PDF-Retail Equity ResearchSteaming up for the cold zone

Author : tawny-fly | Published Date : 2015-10-26

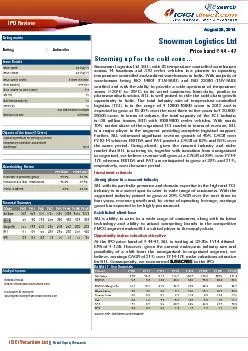

August 25 2014 IPO Review Key Financials CroreFY10FY11FY12FY13FY14FY15EFY16EFY17ENet Sales34645261411371534193825453312EBITDA5490129255380496662869EBITDA Margin

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "Retail Equity ResearchSteaming up for th..." is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Retail Equity ResearchSteaming up for the cold zone: Transcript

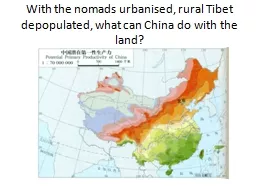

August 25 2014 IPO Review Key Financials CroreFY10FY11FY12FY13FY14FY15EFY16EFY17ENet Sales34645261411371534193825453312EBITDA5490129255380496662869EBITDA Margin 15719921022. WindChill and Heat Index information is from the National Weather Service Child Care Weather Watch atching the weather is part of a child care providers job Planning for playtime field trips or weather safe ty is part of the daily routine The change zone zonezone zone zone zone zone N How Chinese scientists expect climate change to make Tibet more productive. 热带森林. Tropical Forest. 亚热带森林. Subtropical Forest. 亚热带型山地森林. mountainous forest with Subtropical type. Core body temperature . . thermoregulatory mechanisms that rely largely on control of cutaneous blood flow. AV anastomoses, abundant in . acral. areas regulate volume of blood that passes through skin.. In this session we will explore equity praxis and pedagogy, equity literacy abilities, and what creates barriers to successful implementation…And how to overcome those barriers! . Facilitated By. Veronica Neal, . April 13, 2016. Job Zone/Career Zone/SMART. https://www.jobzone.ny.gov. https://www.careerzone.ny.gov. . . . . What is Job Zone? . . Creating a Free Account. . Date:. Time in effect. From:. Time in effect. To:. . Population. (approx.). No. of. Dwellings (approx.). Evacuation Centre. Option 1. Evacuation Centre. Option 2. Evacuation Routes. 563. 201. Caboolture Memorial Hall. SEO is anything but a “one size fits all” strategy. What works for one website may not work for another. And what worked for you in the past may not yield the same results in the future. If your cold emails do not match these standards then yes, you’ve got to go back and revise them. Yes, that’s a pain, but at least you’ll know what to do the next time around. The Abyssal Zone Created by Shalynn Lee The Abyssal Zone What is it? The Abyssal Z one is 1 out of the 5 pelagic layers in the ocean. This zone contains a very deep depth. “Abyss” comes from the Greek word “ . SYFTET. Göteborgs universitet ska skapa en modern, lättanvänd och . effektiv webbmiljö med fokus på användarnas förväntningar.. 1. ETT UNIVERSITET – EN GEMENSAM WEBB. Innehåll som är intressant för de prioriterade målgrupperna samlas på ett ställe till exempel:. In conclusion, retail signage plays a crucial role in guiding and engaging customers within a retail environment. Explore here! If you are wondering what the design of your cold storage facility should be and how you can get the best results with the design, you should trust RL Cold for it. Working Towards Health Equity with Wellbeing and Self-Compassion In Mind. Thursday, December 14th, 2023. 12-1pm ET. Questions, Comments & Closed Captioning. Disclaimer. The views, opinions, and content expressed in this presentation do...

Download Document

Here is the link to download the presentation.

"Retail Equity ResearchSteaming up for the cold zone"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents