September 13 2012 Presentation to Macro Financial Modeling Conference Dale Gray IMF Monetary and Capital Markets Department The views expressed in this presentation are those of the authors ID: 1027445

Download Presentation The PPT/PDF document "Using Contingent Claims Analysis (CCA) t..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

1. Using Contingent Claims Analysis (CCA) to Measure and Analyze Systemic Risk, Sovereign and Macro Risk September 13, 2012Presentation to Macro Financial Modeling Conference Dale Gray, IMF, Monetary and Capital Markets Department The views expressed in this presentation are those of the authors and should not be attributed to the International Monetary Fund, its Executive Board, or its management.

2. 2Outline of PresentationTraditional AnalysisContingent Claims Analysis (CCA)Applications of CCA: Macro Financial CCA: Non-linear Risk TransmissionEstimating Government Contingent LiabilitiesSystemic Risk Analysis (Application to US)Sovereign CCA models and Sovereign-Banking Destabilization SpiralsIntegrated Policy Analysis

3. 3Outline of Presentation (cont.)Presentation is based on material in: Gray, D. F., Merton R. C. and Z. Bodie, 2008, “A New Framework for Measuring and Managing Macrofinancial Risk and Financial Stability,” Harvard Business School Working Paper No. 09-015. Gray, D., A. Jobst, 2011, “Modeling Systemic Financial Sector and Sovereign Risk,” Sveriges Riksbank Economic Review, September.As well as: Book: Macrofinancial Risk Analysis; other IMF, JOIM, Annual Review of Financial Economics (2009 and 2012) and related papers Financial Risk Indicators in Monetary Policy Models (joint work with Central Bank of Chile IMF WP 11/228)International Transmission of Macro, Sovereign, Financial, and Corporate Distress (joint work with ECB CCA- GVAR Model of EU)

4. 4 Traditional Analysis is IncompleteTraditional macroeconomic and banking models do not adequately measure risk exposures of financial institutions and sovereigns and cannot be used to understand the transmission and amplification of risk within and between balance sheets in the economy. Traditional macroeconomic analysis of the government and central bank is almost entirely flow or accounting balance sheet based. Sovereign debt analyses focus on debt sustainability (stocks, flows and debt to GDP), not sovereign risk exposures (contingent liabilities, expected losses on sovereign debt). A fundamental point is that accounting balance sheets or a flow-of-funds do not indicate risk exposures, which are forward-looking.

5. 5 CCA Balance Sheet Models and Macroeconomic ModelsMacroeconomic models are largely based on flow and accounting balance sheets, geared to try to forecast the mean of macro variables (i.e. first moment)Finance measures risk from stochastic assets relative to threshold (second and third moments critical to risk indicators).CCA is an excellent tool for analyzing macrofinancial linkagesTime pattern of CCA risk indicators can be linked to macroeconomic variables and to monetary policy, DSGE, and other models

6. 6Added Dimension of Risk Indicators CCA Risk Analytics Models to Spectrum of Macroeconomic Models

7. 7Macrofinancial Risk AnalysisFramework integrates risk-adjusted balance sheets using Contingent Claims Analysis (CCA) of financial institutions, corporates, and sovereigns together and with macroeconomic and monetary policy models TOOLKIT FOR MACRO RISK ANALYSIS

8. 8Core Concept of Contingent Claims Analysis (CCA): Merton Model Assets = Equity + Risky Debt = Equity + Default-Free Debt – Expected Loss = Implicit Call Option + Default-Free Debt – Implicit Put Option AssetsEquity or Jr ClaimsRisky Debt Value of liabilities derived from value of assets. Liabilities have different seniority. Randomness in asset value.

9. CCA is Generalization of Black, Scholes, Merton Option Pricing Theory Liabilities derive their value from assetsAssets are stochastic (changes driven by income flows, asset sales, or changes in value, including credit risk/guarantees)Uncertain changes in future asset value, relative to the promised payments on debt are the driver of forward-looking values of equity and risky debt.Risky debt is default-free debt value minus the expected loss due to default which can be measured with an implicit put option. Key elements are Asset value (A) at time 0, asset return volatility (σ), default barrier (B = PV of promised payments on debt, time horizon (T) and risk-free rate (r).Note : one does not have to know the expected returns to use CCA/Merton models for valuation of liabilities!9

10. 10Tradeoffs between Market Capitalization, Market Value of Assets and Default Probability (Moody’s KMV data)CITIGROUP EXAMPLE: From Sept 9, 2008 to March 9, 2009, Market Capitalization fell from $125 bn to $6 bn, Assets declined and Default Probability went from 0.5% to 24%To get back to a BBB+ rating (0.3% EDF) combinations of capital injection, asset guarantees, debt-equity swaps can be evaluated; during TARP 107bn in capital was raised

11. CCA is Based on Proven, Well-tested Calibration TechniquesTools and techniques for calibrating CCA balance sheets of corporates and financial institutions are decades old (as described in HBR 2008 paper). Even commercial sources available (e.g. Moody’sKMV provide CCA risk indicators daily for 40,000 firms and financial institutions in over 60 countries)Extensions to sovereigns and economy-wide risk transmission is becoming widespreadOver 20 countries have been calibrated; 35 sovereigns; CCA now included in several IMF FSAPs; recent integration into DSGE/monetary policy models and CCA GVAR (Global and EU)11

12. As a result of the crisis, CCA concepts have now found their way into the mainstreamThe structural CCA model, with its embedded fundamental volatility, endogenously changes as values change (e.g. shocks to assets endogenously change values of equity and risky debt and credit risk premiums)It helps explain complex risk, especially expected losses in financial system and “insidiousness” of risk exposures where small changes in value can lead to very large changes in risk due to convexity! 12

13. CCA has robustnessIt does not depend on expected returns;It does not depend on preferences;It is designed to be modular (can be integrated with many models of consumption and investment);Retains the (endogenous) non-linearity of values and risk exposures, and can linked to macro models in different ways.13

14. For the remainder if my presentation I will describe several ways CCA can be applied to enhance financial stability and macroeconomic analysis1. Non-linear risk transmission across sectors of an economy 2. Estimating government contingent liabilities 3. Systemic CCA: Measuring Financial Sector Tail-risk Losses And Contingent Liabilities 4. Applying CCA To The Sovereign Balance Sheet; Framework For Sovereign-Bank Feedback Destabilization Processes5. Unified Macrofinancial Policy FrameworkFurther Applications 14

15. 1. NON-LINEAR RISK TRANSMISSION ACROSS SECTORS OF AN ECONOMY Risky debt of households and corporates are assets on financial institution balance sheets and implicit and explicit guarantees of bank’s liabilities are on the sovereign balance sheet 15

16. 16CCA Balance Sheet: Assets Minus Liabilities equal ZeroCCA Balance Sheet Assets+or - Implicit or Explicit Guarantees {Implicit Put Options}minus Equity / Jr. Claim {Implicit Call Option}minus(Default-free Value of Debt – Implicit Put Option)= 0For a sector, sub-sector or individual institution

17. Stylized Interlinked CCA Balance Sheets for an Economy17Sectors of an economy can be viewed as interconnected risk-adjusted balance sheets with portfolios of assets, liabilities, and guarantees—explicit and implicit.

18. 18Economy-wide CCA Balance Sheet Models Capture Non-linear Risk TransmissionInterlinked implicit options result in compound options that exhibit highly non-linear risk transmission, as seen a variety of financial crises Note that if asset volatility in CCA balance sheets is set to zero:Implicit put options go to zero,Macroeconomic accounting balance sheets and traditional flow-of-funds are the result Measurement of (non-linear) risk transmission is not possible using macroeconomic flow or accounting frameworks when fundamental structural volatility is ignored (i.e. = 0).

19. Examples of Channels of Risk TransmissionCorporates/Households BanksBanks SovereignsSovereigns Sov Debt HoldersFinancial System Risk GDP GrowthFinancial Sector Sovereign GDP Growth19

20. Example of Transmission of Risk from Corporate Sector to Banks to Sovereigns: Case of Thailand My initial work was motivated to try to understand Asia crisis. First model was a simple: four corporate sectors, two bank sectors, sovereign model for the Thai economy in the 1990s. Large amounts of foreign debt and pegged exchange rate. This simple model showed: Corporate risk is embedded in the banking risk. The sensitivity (delta) and convexity (gamma) of banking sector risk increased as the exchange rate depreciates (insidious risk).20

21. Example of Transmission of Risk from Corporate Sector to Banks to Sovereigns: Case of Thailand (cont.)21In fact, by using forward exchange rate level and volatility plus balance sheet data (available at the time), the probability distribution of financial sector losses was 25% of GDP, BEFORE the spot rate moved from its pegged level!Actual losses reached around 40% of GDP

22. 22 2. ESTIMATING GOVERNMENT CONTINGENT LIABILITIES AND RISK TRANSMISSION TO SOVEREIGNImplied credit spreads derived from CCA models (i.e. derived from equity information) are frequently higher than the observed market CDSThis is due to the depressing effect of implicit and explicit government guaranteesThe ‘market implied’ guarantees (implicit put option values) can be estimated using CCA and observed CDS

23. 23Citigroup: Example of Implicit Put Option Value Extracted from CDS vs from CCA model and Estimated Contingent Liability (billions of US$) Estimated “market implied" government continent liability

24. Transfer of Risk: Ireland CDS spreads of banks declined following guarantees in 4Q 2008 and sovereign spread increases

25. 25Transfer of Risk to Sovereign: Austria Example – CCA Banking Contingent Liabilities vs Sovereign CDS spread

26. Note how CCA financial sector risk indicators (aggregated financial institution CCA indicator related to expected losses) provides: A robust measure of financial sector systemic risk;Frequently a leading indicator of credit growth and GDP/output gap;Provides a quantitative measure of government contingent liabilities, which affects sovereign risk (e.g. spreads) 26

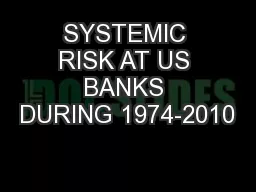

27. 3. SYSTEMIC CCA: MEASURING AND STRESS TESTING FINANCIAL SECTOR TAIL-RISK LOSSES AND CONTINGENT LIABILITIES 27Beginning with CCA models of individual banks, expected losses and market implied contingent liabilitiesMultivariate extreme value dependence model is then used to calculate the multivariate density of: (i) the banking system expected losses, and,(ii) government’s contingent liabilities accounting for the time-varying and non-linear dependence(iii) measures of financial sector tail risk (95% VaR or Expected Shortfall) (See Gray and Jobst Swedish Economic Review 2011, and 2009, 2010, & forthcoming)

28. Extreme Tail Risk Total Expected Losses including dependence structure, 36 largest US financial institutions, 95th percentile28Source: IMF US Financial Sector Assessment Program Stress Testing Technical Note 2010

29. Extreme Tail Risk Government Contingent Liabilities including dependence structure, 36 largest financial institutions, 95th percentile 29Source: IMF US Financial Sector Assessment Program Stress Testing Technical Note 2010

30. Systemic CCA Shows Nonlinearities of Asset Volatility, Market Capital/Assets, Fair Value Credit Spreads, and Joint Losses – for individual institutions and for the system as a whole (illustrated below)30

31. 4. APPLYING CCA TO THE SOVEREIGN BALANCE SHEET; FRAMEWORK FOR SOVEREIGN BANK FEEDBACK DESTABILIZATION PROCESSES 311. Calibrating sovereign balance sheets for emerging market sovereigns with significant foreign currency debt (see Gray, Merton, Bodie 2007 JOIM paper; Gapen et al. IMF Staff Papers 55 #1)2. Calibrating developed country sovereign balance sheets or government balance sheets in euro area. Calibration uses term structure of CDS/bonds plus debt data to infer sovereign assets, volatility and skew (see Gray, Jobst Swedish Economic Review, page 24 and Appendix 3).

32. 32Sovereign CCA Balance Sheet, Contingent Liabilities, Joint Bank-Sovereign Stress Testing Sovereign, or Government, CCA model gives implied sovereign asset value and volatility, whose components can be estimated as shown below: ASov = Reserves + PV (primary fiscal surplus) – Contingent Liabilities to Financial sector + Other (residual) Sovereign spreads = f (sovereign assets, volatility, debt default barrier, time horizon, risk-free rate) Joint stress testing of banks and sovereigns can be carried out: macro variables affect bank CCA, and thus contingent liabilities, and fiscal surplus and in turn sovereign spreads (Swedish Economic Review paper shows example on page 24 and 25 of base and adverse stress test of bank expected losses and sovereign spreads.)

33. Linkages between Stylized Financial Sector and Sovereign CCA Balance Sheets33 FINANCIAL SECTORGOVERNMENTASSETSAssets (including government debt)/Loans/Other Assets+ Liquid Assets/Reserves+ Asset GuaranteesPresent value of (Fiscal Surplusand Guarantee fees)+ Equity (government owned)+ Other AssetsLIABILITIES - Equity (non-government) - Equity (government-owned)- Credit owed to Central Bank- Asset Guarantees- Default-free Debt & Deposits+ (1-α) *Expected Losses due to Default - α* Expected Losses due to Default - Present value of Guarantee fees- Default-free Sovereign Debt+ Expected Losses due to Sovereign Default ASSETS MINUS LIABILITIES00 Source: Gray Jobst 2010, and Swedish Economic Review 2011The circular linkage of bank expected losses and expected losses on sovereign debt can create an insidious destabilization spiral

34. 34

35. 35CCA Risk Exposures Facilitate Quantitative Analysis of Risk Mitigation Policy OptionsBanks:Increase bank capital higher assets, lower expected losses Portfolio adjustment/ring-fenced asset guarantees Lower asset volatilityDebt to equity conversion lower default barrier, higher equity Guarantees on bank debt lower borrowing spreads Sovereigns:Increase debt maturity lower default barrierFiscal adjustment (“Fiscal Compact”) higher sovereign assetsGuarantees/insurance on sovereign debt lower sovereign spreadsSupranational:Debt purchases by public entity (ECB, EFSF, ESM, other) lower sovereign spreadsEurobonds lower sovereign spreads, risk diversification

36. 365. UNIFIED MACROFINANCE FRAMEWORK Targets: Inflation, GDP, Financial System Credit Risk, Sovereign Credit Risk Sovereign CCA Balance Sheet ModelMonetary Policy ModelInterest Rate Term Structure Financial System Credit Risk IndicatorFinancial Sector CCA Model Fiscal Policy Debt Management Reserve Management Policy Rate Liquidity Facilities Quantitative Actions Capital Adequacy Financial Regulations Economic CapitalFiscal and Debt Policies:GuaranteesFinancial Stability Policies:Sovereign Credit Risk IndicatorMonetary Policies:Household CCA Balance Sheet(s)Corporate Sector CCA Balance Sheet(s)Sovereign Equity Claims (from Capital Injections)Global Market Claims on Sovereign

37. 37Traditional Flow and Accounting Framework No Risk-Adjusted Balance Sheets (Asset Volatility = 0) No Credit Risk or Guarantees; No Risk Exposures GovernmentAccounts Flow of FundsMonetary Policy ModelInterest RatesBank Accounting Balance Sheets Fiscal Policy Debt Management Reserve Management Policy Rate Liquidity Facilities Quantitative Actions Capital Adequacy Financial RegulationsFiscal and Debt Policies:Financial Stability Policies:Monetary Policies:Household AccountingBalance Sheet(s)Corporate AccountingBalance Sheet(s)Capital InjectionsGlobal Market FlowsCredit Flows

38. FURTHER APPLICATIONS – New risk-adjusted GDP and external account measures (from economy-wide CCA balance sheets, slide 17)38See Gray, D. F., Jobst, A. A., and S. Malone, 2010, “Quantifying Systemic Risk and Reconceptualizing the Role of Finance for Economic Growth,” Journal of Investment Management

39. 39FURTHER APPLICATIONS (cont.) - Integrating Financial System Risk Indicators into Monetary Policy ModelsGDP is affected by financial stability in the banking system via:Financial accelerator links;Financial distress in banks and bank’s borrowers reduces lending as borrower’s credit risk increases; Explicit inclusion of CCA banking system credit risk indicator in monetary policy models in the output gap equation. Uses a simple two-module framework:Central Bank of Chile Macro Monetary Policy Model.CCA Financial System Module. See Garcia et al. 2011 “Incorporating Financial Sector into Monetary Policy Models: Case of Chile” IMF WP/11/228

40. 40Including CCA Banking Risk Indicator in Bank of Chile Monetary Policy Model: ConclusionsA simple, but powerful model for monetary policy including financial sector risk. Empirical evidence supports the model. Impulse Responses behave according to theory.Robust efficient frontier (inflation volatility vs output volatility) A stronger reaction of interest rates to financial risk indicator reduces inflation volatility and output volatility.

41. FURTHER APPLICATIONS (cont.) - Ongoing Joint work with ECB – CCA-GVAR for EU(Joint work with ECB: Marco Gross, Matthias Sydow, and Joan Paredes)Framework for analysis the interactions of banking sector risk, sovereign risk, GDP growth, stock markets, and other macro variable for 15 EU countries plus the US. Uses CCA risk indicators for the banking systems and corporate sectors and sovereigns in each country, Together with the GVAR (Global Vector Autoregression) model for each country, and weight matrices, impulse responses captures the non-linearity of changes in bank assets, equity capital, bank credit spreads, sovereign spreads and corporate credit risk. 41

42. CCA-GVAR model framework 42

43. 43Conclusions for CCA GVAR ModelIntegrated forward-looking banking system, corporate and sovereign risk indicators in a GVAR with macroeconomy and financial markets;Large panel of banks, sovereigns, macro, financial markets all fully endogenous;Stable global model provides meaningful responses in terms of directions and magnitude;CCA captures nonlinear features related to bank capital, funding cost and sovereign risk;Allows a range of policy options to be modeled and their risk mitigation impact quantified.

44. 44Additional references:Macrofinancial Risk Analysis, Gray and Malone (Wiley Finance book Foreword by Robert Merton)Gray, Dale F., Robert C. Merton, and Zvi Bodie. (2006) “A New Framework for Analyzing and Managing Macrofinancial Risks of and Economy” Harvard Business School Working Paper, No. 07-026, 2006. (Also NBER Working Paper Series, No. 12637.)Gray, D. F., Merton R. C. and Z. Bodie, 2007, “Contingent Claims Approach to Measuring and Managing Sovereign Credit Risk, Journal of Investment Management, Vol. 5, No. 4, pp. 5-28.Gapen M. T., Gray, D. F., Lim C. H., Xiao Y. 2008, “Measuring and Analyzing Sovereign Risk with Contingent Claims,” IMF Staff Papers Volume 55 Number 1 (Washington: IMF). Gray, D. F., Jobst, A. A., and S. Malone, 2010, “Quantifying Systemic Risk and Reconceptualizing the Role of Finance for Economic Growth,” Journal of Investment Management, Vol. 8, No. 2, pp. 90-110.Chen, Q., D. Gray, P. N’Diaye, H. Oura 2010 “International Transmission of Bank and Corporate Distress” IMF Working Paper No. 10/124 (Washington: International Monetary Fund). Garcia, C., D. Gray, L. Luna, J. Restrepo, 2011, “Incorporating Financial Sector into Monetary Policy Models: Application to Chile,” IMF WP/11/22Gray, D. and S. Malone, 2012, “Sovereign and Financial Sector Risk: Measurement and Interactions” Annual Review of Financial Economics, 4:9.Gray, D., M. Gross, J. Paredes, M. Sydow, 2012, “Modeling the Joint Dynamics of Banking, Sovereign, Macro, and Financial Risk using Contingent Claims Analysis (CCA) in a Multi-country Global VAR” forthcomingGray, D. F., and A. A. Jobst, 2012, “Systemic Contingent Claims Analysis (Systemic CCA) – Estimating Potential Losses and Implicit Government Guarantees to Banks,” IMF Working Paper (Washington: International Monetary Fund), forthcoming.