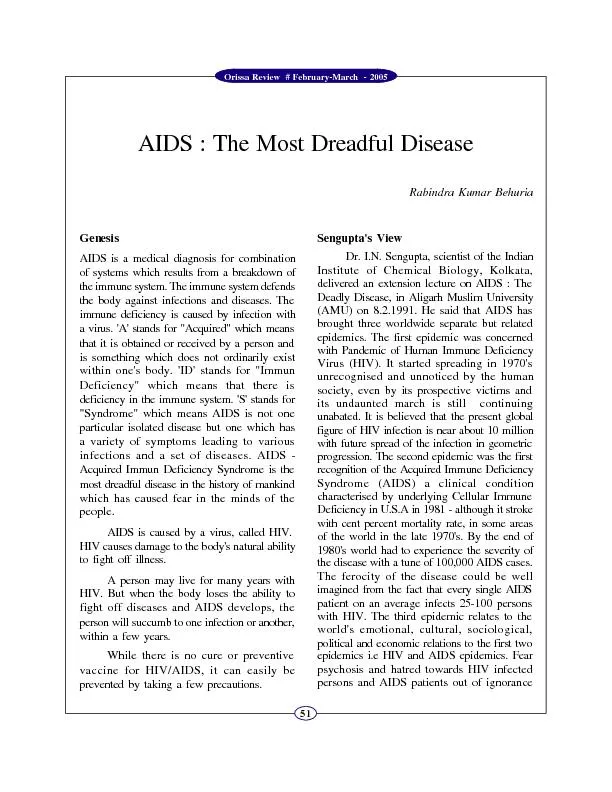

III A look at trading volumes in the euro 0198079801990799 USDEUR DEM in 1998 USDJPYSource EBS BIS Quarterly Review February 2000According to market sources this share increased substanti ID: 822860

Download Pdf The PPT/PDF document "BIS Quarterly Review, February 2000Flore..." is the property of its rightful owner. Permission is granted to download and print the materials on this web site for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

BIS Quarterly Review, February 2000Flore

BIS Quarterly Review, February 2000Florence Branger(41 61) 280 9197florence.beranger@bis.orgGabriele Galati(41 61) 280 8923gabriele.galati@bis.orgIII. A look at trading volumes in the euro01.9807.9801.9907.99USD/EUR (DEM in 1998)USD/JPYSource: EBS.BIS Quarterly Review, February 2000According to market sources this share increased substantially in 1999. Globally, about one third of alltransactions involving the dollar, the yen and the euro are said to be currently effected throughelectronic brokers. Given that electronically brokered transactions cover only a part of FX markets, itwould be misleading to use them as a proxy for total turnover. Subject to this important caveat,however, they support the conclusion reached by looking at traders informal estimates.Another source of information on the role of the euro in FX markets is estimates of trading inemerging market countries. An important issue is whether traders in these countries will transact theirhome currency against the euro much more than they did against its predecessor currencies andwhether the euro might threaten the dollars dominant role. While FX markets in emerging marketcountries are still very small, data on these markets are interesting as qualitative information.In those FX markets, the role of the euro so far seems similar to that of the mark, being confinedmainly to eastern Europe. Hungary is an interesting case because until December 1998 it managed itsexchange rate by reference t

o a currency basket heavily tilted towar

o a currency basket heavily tilted towards the mark. Since January 1999,the euro has taken over this role. The graph below shows that, with a share of total trading involvingthe forint of about 25%, trading against the euro in 1999 was no higher than trading against the markbefore January 1999.Foreign exchange market: HungaryLeft-hand scale: millions of US dollars per working day; right-hand scale: percentage shares01.9804.9807.9810.9801.9904.9907.9910.99HUF/EUR (DEM in 1998) (left-hand scale)HUF against all other currencies (left-hand scale)Share of EUR (DEM in 1998) in total HUF trading (right-hand scale)Source: National Bank of Hungary.In emerging markets outside eastern Europe, the euros role remains limited, as was that of the markpreviously (Galati (1998)). In Thailand and Korea, for example, less than 1% of all transactionsinvolving the domestic currency are conducted against the euro. In South Africa this fraction is onlyslightly higher than 1%. In Brazil, 8590% of all trading of reais against foreign currencies is againstthe dollar. It may be misleading to gauge developments in total FX volumes from electronically brokered volumes alone for tworeasons. First, part of the changes in volumes may be the result of the substantial increase in their market share over thelast 18 months. Moreover, because of the fundamentally different price discovery processes of electronic brokering andother means of FX trading, a decrease in electronically broker

ed volumes may not reflect a reduction i

ed volumes may not reflect a reduction in liquidity. Moreover, when we consider transactions taking place in Hungary that do not involve the local currency, trading volumesfor dollar/euro are not much larger than trading volumes for mark/dollar before 1999. It is interesting to note that localFX trading is still dominated by the dollar, which captures about 75% of total activity.BIS Quarterly Review, February 2000Our analysis suggests that the introduction of the euro has not to date caused major changes in FXmarket activity. The euro made its appearance at a time of reduced overall FX market volumes. Interms of its importance in FX trading, the new currency roughly matches the mark. This appearsplausible given that the euro did not start with a Big Bang. Rather, markets had been preparing forits arrival for several years, as the trends in trading of European cross rates through EBS shows (BIS(1998)).The next BIS triennial central bank survey of foreign exchange and derivatives marketactivity, scheduled for 2001, may be useful to test whether FX markets will by then have found a newnorm.ReferencesBank for International Settlements (1997): 67th Annual ReportBank for International Settlements (1999): Central Bank Survey of Foreign Exchange and DerivativesMarket Activity, May.Bank for International Settlements (1998): 68th Annual ReportGalati, Gabriele (1998): The role of major currencies in emerging foreign exchange markets, in BISQuarterly Review, February.