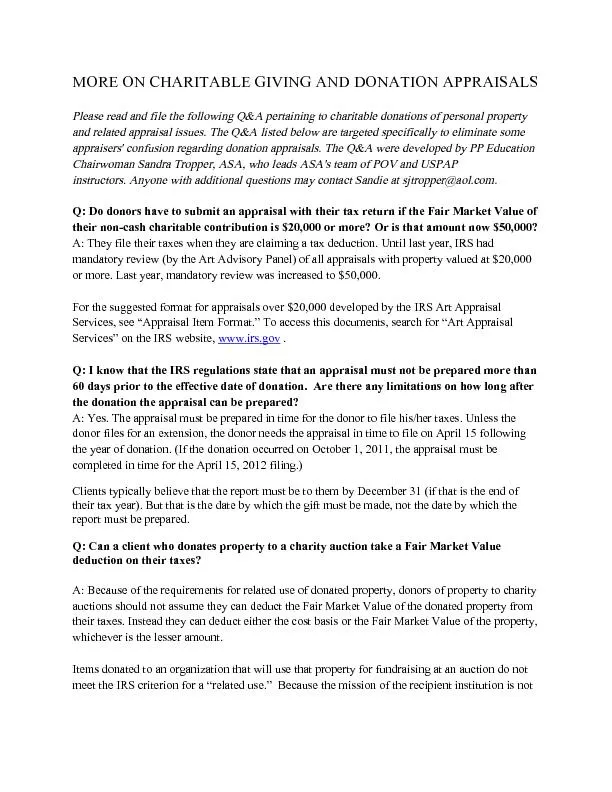

PDF-or more? Or is that amount now $50,000? A: They file their taxes when

Author : mitsue-stanley | Published Date : 2016-05-29

deduction on their taxes A Because of the requirements for related use of donated property donors of property to charity auctions should not assume they can deduct

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "or more? Or is that amount now $50,000? ..." is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

or more? Or is that amount now $50,000? A: They file their taxes when: Transcript

deduction on their taxes A Because of the requirements for related use of donated property donors of property to charity auctions should not assume they can deduct the Fair Market Value of the do. Old folks allow their bellies to jig gle like slow tambourines The hollers rise up and spill over any way they want When old folks laugh they free the world They turn slowly slyly knowing the best and worst of remembering Saliva glistens in the cor National Aeronautics and Space Administration 300,000,000900,000,0001,500,000,0002,100,000,0002,700,000,0003,300,000,0003,900,000,0004,500,000,000 5,100,000,0005,700,000,000kilometers 0 Source: MRI . Doublebase. 2013. Cable . Viewer . Index. Broadcast . Viewer. Index. Automotive. Total Amount Spent on Most Recent Purchase/Lease [$30,000+]. 109. 61. Total Amount Spent on Most Recent Purchase/Lease [$50,000 +]. GOVERNMENT OF WEST BENGAL. Direct Reforms (Restructuring, Reorganisation). Indirect Reforms (Through ICT & Process Reengineering). REFORMS IN VAT LAWS. Direct Administration Reforms: Reorganisation in the Directorate of Commercial Taxes. National Aeronautics and Space Administration 300,000,000900,000,0001,500,000,0002,100,000,0002,700,000,0003,300,000,0003,900,000,0004,500,000,000 5,100,000,0005,700,000,000kilometers 0 LG-2009-09-570 National Aeronautics and Space Administration 300,000,000900,000,0001,500,000,0002,100,000,0002,700,000,0003,300,000,0003,900,000,0004,500,000,000 5,100,000,0005,700,000,000kilometers 0 Three Types of Taxes. Progressive Tax. Regressive Tax. Proportional Tax. Progressive Tax. A progressive tax is a tax for which the percentage of income paid in taxes increases as income increases.. Our Federal Taxes System is Progressive. “I want to find out who this FICA guy is and how come he’s taking so much of my money.” . -- Nick Kypreos . Chapter 10. . 10-. 2. LO # 1 Payroll and Form 1040. Withholding taxes are imposed on taxpayers to help fund government operations using a “pay as you go” system. Sales Tax Exemptions. “Sale Tax Exemption” Means That A Sales Transaction Is Not Subject To Sales Tax (SGC 4.09.100). 28 Separate Categories of Sales Tax Exemptions in Sitka General Code. In 2014, only 40.5% of all reported sales transactions in Sitka were taxed. 59.5% of all reported sales transactions were exempt from sales taxation. These percentages DO NOT include unreported sales, such as internet sales. Thus, the actual percentage of sales transaction with a nexus in Sitka is less than 40%.. Doug Walker. College of Charleston. 85. th. Annual Meetings, Southern Economic Association. Session on . Taxing More Choice. 21 November 2015. Background. Lottery. First modern lottery in NH, 1964. Now all but 6 states (AL, AK, HI, MS, NV, UT). . Understanding Federal Income Tax Principles. . Internal Revenue Service (IRS). responsible for administration and enforcement of federal tax laws. July 8, 2016. Industry overview. Louisiana limits the number of riverboat gaming licenses to a total of fifteen which must be located on specific waterways within the state.. Those fifteen licenses by market are currently distributed:. Ben Trnka/Boz Bostrom. www.benandboz.com. . Liabilities will differ by company and industry. Overview. Understand how to account for liabilities. Understand how to compute future value of a single amount and an annuity. Mrs. . Leuschen’s. 3. rd. Period Math. Learning Targets. I can find the discount using the percent equation. I can find the new cost of a discounted item. I can find the markup cost using the percent equation.

Download Rules Of Document

"or more? Or is that amount now $50,000? A: They file their taxes when"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents