Explore

Featured

Recent

Articles

Topics

Login

Upload

Featured

Recent

Articles

Topics

Login

Upload

Search Results for 'volatility time'

volatility time published presentations and documents on DocSlides.

THE VOLATILITY OUTLOOK FOR COMMODITIES

by ellena-manuel

ROBERT ENGLE. DIRECTOR VOLATILITY INSTITUTE AT NY...

Derivatives Lecture 22 Volatility

by calandra-battersby

Only non-observable variable. Historical volatili...

Forecasting Energy Market Series Using Econometric Models and Machine Learning Techniques

by finley941

Spyridon Mastrodimitris Gounaropoulos. Supervised ...

Credit and Counterparty Risk Systems That Read

by augustine796

Dan . diBartolomeo. . QWAFAFEW Boston. June 2015....

High frequency

by myesha-ticknor

q. uoting. : . short-term . volatility . in . bid...

Physics Meets Finance:

by danika-pritchard

Risk Systems That . Read. ®. Dan . diBartolomeo....

Chapter 14

by liane-varnes

Time-Varying Volatility and ARCH Models. Walter R...

High Frequency Quoting:

by pamella-moone

Short-Term Volatility . in . Bids and . Offers. J...

High Frequency Quoting:

by faustina-dinatale

Short-Term Volatility . in . Bids and . Offers. J...

The macroeconomics of time-varying uncertainty

by olivia-moreira

Nick Bloom (Stanford & NBER). Harvard, April ...

MODELING COMMODITY PRICES WITH DYNAMIC CONDITIONAL BETA

by test

ROBERT ENGLE. DIRECTOR: VOLATILITY INSTITUTE AT N...

The macroeconomics of time-varying uncertainty

by jane-oiler

Nick Bloom (Stanford & NBER). Harvard, April ...

Price Discovery, Volatility Spillovers and Adequacy of Spec

by natalia-silvester

Marin Bozic. University of Minnesota-Twin Cities....

High Frequency Quoting:

by faustina-dinatale

Short-Term Volatility . in . Bids and . Offers. J...

Using The LIBOR Market Model to Price The Interest Rate Der

by kittie-lecroy

交通大學 財務金融研究所. ...

Machine Learning in Finance

by jane-oiler

ISB presentation. Claudio . Moni. 25/03/2010. Mai...

High frequency trading:

by tawny-fly

Issues and evidence. Joel Hasbrouck. 1. The US (R...

Using The LIBOR Market Model to Price The Interest Rate Der

by myesha-ticknor

交通大學 財務金融研究所. ...

Selecting The Ideal Option Strike Price Using Fibonacci

by celsa-spraggs

Part II – October 1. st. , 2015 . PART II – O...

Mike West Duke University

by briana-ranney

ISBA Lecture on Bayesian Foundations ...

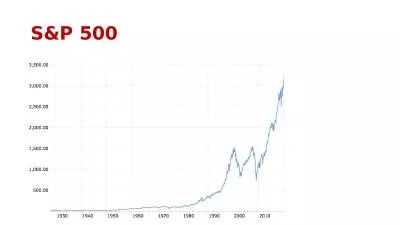

S&P 500 S&P 500, logarithmic scale

by paige

Asset price model assumption. S(t) = Asset price a...

Fundamental Concept Option prices don’t move in a linear way compared to their underlying stocks

by dailyno

Using the Greeks we can understand what will happe...

THE KEY TO SUCCESSFUL INVESTING ISN’T PREDICTING THE FUTURE, IT’S LEARNING FROM THE PAST AND UN

by karlyn-bohler

“PRINCIPLES FOR SUCCESSFUL LONG-TERM INVESTING,...

Term Structure Model Implementation, Calibration, and Validation

by trish-goza

2016 MFM WINTER MODELING . WORKSHOP, Master of F...

Value -at-Risk on a portfolio of Options, Futures and Equities

by stefany-barnette

Radhesh. . Agarwal (Ral13001) . Shashank Agarwal...

Comments on Frankel’s

by alida-meadow

“Systematic Managed Floating”. Andrew K. Rose...

Volatility of container ocean freight

by pamella-moone

Volatility of container ocean freight. 1. The b...

Path integrals for option pricing

by faustina-dinatale

Theory of . Quantum and. Complex systems. Statist...

The macroeconomics of time-varying uncertainty

by lindy-dunigan

Nick Bloom (Stanford & NBER). IMF Lectures, J...

Temporal Query Log Profiling to Improve Web Search Ranking

by alexa-scheidler

Alexander . Kotov. (UIUC). . Pranam. . Kolari....

Event-Driven Finance

by phoebe-click

Lecture 3: Dynamics.. ...

Determinants of Credit Default Swap Spread:

by tatyana-admore

Evidence . from the Japanese Credit Derivative . ...

Load More...