PPT-Identifying and Classifying Costs for Indirect

Author : briana-ranney | Published Date : 2025-05-29

Identifying and Classifying Costs for Indirect Cost Rates North Carolina Department of Health and Human Services Office of the Controller Cost AnalysisFederal Financial

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "Identifying and Classifying Costs for In..." is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Identifying and Classifying Costs for Indirect: Transcript

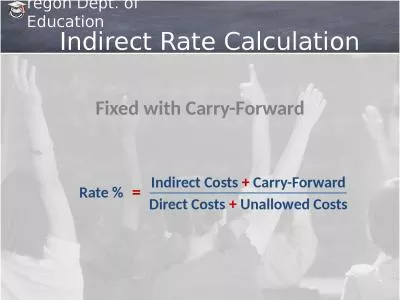

Identifying and Classifying Costs for Indirect Cost Rates North Carolina Department of Health and Human Services Office of the Controller Cost AnalysisFederal Financial ReportingAdministrative Services October 2016 Objectives Background. OMB Circular A-110 (2 CFR Part 215) . 2 CFR Part 230. Appendix A – General Principles. . GPD Indirect Cost Rate Agreement . Chief, . Operational Oversight Division. Joseph E. Baldwin . Project Review: . U.S. Department of Education. Objectives. Overview of Indirect Costs. Key Changes Under the Uniform Guidance. GAN Changes. De Minimis . R. ate. Grant Extensions. Sub-Recipient Rates. Timelines. Time and Effort . . . WHAT ARE INDIRECT COST RATES????. Indirect Cost Pool-How Deep?. Indirect Cost Base-How Large?. Indirect Cost Rate-How High?. AGENDA. . Who Are We- Indirect Cost Branch. Definitions. Why Indirect Cost Rates Are Needed; Including An Example . U.S. Department of Education. Objectives. Overview of Indirect Costs. Key Changes Under the Uniform Guidance. GAN Changes. De Minimis . R. ate. Grant Extensions. Sub-Recipient Rates. Timelines. Time and Effort . To understand one objection to indirect realism. What we’re directly aware of are our . sense data. .. . ?. Remember. If a tree falls over in a forest, and no one is there to hear it…. …does it make a noise?. Office of Management and Budget (OMB) – Circular A-87. US Department of Education. Delegates authority for rate determination to states. Delegation agreement renews every five years. Authority. 2. Costs of a general nature which are not readily identifiable with the activities of the grant but are incurred for the joint benefit of those activities and other activities or programs of the organization. . Appendices III - VII. Indirect/F&A Costs. 2 CFR 200.56. Costs incurred for Common or Joint purposes. Benefit more than one cost objective. Cannot be readily identified with particular cost objective without undue effort. Office of Management and Budget (OMB) – Circular A-87. US Department of Education. Delegates authority for rate determination to states. Delegation agreement renews every five years. Authority. 2. Costs of a general nature which are not readily identifiable with the activities of the grant but are incurred for the joint benefit of those activities and other activities or programs of the organization. OMB Circular A-110 (2 CFR Part 215) . 2 CFR Part 230. Appendix A – General Principles. . GPD Indirect Cost Rate Agreement . Chief, . Operational Oversight Division. Joseph E. Baldwin . Project Review: . What’s . the difference? . Overview. Define administrative costs. . Describe . the difference between direct and indirect costs. . Describe . what an indirect cost rate agreement is and where you go to apply for one. . Direct Costs . +. . Unallowed. Costs. =. Rate %. . Fixed . with Carry-Forward. Indirect Rate Calculation. Indirect Cost Classification Matrix. Classifications: Direct, Excluded, Indirect, or Unallowed. Fiscal Year . #### Rates—provides guidance for all fiscal years. Authority. Office of Management and Budget (OMB) – Circular A-87. US Department of Education. Delegates authority for rate determination to states. What are Product Costs?. Product costs are costs that are incurred to create a product that is intended for sale to customers. . Product . costs include direct material (DM), direct labor (DL) and manufacturing overhead (MOH).. Branch Chief. Indirect Cost Services Division (ICSD). Interior Business Center (IBC). U.S. Department of Interior (DOI. ). Agenda. General . Principles . Uniform Guidance. Direct, Indirect, Unallowable, Exclusions.

Download Document

Here is the link to download the presentation.

"Identifying and Classifying Costs for Indirect"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents