PDF-Retail Equity Research

Author : briana-ranney | Published Date : 2016-10-04

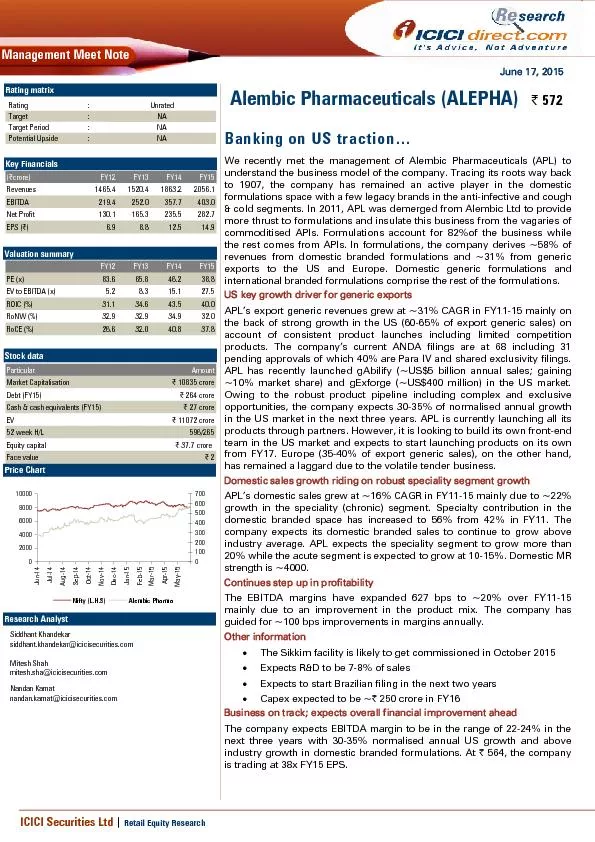

June 17 2015 Management Meet Note We recently met the management of Alembic Pharmaceuticals APL to understand the business model of the company Tracing its roots

Presentation Embed Code

Download Presentation

Download Presentation The PPT/PDF document "Retail Equity Research" is the property of its rightful owner. Permission is granted to download and print the materials on this website for personal, non-commercial use only, and to display it on your personal computer provided you do not modify the materials and that you retain all copyright notices contained in the materials. By downloading content from our website, you accept the terms of this agreement.

Retail Equity Research: Transcript

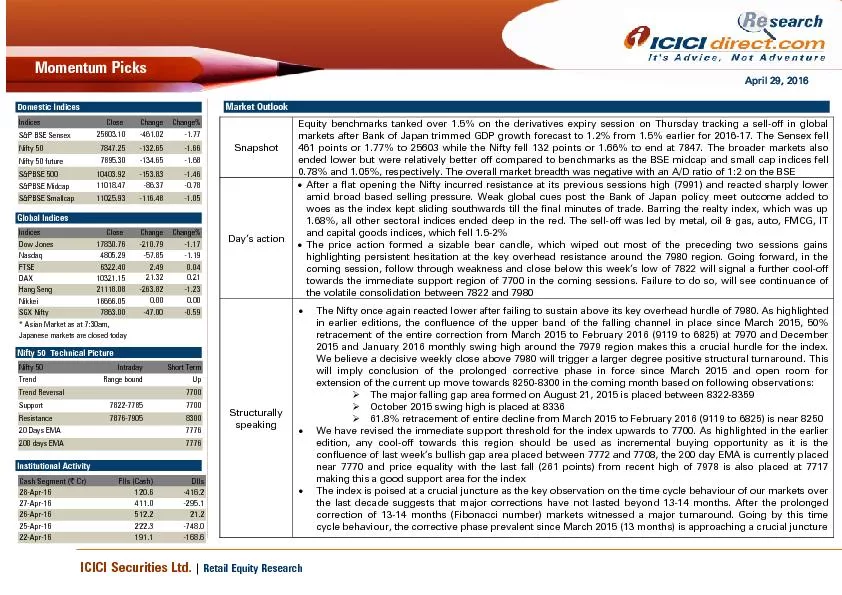

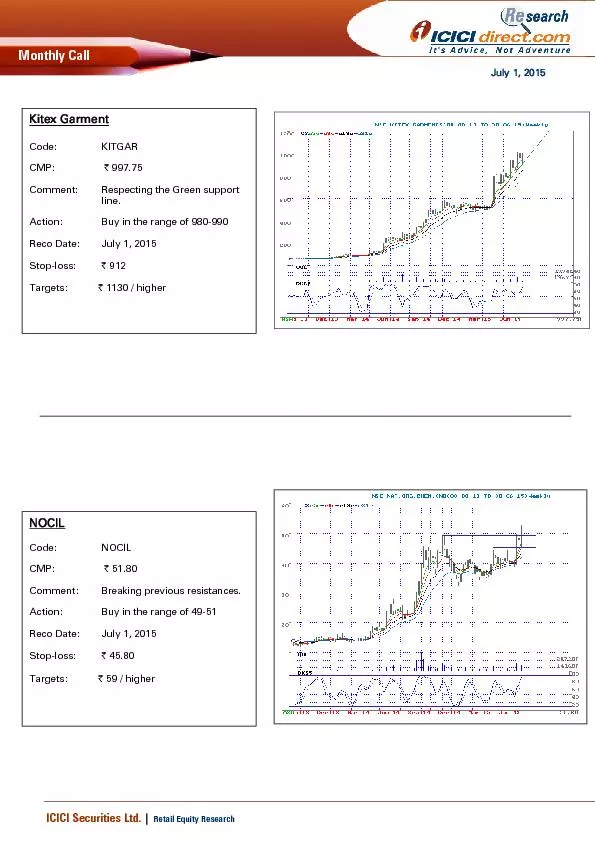

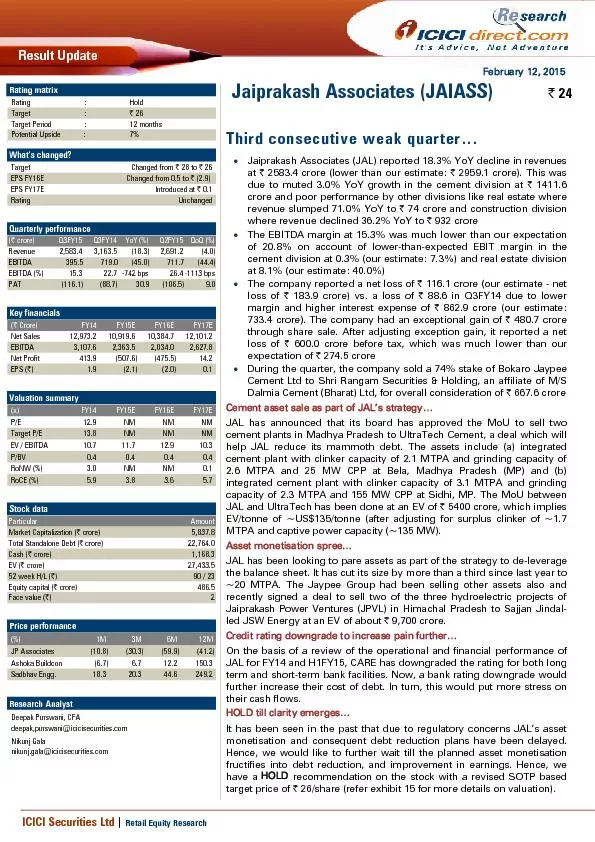

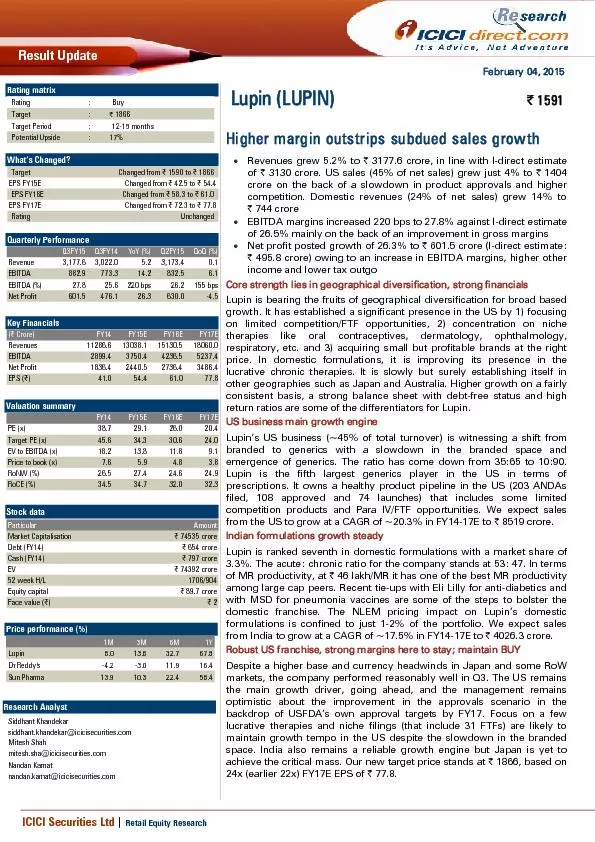

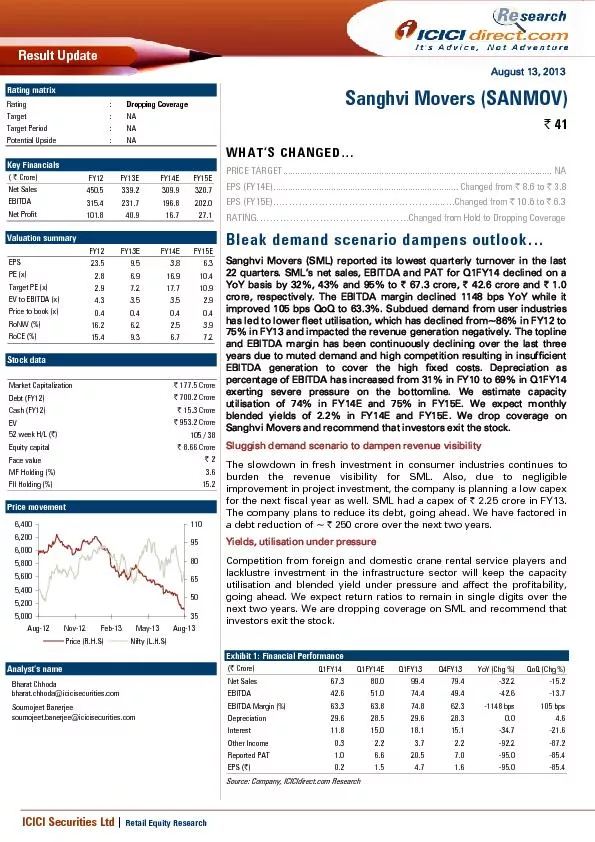

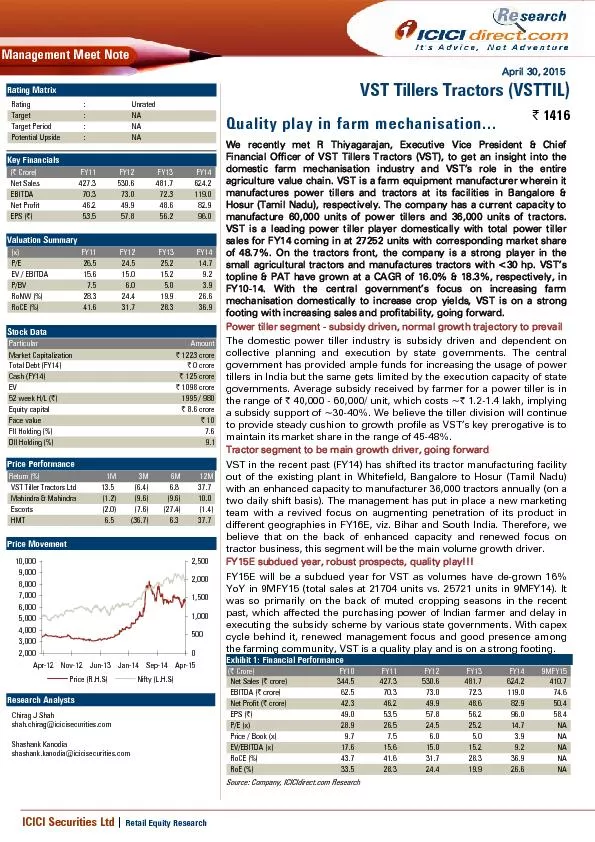

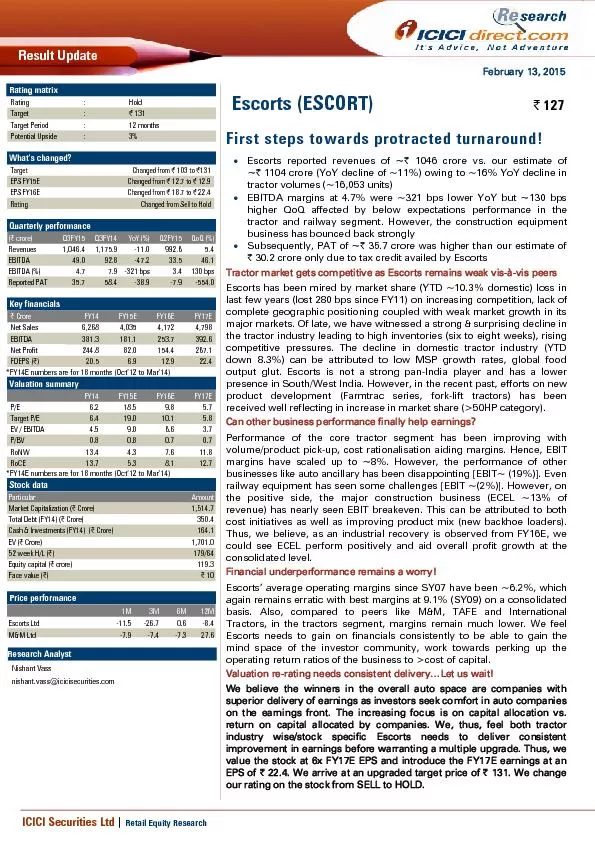

June 17 2015 Management Meet Note We recently met the management of Alembic Pharmaceuticals APL to understand the business model of the company Tracing its roots way back to 1907 the company has. November 21, 2012 IPO Review Key Financials | croreFY09FY10FY11FY12May 2012Net Sales754.2 804.4 1,142.3 1,399.1 178.9 EBITDA (%) 8.3 8.5 9 August 18, 2014 Result Update Topline growth remains tepid April 24, 2015 MotoGaze April 2015 March ends on flattish note!!! Weak rural demand impacts volumes For March 2015, overall auto industry sales volumes declined ~1% YoY. This happened mainly after t Market Outlook Snapshot Equity benchmarks tanked over 1.5% on the derivatives expiry session on Thursday tracking a sell-off in global markets after Bank of Japan trimmed GDP growth forecast to 1.2% f Monthly Call Kitex Garment Code: KITGAR CMP: | 997.75 Comment: Respecting the Green support Action: Buy in the range of 980-990 Reco Date: July 1, 2015 Stop-loss: | 912 Targ February 12, 2015 Result Update Jaiprakash Associates (JAL) reported 18.3% YoY decline in revenues at | 2583.4 crore (lower than our estimate: | 2959.1 crore). This was due to muted 3.0% YoY growth i February 4, 2015 Result Update Higher margin outstrips subdued sales growth Revenues grew 5.2% to | 3177.6 crore, in line with I-direct estimate of | 3130 crore. US sales (45% of net sales) grew just August 13, 2013 Result Update PRICE TARGET................................................................................................................NA .......................................... April 30, 2015 Management Meet Note Quality play in farm mechanisation... We recently met R Thiyagarajan, Executive Vice President & Chief Financial Officer of VST Tillers Tractors (VST), to get an i Disclaimer ANALYST CERTIFICATION We /I, Bharat Chhoda, MBAAnkit Panchmatia MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in September 7, 2015 Management Meet Note We met the management of Eros International to get a deeper insight into the growth triggers that would favour the company in coming years. Eros, producer/distr February 13, 2015 Result Update Escorts reported revenues of ~| 1046 crore vs. our estimate of ~| 1104 crore (YoY decline of ~11%) owing to ~16% YoY decline in tractor volumes (~16,053 units) EBITDA March 13, 2015 Business specific Delay in revival of capex cycle/industrial activity: Pitti May 11, 2015 Management Meet Note BKC project the trump card

Download Document

Here is the link to download the presentation.

"Retail Equity Research"The content belongs to its owner. You may download and print it for personal use, without modification, and keep all copyright notices. By downloading, you agree to these terms.

Related Documents