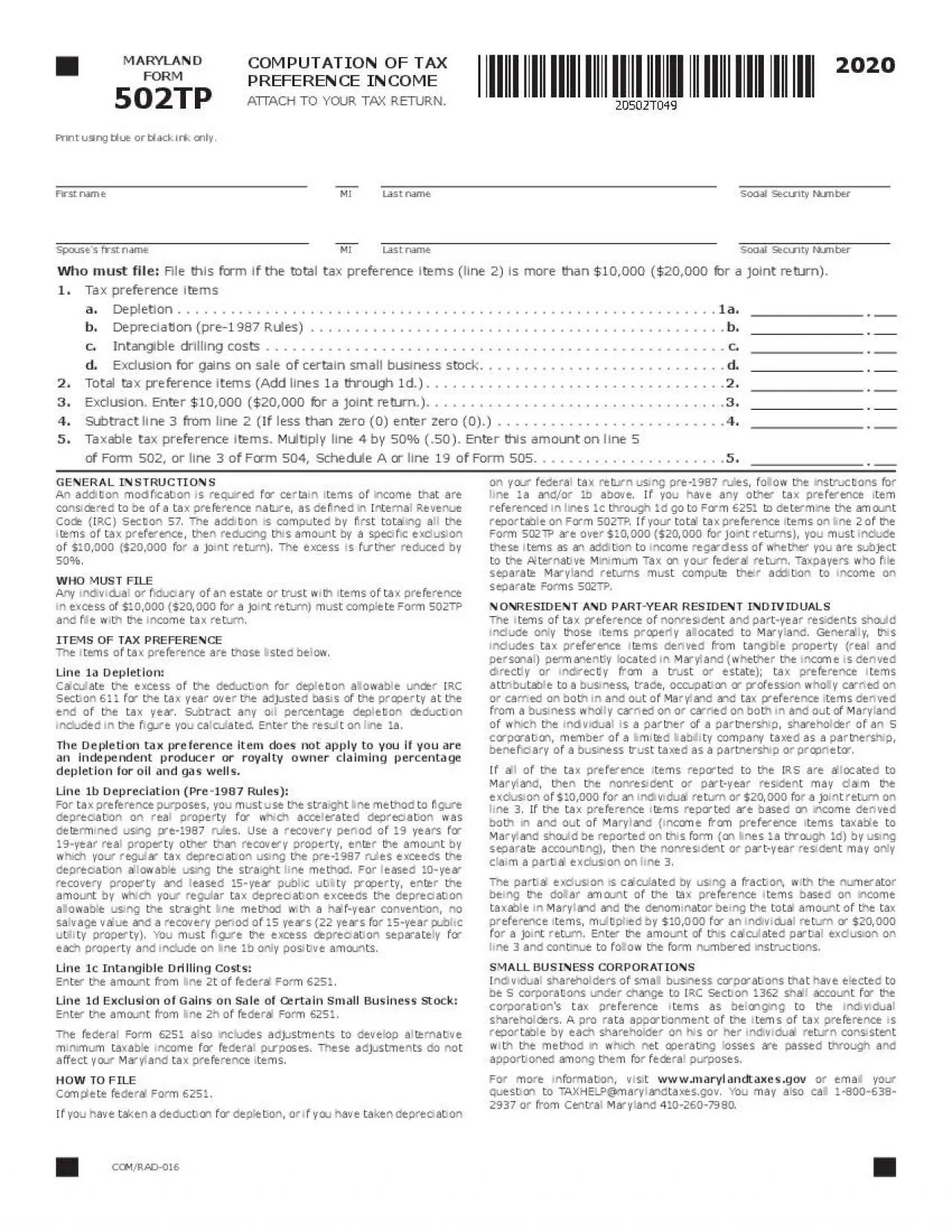

PDF-Who must file

File this form if the total tax preference items line 2 is more than 10000 20000 for a joint return1Tax preference itemsa1abDepreciation pre1987 RulesbcIntangible

Download Presentation

"Who must file" is the property of its rightful owner. Permission is granted to download and print materials on this website for personal, non-commercial use only, provided you retain all copyright notices. By downloading content from our website, you accept the terms of this agreement.

Presentation Transcript

Transcript not available.