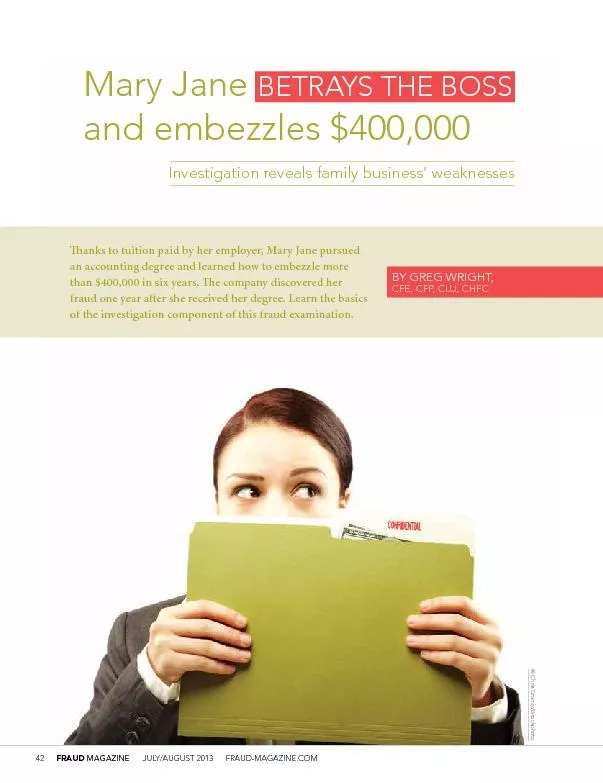

PDF-JULY/AUGUST 2013 FRAUD-MAGAZINE.COMBETRAYSInvestigation reveals f

Author : alexa-scheidler | Published Date : 2016-10-16

Download the PowerPoint presentation from the JULY/AUGUST 2013 FRAUD-MAGAZINE.COMBETRAYSInvestigation reveals f

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "JULY/AUGUST 2013 FRAUD-MAGAZINE.COM..." is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

JULY/AUGUST 2013 FRAUD-MAGAZINE.COMBETRAYSInvestigation reveals f: Transcript

. 275752631Nov 3575267 October 20 2014 October 22 2014 October 24 2014 January 2015 6575267 November 6 2014 December 30 2014 January 2 2015 Re gister with PCAT 574415745457444 schedule with Pearson VUE as seating is on a 57375rstcome 57375rstserved b Jesse Ventura by Lawrence Grobel 20 Questions Cindy Margolis by David Rensin Features Lets Go Racing by Mardi Gras 2000 Elizabeth Cox Show More Show Fewer DO NOT FORGET The Unforgettable wwwshopwikicomlplayboymagazinemaycindymonth GeometryNet Cel Adobe Illustrator/Photoshop lesson. Objective:. 1. Design a magazine cover for a specific TARGET audience.. 2. Demonstrate understanding of the ways in which magazines, their sponsors and their advertisers target and attract audiences. Spring 2015 Leadership =ssue magazine magazine magazine magazine magazine magazine Save the Date W!E! Board Mee�ngs !ll members are =nvited to a�end! May 16, 2015 11am - 1pm Bainb more securities and savings (ex. home). Source: PMB, Fall 2011 : A12+, Heaviest quintiles (1 & 2). $206.2. $126.4. $146.6. $91.7. $184.6. Total. securities. & savings. (ex. home). in millions.. Izzy. Clayton and Tanya Hitchen. Introduction. •. Overview including changes to prior year. •. High-level Timetable. •. CD forms – When to use them, how to use them and examples. •. Internal trading – David Phillips. What are the central securities depositories doing to mitigate this risk?. Cancún, . May. 21, 2015. What is Fraud?. Generally, fraud is described as a deliberate act of abuse of trust, taking advantage of swindles. . Recalibrating Your Heart. Your Heart. Your Heart. Your Heart. H. eart – . leb. (hebrew). -. inner man, mind, will, understanding, inner part, soul, seat of emotions – passions –courage. Heart –. Microworld. Physics . Gomel, Belarus, July 22 - August 2, 2013. The new electro-nuclear method and scheme of energy production and transmutation of radioactive waste components of nuclear power. . By Lauren Whitsell. Scatter Plot. This scatter plot shows data for the US Annual Wages.. The equation generates this line, which was an . r . value of .96. That means the line is extremely close to the data, which means the data rises in a linear fashion.. Missey Jackson, CPP. Payroll Director. Parallon/HCA. Topics. Payroll Fraud. Statistics. Red Flag Indicators. Types of Payroll Fraud. Payroll Fraud Prevention. Recent Payroll Fraud . Cases. Payroll Privacy. The people or animals that take part in a story’s action.. Characters are driven by . motivation. -the reason or reasons they do what they do. .. Character. The way a writer reveals a character’s personality and qualities.. Fraudsters . and Current . Fraud Schemes. Brian . Lopez, CFE, MBA, CIDA. Zach Snickles, CPA, CFF, CITP. What is Fraud?. 2. Definitions of “Fraud”. Black’s Law Dictionary. . (8. th. Ed. 2004) - “A knowing misrepresentation of the truth or concealment of a material fact to induce another to act to his or her detriment. A misrepresentation made recklessly without belief in its truth to induce another person to act. A tort arising from a knowing misrepresentation made to induce another to act to his or her detriment.” . Charity Fraud Charity Fraud Has anyone ever asked you to donate to charity? Real Fundraising Many charities get in touch: By phone By mail By email Charity Fraud Here’s how it works: Phone call Charity name sounds familiar

Download Rules Of Document

"JULY/AUGUST 2013 FRAUD-MAGAZINE.COMBETRAYSInvestigation reveals f"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents