PPT-Intermediate Accounting

Author : conchita-marotz | Published Date : 2020-01-31

Intermediate Accounting Seventeenth Edition Kieso Weygandt Warfield Chapter 1 Financial Accounting and Accounting Standards This slide deck contains animations

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "Intermediate Accounting" is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Intermediate Accounting: Transcript

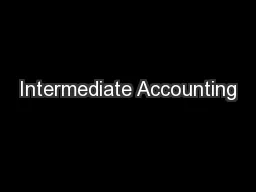

Intermediate Accounting Seventeenth Edition Kieso Weygandt Warfield Chapter 1 Financial Accounting and Accounting Standards This slide deck contains animations Please disable animations if they cause issues with your device. Chapter 22. Accounting for Changes and Errors. © 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.. Chapter 1 . The Demand for and Supply of Financial Accounting Information. © 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.. 1 s Per Share Dr.ChulaKingRights Intermediate Accounting IIDr. Chula King g Part 3: Diluted EPS Chapter 19. Accounting for Postretirement Benefits. © 2013 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.. IFRS 2nd . Edition. Kieso, Weygandt, and Warfield. . 20. Use a worksheet for employer’s pension plan . entries.. Explain . the accounting for past service . costs.. Explain . the accounting for . remeasurements.. 16th . Edition. Kieso . ●. . Weygandt . ●. . Warfield. . Understand . the accounting for investments in debt securities. .. Understand . the accounting for investments in equity securities.. 16th . Edition. Kieso . ●. . Weygandt . ●. . Warfield. . Identify . types of accounting changes and understand the accounting for changes in accounting principles. .. Describe . the accounting for changes in estimates and changes in the reporting entity.. 16th . Edition. Kieso . ●. . Weygandt . ●. . Warfield. . Describe . the nature of bonds and indicate the accounting for bond issuances. .. Describe the accounting for the extinguishment of debt.. 16th . Edition. Kieso . ●. . Weygandt . ●. . Warfield. . Explain . the nature, economic substance, and advantages of lease transactions. .. Describe . the accounting for leases by lessees.. LEARNING OBJECTIVES. 16th . Edition. Kieso . ●. . Weygandt . ●. . Warfield. . Indicate . how to report cash and related items. .. . Define receivables and understand accounting issues related to their recognition. . Intermediate Accounting Seventeenth Edition Kieso ● Weygandt ● Warfield Chapter 5 Balance Sheet and Statement of Cash Flows This slide deck contains animations. Please disable animations if they cause issues with your device. The Benefits of Reading Books The Benefits of Reading Books The Benefits of Reading Books,Most people read to read and the benefits of reading are surplus. But what are the benefits of reading. Keep reading to find out how reading will help you and may even add years to your life!.The Benefits of Reading Books,What are the benefits of reading you ask? Down below we have listed some of the most common benefits and ones that you will definitely enjoy along with the new adventures provided by the novel you choose to read.,Exercise the Brain by Reading .When you read, your brain gets a workout. You have to remember the various characters, settings, plots and retain that information throughout the book. Your brain is doing a lot of work and you don’t even realize it. Which makes it the perfect exercise!

Download Document

Here is the link to download the presentation.

"Intermediate Accounting"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents