortnightlycontinued ��Robert W. Baird & Co. IncorporatedPage of Yield Curve and Muni Curve Changes (since 3/14/21)One can observe these changes by looking at how rates have changed along the curve for both the Treasury curve and for the AAArated G.O. Index since last week. The top panel shows four yield curves; two for the Treasury curve one for the most current date and one from last week and two for the AAArated G.O. current and last week. The bottom panel of the graph showschanges in the rates along both curves for the week for both Treasuries and the AAA G.O. Index. Data Source: BloombergThe 10yr AAA GO Ra

2 tiois 59.6The line graph to the right sh

tiois 59.6The line graph to the right shows the ratio of 10year AAArated muni yields to the 10year Treasury yield over the last year. Data Source: BloombergThe Bloomberg 30Day Visible Supplycurrently standat 1.0billionyeardate average is 10.5 billion andthe mo average is $billion. Data Source: Bloomberg Muni Fortnightlycontinued ��Robert W. Baird & Co. IncorporatedPage of Articles of Interest Muni Fund Flows: According to Refinitiv Lippermuni funds had net inflowsof $1.64illion last week. ETFs and highyield funds also had net inflows for the week. Mass Transit Outlook Improves (Moody’s): Moody’s issued anew Mass Transit sector Outlook, revising it to Stable from Negative. The rationale for the outlook change includes: 1) incremental Federal assistance through The American Rescue Plan Act which includes $30.5 billion to support the industry after two smaller assistance packages earlier on during the pandemic. 2) An expectation of improved tax collections upon the improvement in the economy. 3) They note that changing commuter behavior will remain a challenge to the sector. Higher Education Private Education Sector Demonstrated Flexibili(Moody’s): In a Sector Profile, Moody’s describes the private higher education as demonstrating flexibility during fiscal 2020 during Covid. The highlights of the report include: 1) Larger private universities remained in a stronger financial position as compared to smaller private schools. Fifty percent of privates saw operating revenue declines in 2020 as compared to 20% seeing a declinein 2019. 2) Private universities showed their flexibility by cutting expenses alongside the reductions in revenues to

3 maintain an a nearly unchanged operatin

maintain an a nearly unchanged operating cash flow margin. 3) Onethird of the rated universities saw net tuitions decline with a median drop of 4.6%. 4) Private universitiesreserves and liquidity were maintained. 5) Universities turned more to public financing, away from internal reserves, for capital projects. Muni Sector Delinquencies/Reserve Draws etc. (Moody’s):Moody’s summarized the 96 material financialdifficulty credit events of Q1 2021. The credit events of Q1 were concentrated among small unrated issuers and were concentrated among senior living facilities, special tax districts (TIF districts) and Puerto Rico. They commented that given the significance of Covid on the economy that municipal delinquencies and reserve draws were less prevalent that they expected. State Ratings Changes SummaryMoody’s issued the following credit rating changes for states in Q1 2021: 1) Upgraded Connecticut from A1 to Aa3, 2) revised the State of Illinois from negative to stable, 3) revised the outlook for Louisiana from stable to positive, and so far in Q2 4) revised the State of New jersey from negative to stable. Muni Fortnightlycontinued ��Robert W. Baird & Co. IncorporatedPage of Puerto Rico S&P Municipal Bond Puerto Rico Index Level (1year)The S&P Municipal Bond Puerto Rico Indexinished at 1.3vs. 28.2in midMarch1.4%, 2.4% YTD Relative Value by Maturity Table 1 AAA Muni Ratios and Spreads by Maturity Data Source: Bloomberg Relative Value by Rating Figure 5 Muni Index Yield Curve by Credit Rating Data Source: BloombergFor more information please contact your Financial Advisor. 4/30/2021Maturity (yrs.) AAA Gen. Oblig. Treasury Spread (bps) Ratio (%) Spread (bps) Ratio (%) 0.080.047.7181.07.7278.40.100.16-1.359.9-1.392.

4 10.170.33-6.552.3-6.580.50.320.60-10.553

10.170.33-6.552.3-6.580.50.320.60-10.553.6-10.582.40.430.85-19.450.2-19.477.20.651.31-31.349.4-31.376.10.971.63-12.959.8-12.992.11.271.868.568.08.5104.61.432.182.465.72.4101.11.592.2420.470.920.4109.11.652.3123.571.623.5110.2 0% Tax Rate 35% Tax Equivalent Yield-to-worst (%) Muni Fortnightlycontinued ��Robert W. Baird & Co. IncorporatedPage of Appendix Important Disclosures Some of the potential risks associated with fixed income investments include call risk, reinvestment risk, default risk and inflation risk. Additionally, it is important that an investor is familiar with the inverse relationship between a bond’s price and its yield. Bond prices will fall as interest rates rise and vice versa.When considering a potential investment, investors should compare the credit qualities of available bond issues before they invest. The two most recognized rating agencies that assign credit ratings to bond issuers are Moody's Investors Service (“Moody’s”) and Standard & Poor's Corporation (“S&P”). Moody’slowest investmentgrade rating for a bond is Baa3 and S&P’s lowest investmentgrade rating for a bond is BBBRatings are measured on a scale that ranges from AAA or Aaa (highest) to D or C (lowest).The Bond Buyer 20Bond Index consists of 20 general obligation bonds that mature in 20 years. The average rating of the 20 bonds is roughly equivalent to Moody's Investors Service's Aa2 rating and Standard & Poor's Corp.'s AA. The Bond Buyer 11Bond Index uses a select group of 11 bonds in the 20Bond Index.The average rating of the 11 bonds is roughly equivalent to Moody's Aa1 and S&P's AAplus. The Bond Buyer Revenue Bond Index consists of 25 various revenue bonds that mature in 30 years. The average rating is roughly equivalent to Moody's A1 and S&P's Alus. The indexes represent theoret

5 ical yields rather than actual price or

ical yields rather than actual price or yield quotations. Municipal bond traders are asked to estimate what a currentcoupon bond for each issuer in the indexes would yield if the bond was sold at par value. The indexes are simple averages of the average estimated yields of the bonds, are unmanaged and a direct investment cannot be made in them.This is not a complete analysis of every material fact regarding any sector, municipality or security. The opinions expressed here reflect our judgment at this date and are subject to change. The information has been obtained from sources we consider to be reliable, but we cannot guarantee the accuracy. Municipal securities investments are not appropriate for all investors, especially those taxed at lower rates. The alternative minimum tax (AMT) may be applicable, even for securities identified as taxexempt. It is strongly recommended that an investor discuss with their financial professional all materially important information such as risks, ratings and tax implications prior to making an investment. Past performance is not a guarantee of future results.This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.ADDITIONAL INFORMATION ON SECURITIES MENTIONED HEREIN IS AVAILABLE UPON REQUEST BY CONTACTING YOUR BAIRD INVESTMENT PROFESSIONAL.Copyright 202Robert W. Baird & Co. Incorporated