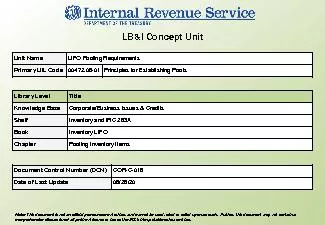

PDF-LBI Concept UnitUnit Name LIFO Pooling Requirements Primary UIL Code

Document Control Number DCN CORC018 Date of Last Update 062620 Note This document is not an official pronouncement of law and cannot be used cited or relied upon

Download Presentation

"LBI Concept UnitUnit Name LIFO Pooling Requirements Primary " is the property of its rightful owner. Permission is granted to download and print materials on this website for personal, non-commercial use only, provided you retain all copyright notices. By downloading content from our website, you accept the terms of this agreement.

Presentation Transcript

Transcript not available.