PDF-UnbowedQ2 Westpac McDermott MillerConsumer Con dence Index: 121.2Consu

Unbowed 3

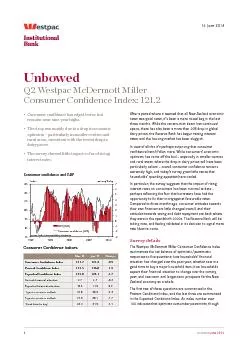

2

1

012345677585

105

115

125

135

1989

1995

2001

2007

2013

ann avg chg

Index

GDP RHS

Consumer confidence LHSSource Westpac McDermott Miller Statistics NZ

Mar14ChangeConsumer

Download Presentation

"UnbowedQ2 Westpac McDermott MillerConsumer Con dence Index: " is the property of its rightful owner. Permission is granted to download and print materials on this website for personal, non-commercial use only, provided you retain all copyright notices. By downloading content from our website, you accept the terms of this agreement. Download

Presentation Transcript

Transcript not available.