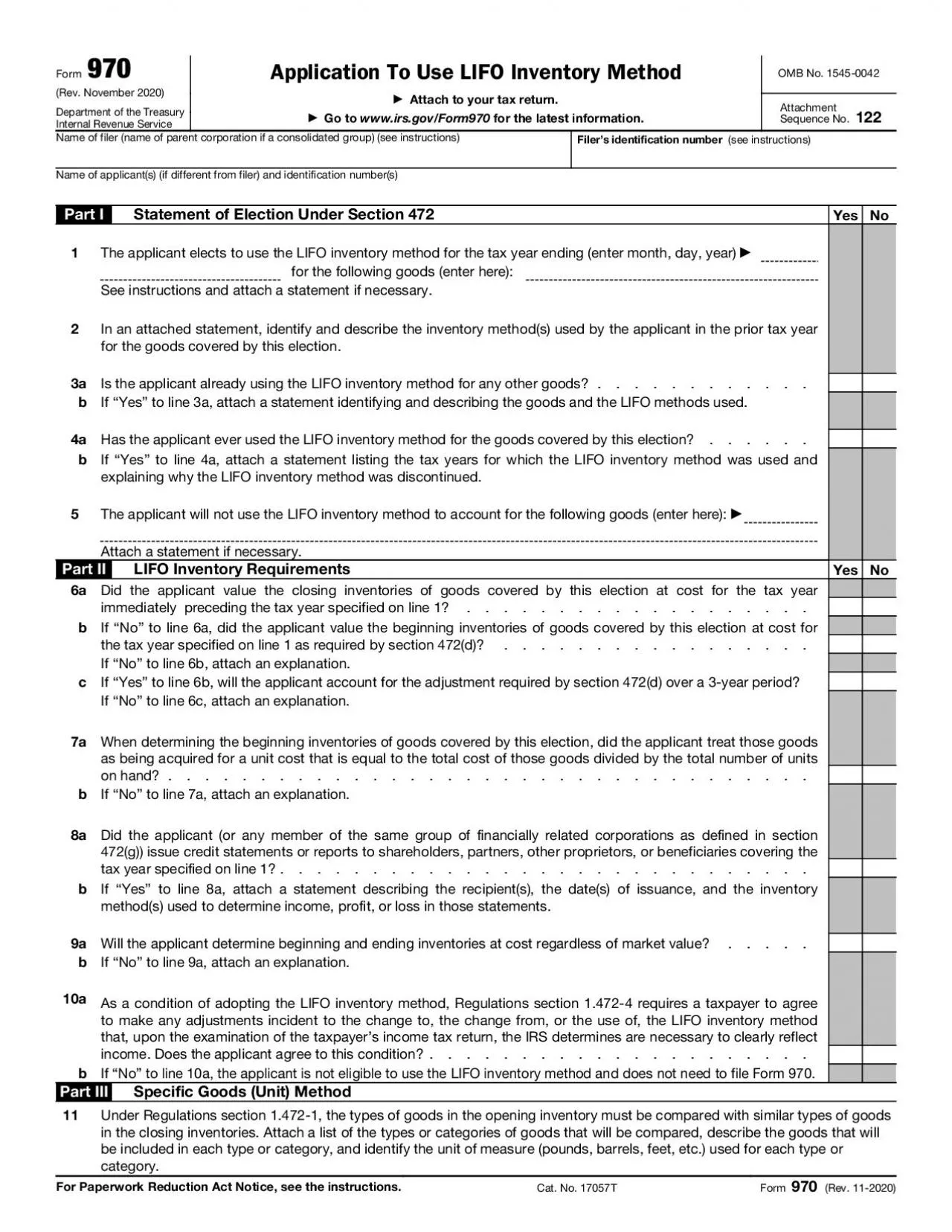

PDF-Form 970Rev November 2020

Department of the Treasury Internal Revenue Service Application To Use LIFO Inventory Method Attach to your tax return Go to wwwirsgovForm970 for the latest information

Download Presentation

"Form 970Rev November 2020" is the property of its rightful owner. Permission is granted to download and print materials on this website for personal, non-commercial use only, provided you retain all copyright notices. By downloading content from our website, you accept the terms of this agreement.

Presentation Transcript

Transcript not available.