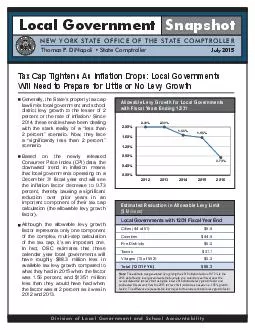

PDF-If these trends continue, it is possible that some local governments w

Author : myesha-ticknor | Published Date : 2016-08-13

later in 2016 could even be faced with zero allowable levy growth For example in school districts which have fiscal years beginning July 1 the impact of a more restrictive

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "If these trends continue, it is possible..." is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

If these trends continue, it is possible that some local governments w: Transcript

later in 2016 could even be faced with zero allowable levy growth For example in school districts which have fiscal years beginning July 1 the impact of a more restrictive allowable levy growth. State Directs. State Constitutions describe how village, town, county, and city governments will be set up.. Charter. – basic plan for local governmental unit that defines its powers, responsibilities, and organization.. Green Eggs and Ham. By Dr. Seuss. Power Point By Corinne Perry. Do you like Green Eggs and Ham?. I do not like them, Sam I am. I do not like green eggs and ham.. Click on Sam to continue!. Would you like them here or there?. . 2011 Clairmont Press. Distribution of Power. Governments can be classified based upon how they distribute power between central and local governments.. There are three ways:. Unitary. Confederation. Presents. Scheduling Participant Visits. With WebCAMP CUIC forms. Introduction. This module is designed to instruct research study investigators, coordinators and other staff how to request a scheduled admission of a study participant to the CRC using the WebCAMP Research Management System.. Dr. Sherifa . Fouad. . Sherif. Cairo University. Corporate Social Responsibility (CSR) is the commitment of business to contribute to sustainable economic development, working with employees, their families, the local community and society at large to improve quality of life, in ways that are both good for business and good for development. . Mrs. Kim West. 8. th. Grade Georgia Studies. GPS: SS8CG5. Georgia Performance Standards. SS8CG5 . The student will analyze the role of . local governments . in the state of Georgia. . a. . Explain the origins, functions, purposes, and differences of county and city governments in Georgia. . Data contributed from Rose Wilson, Rosalie J Wilson Business Development Services and Mary . P. eabody, UVM Extension. Macro . T. rends & Key Words. Healthy & . Natural. Functional Foods. “No . The units of local governments in Virginia are political subdivisions created by the General Assembly.. The units of local government in Virginia are counties, towns, and cities. Local governments exercise legislative, executive, and judicial powers.. Carol S. Weissert, PhD. Director, LeRoy Collins Institute. Professor of Political Science. Florida State University. Senate Committee on Governmental Oversight and Accountability. January 17. , 2013. It’s everyone’s responsibility . to empower, help, and advise Microsoft customers so they get the best experience.. Thank you for your dedication to enable the Customer Experience Framework and deliver on the Microsoft mission.. 2Y2YWe continue to maintain strict and effecti e infection 22 NCONTESTED MOTION TO CONTINUEDOCKET NUMBERPetitionerversus PARISH OF DefendantThis matter comes before the court on Motion to Continuefiled by Plaintiff/Mover Defendant/RespondentAttorney for Plain Opportunities to profile work on the Action Agenda for Nature and People. Mr. Mohamed Elyes KCHOUK. Regional Specialist for francophone Africa for the United Nations Environment Programme (UNEP) – Biosafety Clearing-House (BCH) Project 3. . Issues and Status of Local Government in Myanmar . Name : AKAR, Tin Oo. ID : MEY-15008 . Program : YLP (the School of Government). Country : The Republic of the Union of Myanmar.

Download Rules Of Document

"If these trends continue, it is possible that some local governments w"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents