PDF-DIRECTORATE GENERAL FOR INTERNAL POLICIES

Author : danika-pritchard | Published Date : 2015-09-16

ECB146s Outright Monetary Transactions AbstractThe creation of the EFSF has allowed the IPAECONNT201205 October 2012 PE 492450 EN This document was requested by

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "DIRECTORATE GENERAL FOR INTERNAL POLICIE..." is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

DIRECTORATE GENERAL FOR INTERNAL POLICIES: Transcript

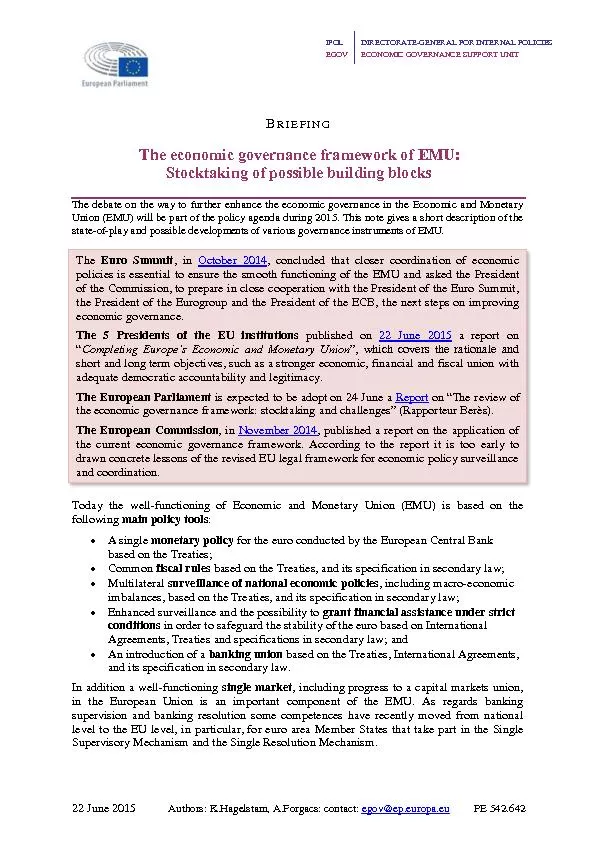

ECB146s Outright Monetary Transactions AbstractThe creation of the EFSF has allowed the IPAECONNT201205 October 2012 PE 492450 EN This document was requested by th. VSc 3557 3557 4150 4150 4481 4481 4440 4440 3464 3464 3586 3586 AGRI 6586 6586 8525 8525 5784 5784 7552 7552 6053 6053 7390 7390 HORT 8793 8793 9512 9512 8206 8206 8955 8955 7672 7672 8523 8523 HORT PAY 9609 10557 8411 8350 6133 8710 CABM 9706 9706 031 66339 031 66582 Tele Fax No 3345536 3340497 Rate Contract No ME3RC14080205062001WAC03FrizairCOAM1076 Dated 12022001 To Ms Frizair Corporation B4748 Industrial Estate Sanathnagar Hyderabad 500 018 Sub Rate contract for the supply of Window T Precincts. National Capital Regional Police Office. Police Regional Office 1-3, 5-13, ARMM, CAR, CALABARZON, MIMAROPA. 5 District Offices. Police Stations. Sub-stations. Regional. Public Safety. Battalion. Web 2.0 and Library 2.0. An introduction. TUT Library Workshop. Fatima Darries. 9 June 2010. Pretoria, South Africa. Full page photograph or graph . TUT LIS Directorate. http://en.wikipedia.org/wiki/File:Web_2.0_Map.svg. IPOL EGOV - GENERAL FOR INTERNAL POLICIES E CONOMIC GOVERNANCE SUPPORT UNIT 22 June 2015 Authors: K.Hagelstam, A.Forgacs: contact: egov@ep.europa.eu PE 542.642 B RIEFING The economic governance fr This document was requested by the European Parliament's Committee on Women's Rights and Gender Equality. AUTHOR(S) OpCit Research, London Katie McCracken RESPONSIBLE ADMINISTRATOR Erika Schulze Polic IP/A/ENVI/NT/2012-20 November PE 492.462 This document was requested by the European Parliament's Committee on Environment, Public Health and Food Safety and produced internally in the Policy Departm 25-27August 2015. Addis Ababa, Ethiopia . Reports from Strengthening National Climate Information/ Early Warning System (CI/. EWS. ) Projects. Sao Tome and Principe. Laurent-Mascar Ngoma. Head of environment and Sustainable Development Unit UNDP/STP. 2016 Surface Operations Workshop. Welcome. This workshop has been developed as a review of policies and procedures, affecting Surface Operations, to better promote safety and efficiency for patrols. Although this is an optional workshop, it can be required at the local level. NATIONAL TRAINING MEETING. ROUND TABLE DISCUSSION. Prepared . by: . NATIONAL DIRECTORATE OF VESSEL EXAMINATION . AND RECREATIONAL BOATING SAFETY PROGRAM VISITATION. MISSION STATEMENT. To minimize loss of life, personal injury, property damage, and the environmental impact associated with the use of recreational boats through preventative means to maximize the safe use and enjoyment of United States waterways by the . Contact our medical center today to receive more information or to schedule an appointment by calling our office number 718 275 8900. kindly visit us at www.examsdump.com. Prepare your certification exams with real time Certification Questions & Answers verified by experienced professionals! We make your certification journey easier as we provide you learning materials to help you to pass your exams from the first try. Professionally researched by Certified Trainers,our preparation materials contribute to industryshighest-99.6% pass rate among our customers. kindly visit us at www.examsdump.com. Prepare your certification exams with real time Certification Questions & Answers verified by experienced professionals! We make your certification journey easier as we provide you learning materials to help you to pass your exams from the first try. Professionally researched by Certified Trainers,our preparation materials contribute to industryshighest-99.6% pass rate among our customers. Presented by Jolene Crist and Ben Froemming. Anta Coulibaly - Director of Internal Audit and Enterprise Risk . Jolene Crist - Internal Audit Manager. Ben . Froemming -. Senior Internal Auditor. Ben Eckert - Internal Audit Intern.

Download Document

Here is the link to download the presentation.

"DIRECTORATE GENERAL FOR INTERNAL POLICIES"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents